US jobs preview: ADP signals potential payrolls weakness as traders eye wage growth

Entry posted by MongiIG in Market News

535 views

Friday’s US jobs report could bring further downside for payrolls, with average earnings also expected to decline

Source: Bloomberg

Source: Bloomberg

The December US jobs report is due to be released at 1.30pm, on Friday 3 January (UK time). Coming at the tail end of a week that will have seen monetary policy decisions from the Federal Reserve, European Central Bank, and the Bank of England, this latest report provides the basis on which markets can gauge the direction of travel for the US jobs market and economy. Recent market optimism comes amid heightened hopes of a so-called ‘soft landing’ for the US market, with investors hoping that consumers and businesses manage to take the recently elevated interest rates in their stride.

From a market reaction perspective, there are two areas to focus on. Firstly, the average earnings figure provides a proxy for potential inflation pressures, with any notable uptick in wages bringing fear that the Federal Reserve will have to keep rates higher for longer. However, that would likely strengthen the dollar which has been losing traction in part on the prospect of a swifter dovish pivot than some had previously speculated might be the case. Elsewhere, look out for the payrolls and unemployment figures, with the ability to stave off any particularly notable deterioration on those fronts bringing optimism that a soft landing is indeed upon us. However, the caveat to that is the fact that a strong jobs market brings less pressure on the Fed to cut rates as soon as possible. It is within those boundaries that traders can view Friday’s release.

What do other employment surveys tell us?

It is often useful to look out for clues within alternate employment readings. That can come from several sources, including the ADP, Conference board, Department of Labour, and ADP.

Conference board survey – The latest CB consumer confidence survey saw a strength over the current outlook, but deterioration over the six-month outlook. Within that survey, we saw the number of respondents claiming that jobs were ‘plentiful’ rise from 46.4% to 48.2%. Meanwhile, the number of replies stating that jobs were ‘hard to find’ fell back to 11.3%. This helped widen the gap between the two, which eases fears of an uptick in unemployment. Markets are currently expecting a move from 3.5% to 3.6% unemployment.

JOLTS job openings – The latest JOLTS job openings data (December) portrayed a very similar message, with the latest figure reversing upwards to 11.01 million. That looks to be bringing an end to the declines seen since the March 2022 peak. However, it is worthwhile noting that layoffs and discharges did rise to a one-year low in December.

ISM Manufacturing PMI – This week we are devoid of the crucial services PMI reading which is released after the jobs report. The ISM manufacturing PMI employment segment did decline, but remains in positive territory. Nonetheless, this is of less value given that the majority of the jobs being created are in the services sector currently.

ADP payrolls – The latest ADP payrolls data brought greater concerns for economists, with the figure of 106k coming in well below estimates. That number represents the worst ADP payrolls survey in 10-months. With the ADP calculation having been adjusted, we can see below that there appears to be a closer correlation with the headline figure. Over the course of the past six-months, the average ADP miss has been 44k. To put this in context, the previous six-months missed by an average of 160k. With this in mind, the disappointing 106k ADP figure does highlight a likely figure below the current market expectations of 190k.

Non-farm Payrolls

Friday’s headline non-farm payrolls figure is forecast to fall below the 200k mark for the first time since December 2021, with markets expecting a figure of 190k. The table below highlights how the top five ranked respondents actually predicted figures well above the 200k mark. Whether the ADP release would have changed their view remains to be seen.

Source: Eikon

Source: Eikon

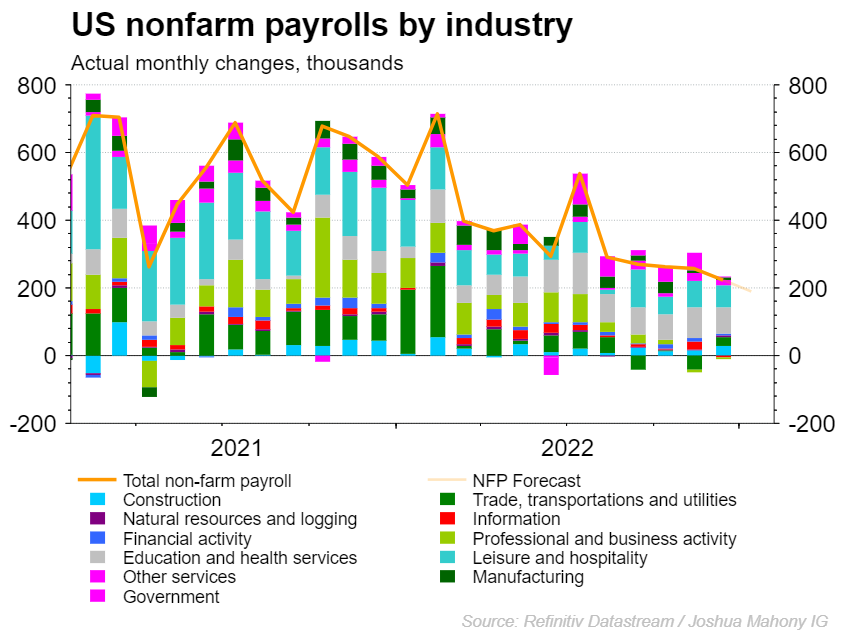

Taking a look at the breakdown of where jobs have been made and lost, it is notable that the trade, transportation, and utilities segment has been contracting twice out of the past four months. Government jobs shrank significantly last month, while Education/health, and leisure/hospitality remain the backbone of jobs growth of late.

Unemployment

As previously mentioned, unemployment is forecast to rise back to 3.6%, remaining within the 3.5%-3.7% range that has dominated for the past 10-months. Thus, unless we see a break from that range, a tick higher would not necessarily spark too much concern for markets.

US average hourly earnings

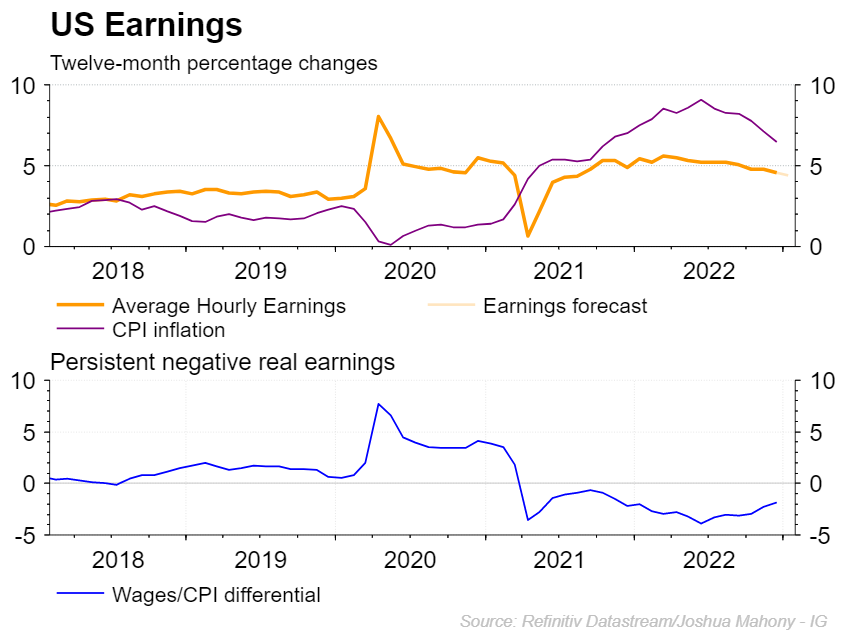

US average hourly earnings have become increasingly important over the course of this crisis, with traders providing a clear association between wages and inflation. Fortunately, we have seen this gauge decline over the course of the past year, although the relatively pedestrian pace of the move means that the differential between CPI and AHE has tightened to the lowest level in over a year. That is a positive development when considering the collapse in real earnings seen in 2022. Nonetheless, the Fed will hope that average hourly earnings will continue to decline to avoid a wage-price spiral that forces businesses to up prices in bid to address rising costs.

Dollar index technical analysis

The dollar has been hit hard over the course of the week, with the FOMC meeting bringing yet another decline for the greenback. The move through 101.10 has brought about a fresh nine-month low, despite the Fed’s insistence that they could yet raise rates further to bring down inflation. That decline brings yet another bearish continuation signal for the dollar. With that in mind, further downside looks likely unless we see price rise through the 102.26 swing-high.

Source: ProRealTime

Source: ProRealTime

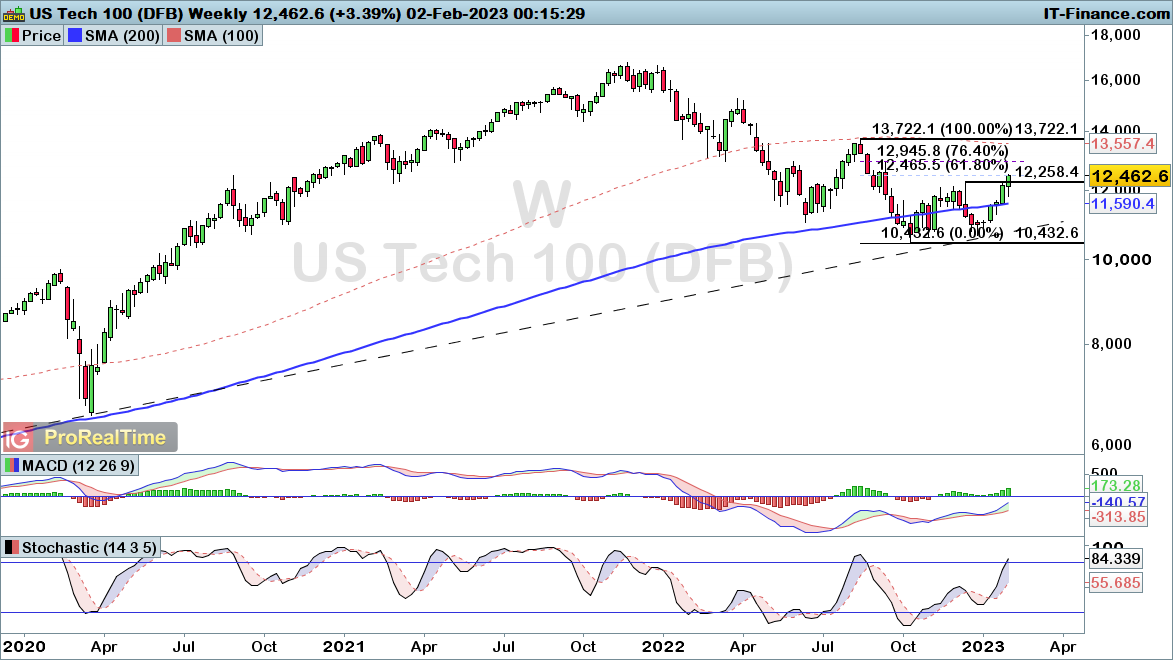

Nasdaq technical analysis

The Nasdaq has managed to push sharply higher this week, bringing a fourth consecutive week of gains for the index. The weekly chart below highlights the potential for Fibonacci resistance up ahead, highlighting the need to watch price action around the key 12465 and 12945 levels.

Source: ProRealTime

Source: ProRealTime

On the intraday charts, we can see a clear pattern of higher highs and lows. The ability to maintain that pattern is key here, with a bullish outlook remaining in play unless we see a move back below 11816.

Source: ProRealTime

Source: ProRealTime

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now