Some wait-and-see ahead of the FOMC meeting outcome: S&P 500, China A50, GBP/USD

Entry posted by MongiIG in Market News

660 views

The US equity markets came in mixed overnight, largely taking a breather from their recent sell-off, along with some wait-and-see ahead of the FOMC meeting outcome.

Source: Bloomberg

Source: Bloomberg

Market Recap

The US equity markets came in mixed overnight (DJIA -0.50%; S&P 500 -0.38%; Nasdaq +0.18%), largely taking a breather from their recent sell-off, along with some wait-and-see ahead of the Federal Open Market Committee (FOMC) meeting outcome. That said, the US 10-year Treasury yields continued to push to a new 11-year high at 3.48%, which reflects further build-up in hawkish bets for Fed’s monetary policy outlook. Thus far, a 75 basis-point hike in the upcoming Fed meeting has been well-anchored as seen from the Fed funds futures, which marks a significant revision from the 50 basis-point hike being priced just last week. With that, further confirmation will be sought later tonight as to whether the Fed will deem the recent upside surprise in inflation as a justification for such an aggressive move.

The last glimpse of inflationary pressures ahead of the FOMC meeting came from the release of the US producer price index (PPI), which rose 10.8% year-on-year (YoY). While the reading was slightly below the 10.9% consensus, it provided little reason to cheer with a double-digit increase running the risk of further cost pass-through to consumers ahead. That seems to reinforce the narrative of inflationary pressures being higher-for-longer in the US and anchor the stance for Fed’s aggressive tightening to continue.

The recent sell-off in the S&P 500 has marked the formation of a new lower high and lower low, leaving its downward trend intact. Having fallen by close to 10% since last Thursday, all eyes are on the upcoming Fed meeting for any near-term relief.

Source: IG charts

Source: IG charts

Asia Open

Asian stocks look set for a lower open, with Nikkei -0.34%, ASX -0.59% and KOSPI -0.60% at the time of writing. Ahead of the Fed meeting outcome, market participants may be refraining from taking on excessive risks while awaiting greater clarity on guidance for Fed’s tightening ahead. That may lead to some muted movements in the Asia region today as well. An attention-grabbing move overnight was the Nasdaq Golden Dragon China Index, which jumped close to 7%, seemingly a breakaway from the weakness in Wall Street. This tapped on a late-session recovery for Chinese equities in the Asia session yesterday, which could point towards some improving market confidence on policy support and potentially some positioning that the worst could be over for China’s economic conditions.

The day ahead will see the release of a series of economic data (fixed asset investment, industrial production, retail sales) out of China, which may be set to improve from April’s reading. Retail sales for May are expected to deliver a 7.1% contraction YoY due to some virus restrictions in place during the month, which restricts consumer spending. That said, it marks a lesser extent of contraction from April’s reading of -11.1%. Industrial production is expected to come in at -0.5% YoY versus -2.9% in April. With some bullish sentiments towards Chinese equities lately, better-than-expected readings ahead may aid to fuel further market confidence for its economic recovery picture.

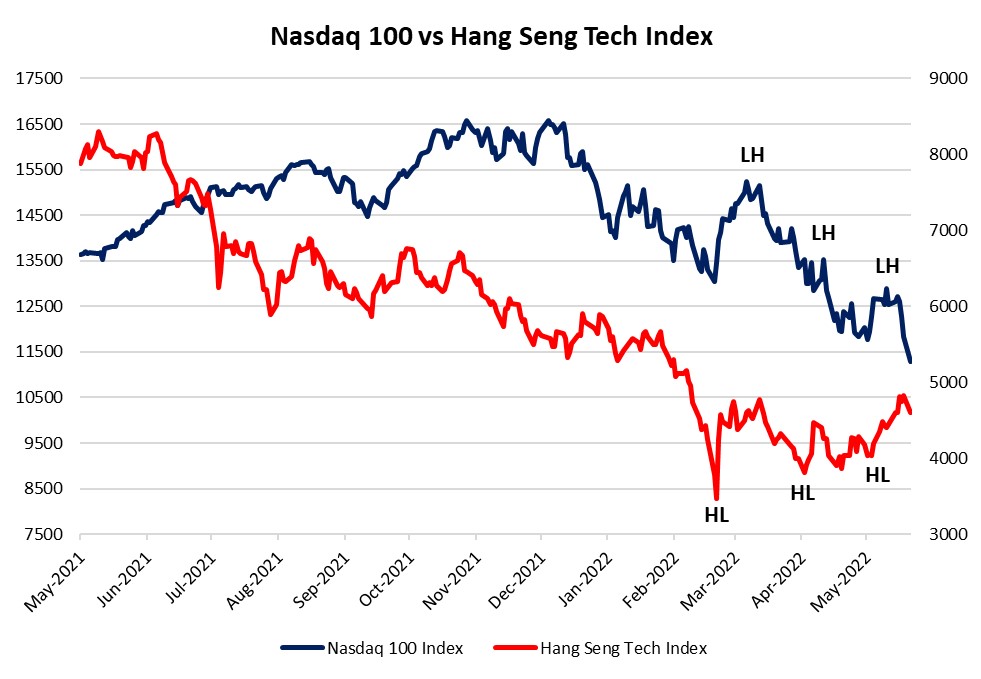

The China A50 index has been trading within an ascending channel pattern since May this year, with the index finding recent support at the lower channel trendline yesterday. This leaves the near-term upward trend intact with the higher lows and trading within the channel will leave the 14,360 level on watch next. Sentiments also seem to be improving on the technology sector in the near term, with the Hang Seng Tech Index forming higher lows as opposed to the lower highs on the Nasdaq 100.

Source: IG charts

Source: IG charts

Source: Bloomberg

Source: Bloomberg

On the watchlist: GBP/USD attempting to hold at key support ahead of BoE interest rate decision this week

The GBP/USD has plunged as much as 4.7% over the past few days, coming after recent US dollar strength and a lower-than-expected April’s GDP figure released in the UK on Monday. That has driven some expectations that the Bank of England (BoE) may have to move more cautiously in its rate increases, with the divergence in tone for monetary policies with the US leading to some downward pressure for the currency pair. The GBP/USD is trading at its lowest level since March 2020 but are currently attempting to hold at a key 1.20 support level. That level has held up the pair on three previous occasions since 2016. Near-term moves will heavily depend on the FOMC meeting outcome, where any push-back against a 75 basis-point hike will lead to some unwinding of hawkish bets and provide a near-term relief for the GBP/USD.

Source: IG charts

Source: IG charts

Tuesday: DJIA -0.50%; S&P 500 -0.38%; Nasdaq +0.18%, DAX -0.91%, FTSE -0.25%

.jpg.27c55ea07d5a17683fbdbda06b8fcace.jpg)

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now