Is there an end in sight for the FTSE 100 turmoil?

Entry posted by MongiIG in Market News

453 views

Fundamental and technical outlook on the FTSE 100 and FTSE 250 amid the sacking of the UK Chancellor of the Exchequer Kwasi Kwarteng.

Source: Bloomberg

Source: Bloomberg

Why are UK stocks in the doldrums?

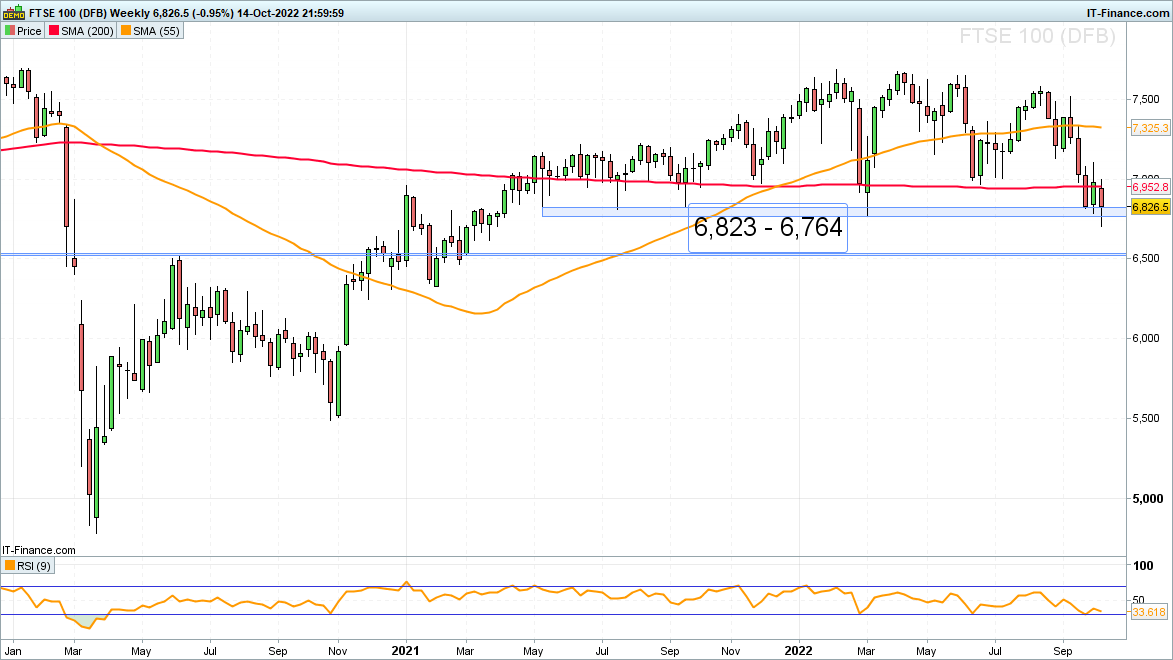

The FTSE 100 and FTSE Mid 250 indices have had a tough year so far, dropping by close to 9% and 29% year-to-date (as of 14/10/2022) respectively, as Liz Truss’ government created additional havoc for UK shareholders amid what the financial markets perceived to be her unfunded mini-budget and largest tax cuts in 50 years three weeks ago.

This pushed UK gilt yields to levels last seen in 2008 during the financial crisis and led to the government’s 30-year borrowing costs to soar above 5% which forced the Bank of England (BoE) to step into markets with an offer to buy up to £65bn of long-term gilts two weeks ago to protect UK pensions, instead of embarking on its quantitative tightening path as had originally been planned.

A few days ago, UK gilt yields rose once more close to their September peaks, with both the FTSE 100 and FTSE 250 continuing their swift descents to multi-year lows.

This renewed turmoil in financial markets brought about the second of the UK government’s U-turns within less than a month with the promised abolition of the corporation tax rise from 19 to 25 percent being scrapped. This follows back peddling on the decrease of the UK higher rate tax band from 45% to 40% only a couple of weeks ago.

Together the elimination of these two tax cuts will save the UK government £2bn and £18bn respectively and will reduce the “mini” budget’s unfunded tax cuts from £45bn to £25bn, prompting a relief rally in UK stocks and pushing UK gilt yields lower.

Another boost for UK stocks came Friday lunchtime as Liz Truss sacked her Chancellor of the Exchequer Kwasi Kwarteng after only 39 days in office, only the second shortest stint since Ian MacLeod in 1970 when he died only a month after taking office, and replacing him with the experienced former culture, health and foreign secretary Jeremy Hunt who, incidentally, supported the prime minister’s rival Rishi Sunak in the Tory leadership battle.

According to the British journalist Stephen Bush on Twitter “the UK conservative party will have had as many chancellors of the exchequer in 2022 as the Labour party has since 1967.”

The UK’s stock market woes have not entirely been of its own making, though, as this year’s declines have been in line with global risk-off sentiment amid soaring inflation, the cost-of-living crisis, the war in Ukraine and rapidly rising central bank interest rate hikes in most developed economies amid a worsening outlook for the world economy which is feared to slip into a recession.

Is the decline in the UK stock market over now that a new chancellor has been appointed?

The fundamental woes mentioned above will remain despite Jeremy Hunt taking over as the UK’s Chancellor of the Exchequer, just as when Kenneth Clarke took over from Norman Lamont who oversaw Black Wednesday in 1992, when the UK government was forced to withdraw sterling from the European Exchange Rate Mechanism (ERM).

The problem is that once a government loses its credibility, it is difficult to regain it. Jeremy Hunt and Liz Truss thus face an uphill struggle, just like the FTSE 100 and FTSE 250 do.

What could help the FTSE 100 and the FTSE 250 recover?

The FTSE 100, which has to a large extent been propped up by its mining, energy and defensive stocks which tend to benefit from an inflationary environment and rising commodity prices, may regain some of this year’s losses as these companies tend to generate more revenue outside the UK, while reporting in pounds (GBP), which further boosts their profits whilst the pound remains under pressure.

Since the UK stock market to a large extent, much like its European counterparts, takes its lead from the US, the third quarter earnings season which began in earnest on Friday with major investment banks such as JPMorgan, Morgan Stanley and Citigroup reporting, should determine the future direction of stock markets, just like US inflation data and the US Federal Reserve's (Fed) monetary tightening stance will.

With regards to the latter, US CPI inflation, despite coming in at a higher-than-expected 8.2% in September versus a year ago, dropped for the third month in a row. Further easing may convince market participants to start buying stocks again as it may lead to less aggressive tightening from the Fed and thus to less of a negative impact on the US economy.

Technical analysis on FTSE 100 and FTSE 250

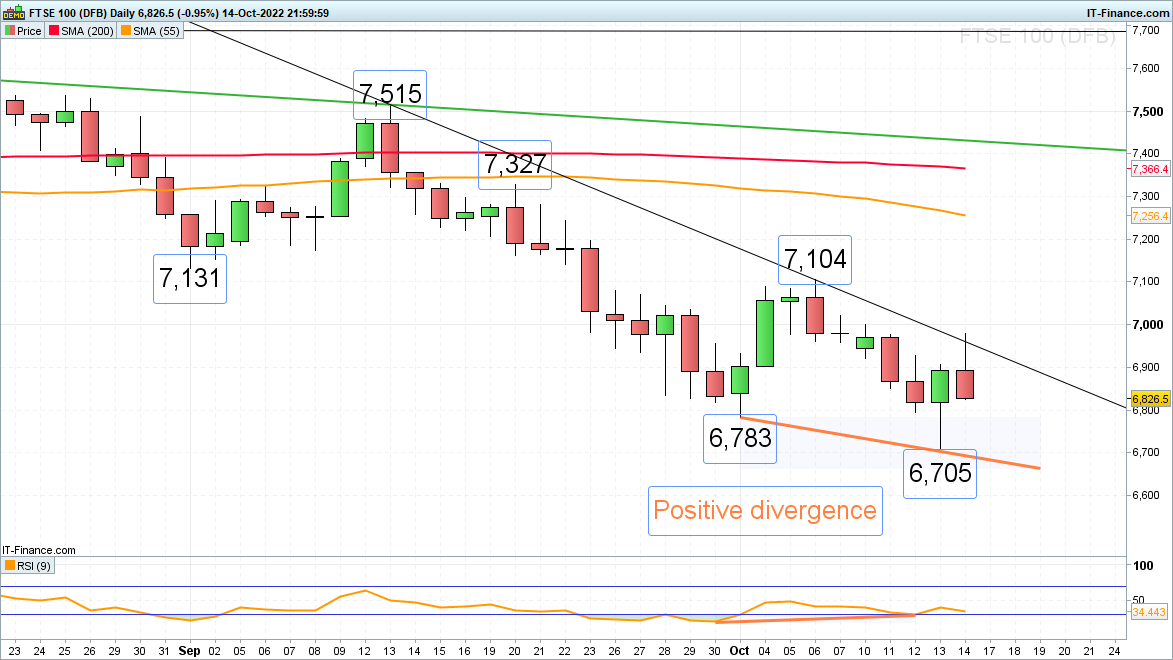

Despite hotter-than-expected US inflation data which initially drove the FTSE 100 to levels last seen in March 2021, the index staged a dramatic bullish reversal late Thursday afternoon.

Source: ProRealTime

Source: ProRealTime

For technical analysts this came as no surprise since market sentiment had been extremely bearish over the last few weeks, short positions were very elevated and because positive divergence could be seen on the daily Relative Strength Index (RSI). It occurs when the index makes a new price low compared to a previous low, but the indicator makes a higher low, thus not confirming the price low and more often than not leads to a bullish reversal in price.

The two-month downtrend line at 6,958 had been retested but capped on Friday. If next week a rise and daily chart close above it were to be seen, the early September low and the early October high at 7,104 to 7,131 would be in focus.

Source: ProRealTime

Source: ProRealTime

Slips should find minor support at the 28 to 29 September lows at 6,835 to 6,828.

While last week’s low at 6,705 underpins, a several days and perhaps weeks long recovery rally might ensue, especially since the FTSE 100 is beginning to enter a time period in which it seasonally tends to outperform into year end. A gradual rise back towards the 200-day simple moving average (SMA) at 7,366 may then also unfold.

Were another down leg to be seen, however, and the 6,705 current October to be slipped through, the November 2016 and December 2018 lows at 6,534 to 6,519 would be pushed to the fore.

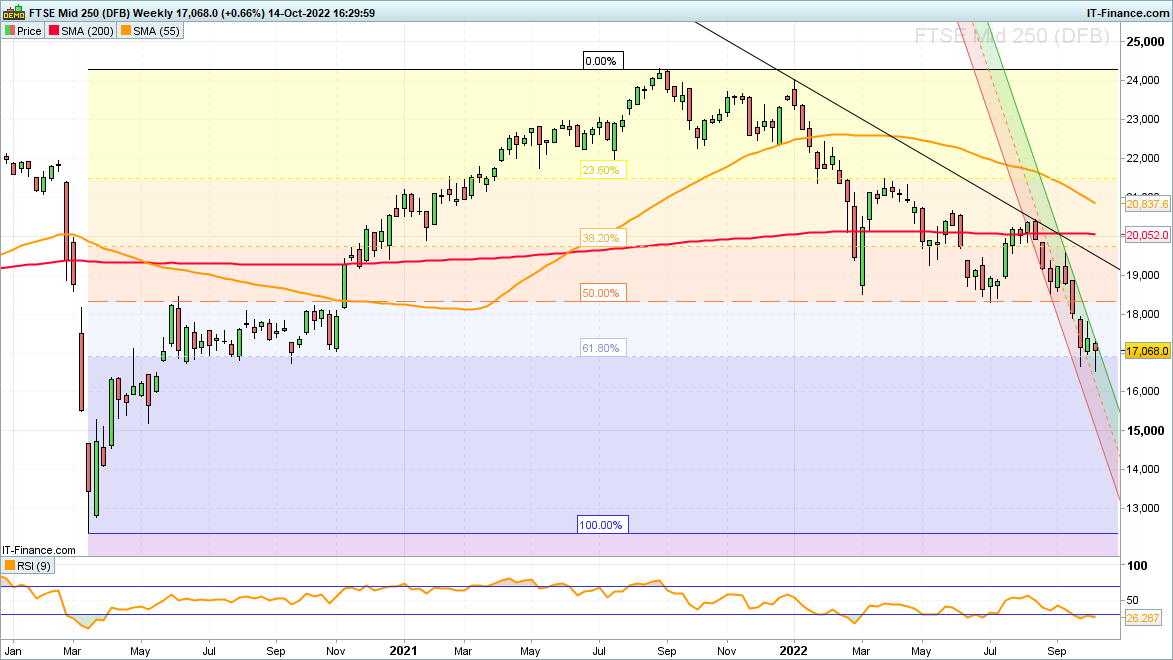

For the FTSE 250, which last week dropped to levels last seen in May 2020, a fall through its current October low at 16,521 would likely engage the May 2020 low at 15,194.

Source: ProRealTime

Source: ProRealTime

As long as last week’s low at 16,521 underpins, however, at least a short-term recovery towards the March and July 2022 lows at 18,289 to 18,509 may ensue, since positive divergence between this week’s price low and the daily Relative Strength Index (RSI) can also be spotted on this index.

Source: ProRealTime

Source: ProRealTime

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now