No reprieve for recovery in risk sentiments: Nasdaq 100, Straits Times Index, USD/JPY

Entry posted by MongiIG in Market News

797 views

Coming back from the holiday break, intermittent attempts to rebound for the major US indices overnight failed to sustain as selling pressure continues to overcome previous dip-buying efforts.

Source: Bloomberg

Source: Bloomberg

Market Recap

Coming back from the holiday break, intermittent attempts to rebound for the major US indices overnight failed to sustain as selling pressure continues to overcome previous dip-buying efforts. The US Institute for Supply Management (ISM) services purchasing managers' index (PMI) reading provided the only economic data of note, with the sector accounting for two-thirds of the US economy and its outperformance (56.9 versus 55.1 expected) kept talks of a more aggressive Federal Reserve (Fed) alive. US Treasury yields reacted with a continuation of its upward trajectory, with the 2-year yield back to retest its last week’s high at 3.5% while the 10-year yields broke to a new higher high at the 3.35% level. These are in reaction to the narrative that the Fed has to maintain its higher-for-longer stance to cool the economy, although a slew of corporate debt supply contributed to the increase as well. Expectations for a 75 basis-point (bp) hike were revised back up to 72% probability from previous day’s 57%.

Non-manufacturing prices saw a slight moderation (71.5 versus 72.3 in July), a positive sign that inflation will continue to trend lower over the coming months but the still-elevated reading suggests that the rate of moderation may not be quick enough to instil a policy pivot from the Fed anytime soon. Business activities (60.9 versus 57.0 forecast) and new orders (61.8 versus 59.9 in July) remain in robust expansionary territory but that may change over the coming months as policy tightening effect continues to seep in. This could bring a switch in sentiments towards ‘bad news for the economy is good news for markets’, potentially towards the end of the year.

Rate-sensitive growth sectors saw greater underperformance once more, with the 12,000 level for the Nasdaq 100 index giving way this morning. Trading below its previous resistance-turned-support level at 12,200 and a break below a near-term upward trendline provided an overall downward bias for now. This may leave the 11,700 level on watch next.

Source: IG charts

Source: IG charts

Asia Open

Asian stocks look set for a downbeat open, with Nikkei -0.90%, ASX -1.04% and KOSPI -1.25% at the time of writing. The negative lead in Wall Street reflects the bears retaining control of risk sentiments, which provided little optimism for the Asia session. The Nasdaq Golden Dragon China Index fell 3.45% overnight, showing that the Fed’s tightening outlook took precedence over recent reiteration of policy support from China authorities. That may drive some paring of previous gains in Chinese equities into today’s session as well.

The day ahead places Australia’s quarter two (Q2) gross domestic product (GDP) and China’s trade balance on the economic calendar, where economic conditions in the region will be in focus. Ongoing virus restrictions in China remains an ongoing headwind for risk sentiments, which may drive markets to look beyond any signs of strength. China’s trade figures release later will also provide an indication of ongoing global demand, which are likely to reflect a moderation in economic conditions and providing another downbeat catalyst for markets to digest.

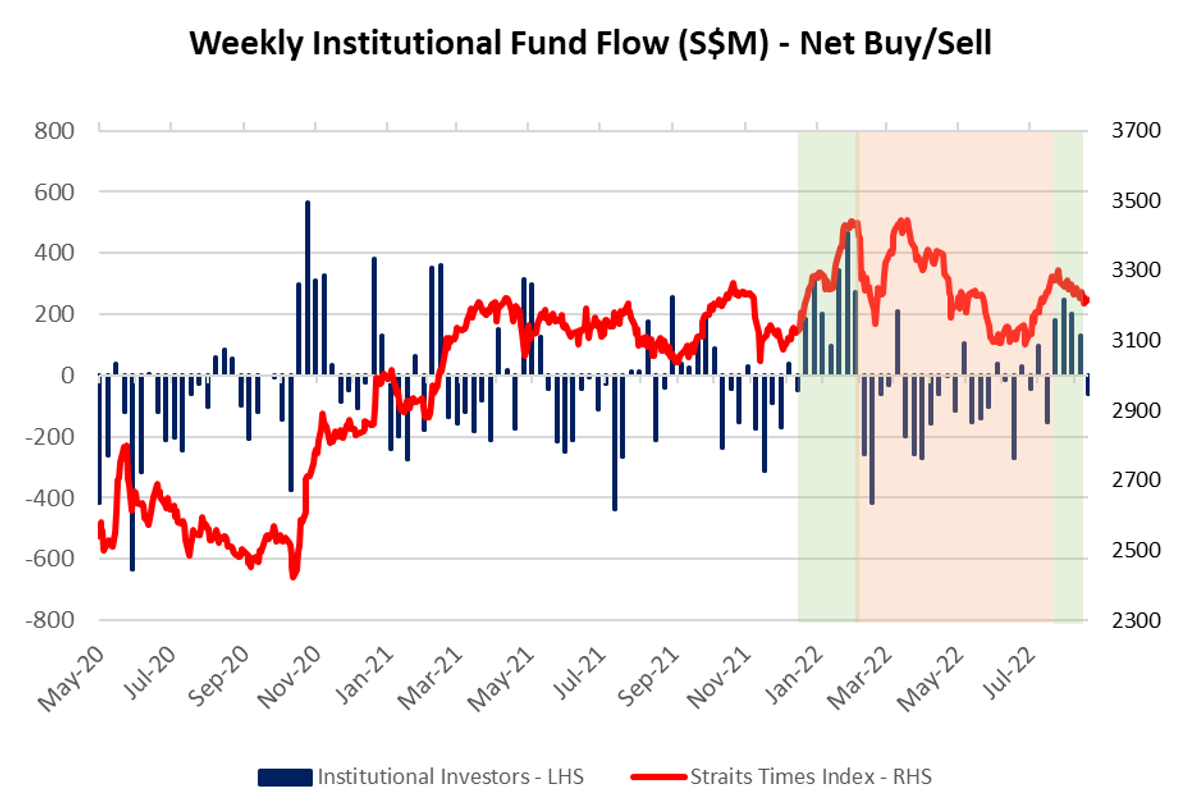

The Singapore Index has been attempting to hang above the 3,200 level, which also marks its 50-day moving average (MA) ahead. The latest SGX fund flow data reflects a net outflow of S$63 million from institutional investors last week, coming after four consecutive weeks of net inflows (amounting to S$762 million overall). The near-term lower highs and lower lows provided an overall downward bias and should the 3,200 support level fail to hold, it may unlock room for further downside to the 3,145 level next.

Source: IG charts

Source: IG charts

Source: SGX, IG

Source: SGX, IG

On the watchlist: USD/JPY on a lift with yield differential but 145.00 level on watch

The USD/JPY has tracked the movements in the US 10-year Treasury yields closely over the past two years, with the widening yield differential brought on by further broad-based selling of US Treasuries overnight providing an uplift for the pair to its highest level since 1998. The 145.00 level will be on close watch, considering that it marks the peak back in 1998 with the Bank of Japan (BoJ)’s intervention by the selling of dollars and purchases of yen. A move above that level could renew some market expectations of intervention, placing a more measured up-move and potentially a ceiling on the USD/JPY. On the technical front, the pair has been trading on an ascending broadening wedge pattern since May this year, with the upper wedge trendline coinciding around the 145.00 level as well. Failure to cross the 145.00 resistance could leave the 139.20 level on watch for near-term support.

Source: IG charts

Source: IG charts

Source: IG charts

Source: IG charts

Tuesday: DJIA -0.55%; S&P 500 -0.41%; Nasdaq -0.74%, DAX +0.87%, FTSE +0.18%

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now