US jobs preview: another strong report looks likely, but Covid-19 concerns cast a shadow

Entry posted by ArvinIG in Analyst article

583 views

The US jobs report looks set for a strong November, with elevated ISM manufacturing and ADP payrolls surveys hinting at another positive month.

Source: Bloomberg

The November US jobs report is due to be released at 1.30pm, on Friday 3 December (UK time). Coming at a time where markets are struggling to gauge exactly which direction things are heading, this forthcoming jobs report looks likely to remind the Federal Reserve (Fed) of the potential for a faster pace of monetary tightening if the Omicron variant proves to be a false alarm.

Undoubtedly, the new Covid-19 variant brings huge economic uncertainty, with the monetary policy picture also likely to depend on whether Omicron leads to stringent lockdown measures and another bout of business closures. In which case, the prospect of sharp market declines and economic struggles will make it difficult for the Fed to continue on a path of monetary tightening despite elevated prices. Nonetheless, with some reports that this latest variant could have less severe symptoms compared with Delta, there is a potential for the economic impact to be less severe. Should that come to fruition, high inflation and strong employment would form the platform to ramp up tapering and drive interest rates higher.

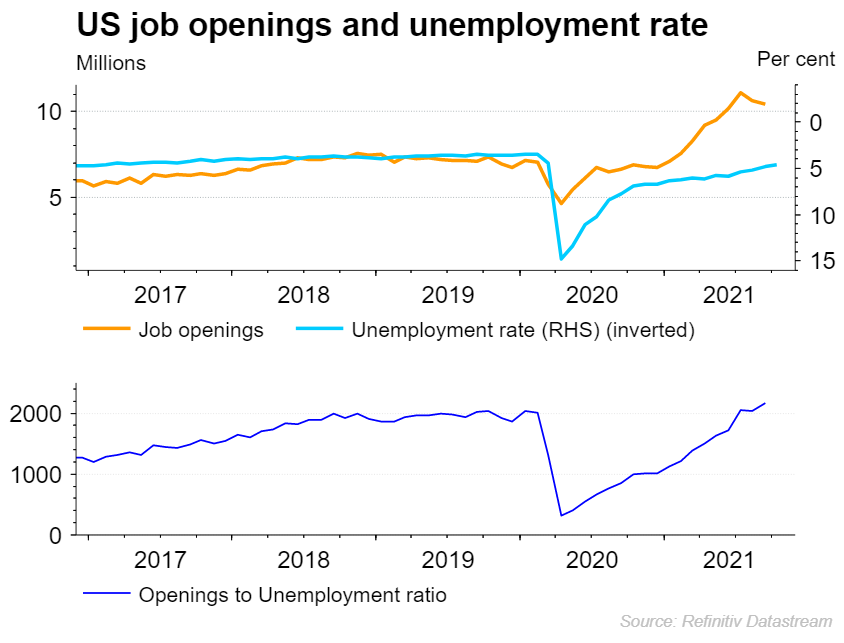

One thing we have seen of late is that the vacancies have rocketed to record levels, allaying any fears that have emerged around volatile payrolls numbers. The chart below highlights how businesses remain committed to hiring new employees, which signals unemployment as largely a misalignment of jobseekers and employers. The ratio between job seekers and job openings are back to pre-pandemic levels, negating much of the fear around any payrolls volatility.

Source: Refinitiv

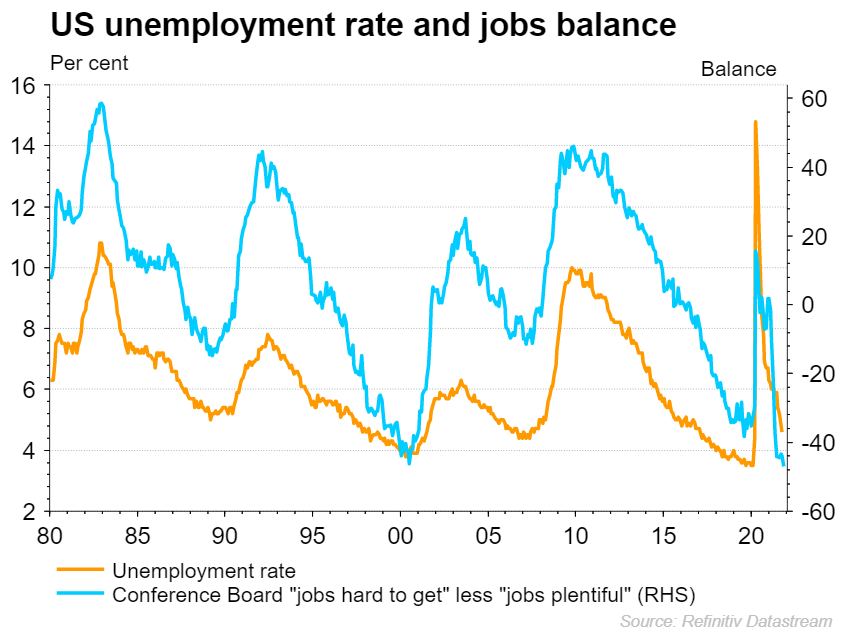

Taking a look at the latest ‘Conference board’ survey, we can see that the ratio between individuals finding employment “hard to find” compared with ‘plentiful’ continued to decline,. That took the ratio into a fresh record lows, highlighting the positive jobs picture in the US.

Source: Refinitiv

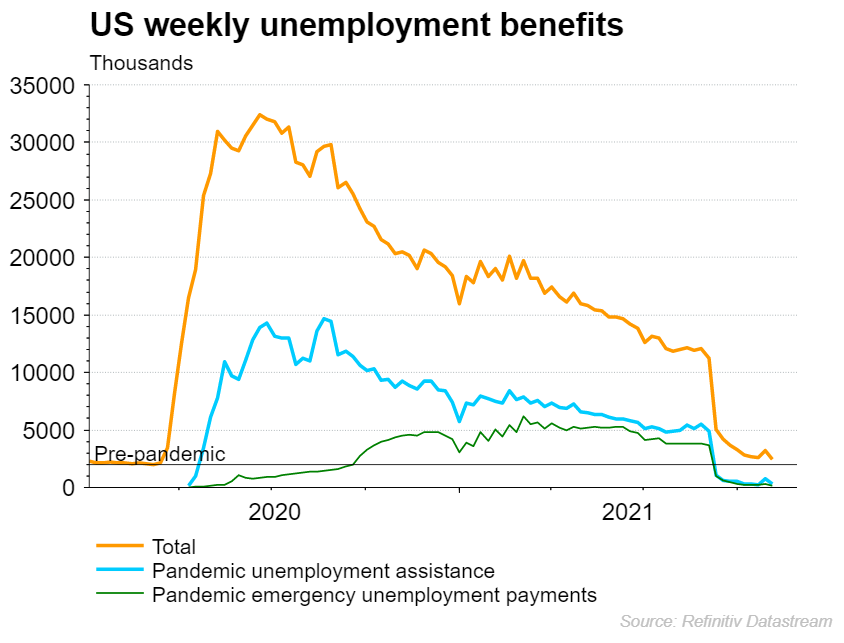

With government benefits having finally dropped off, there is little incentive to hold off on finding a job if unemployed. That could help drive the jobless into roles, which may not have been the case previously. As such, it would make sense that we could see strong downside for the unemployment this time around. Last month saw unemployment fall more than expected, and we could see something similar on Friday.

Source: Refinitiv

What do other employment surveys tell us?

It is often useful to look out for clues within alternate employment readings, with the ADP, jobless claims, and Institute for Supply Management (ISM) manufacturing purchasing managers index (PMI) all worth analysing ahead of the main event.

ADP payrolls

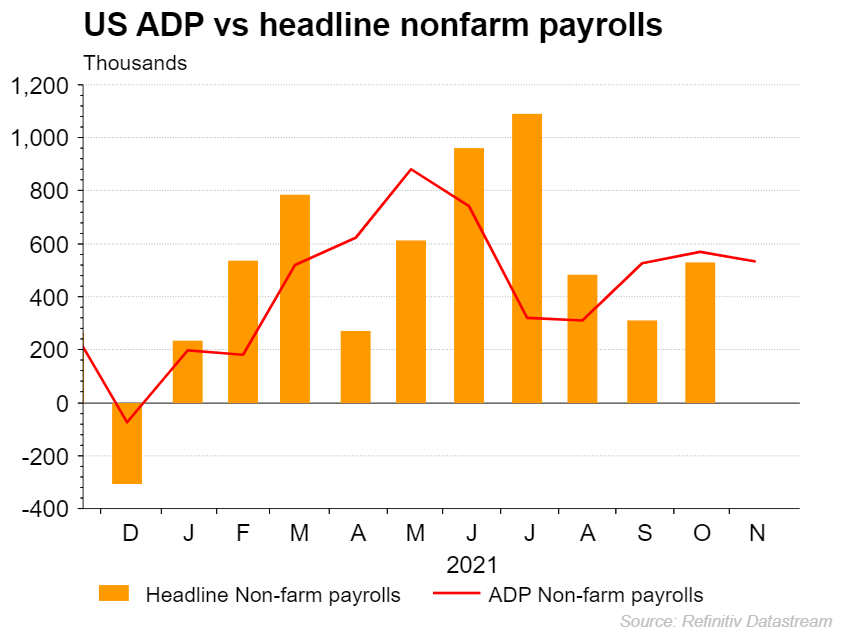

Wednesday’s ADP payrolls figure for November came in at 534,000, which stook slightly below the October reading of 570,000. While some refute the relationship between the ADP and headline payrolls readings, they can often provide a good general direction of travel. With that in mind, the fact that we have seen another ADP reading over 500,000 does support the notion that payrolls will post another strong number on Friday.

Source: Refinitiv

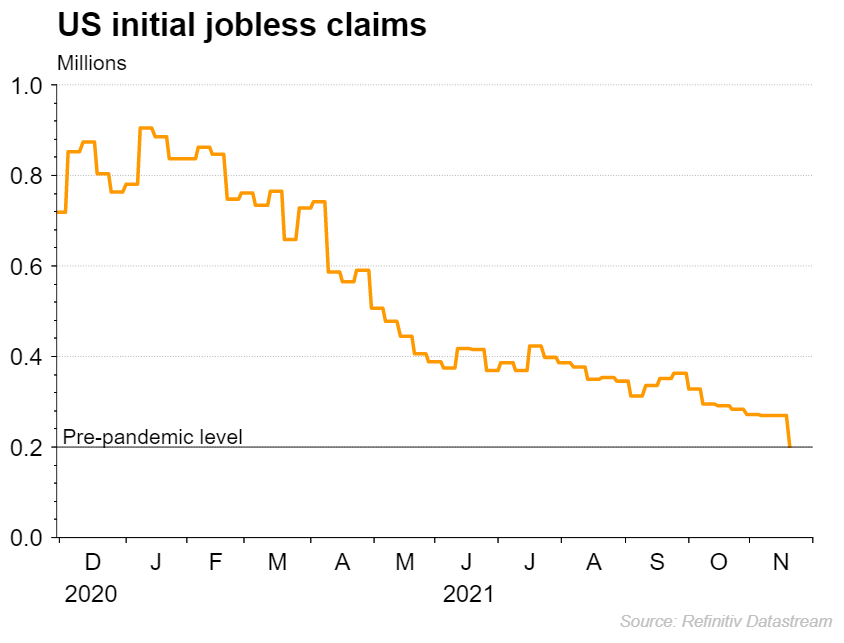

Initial jobless claims

Initial claims saw another sharp move lower last month, with the indicator falling back into pre-pandemic levels. This provides greater confidence that we are not on experiencing a jobs market shock that could impact the payrolls figure.

Source: Refinitiv

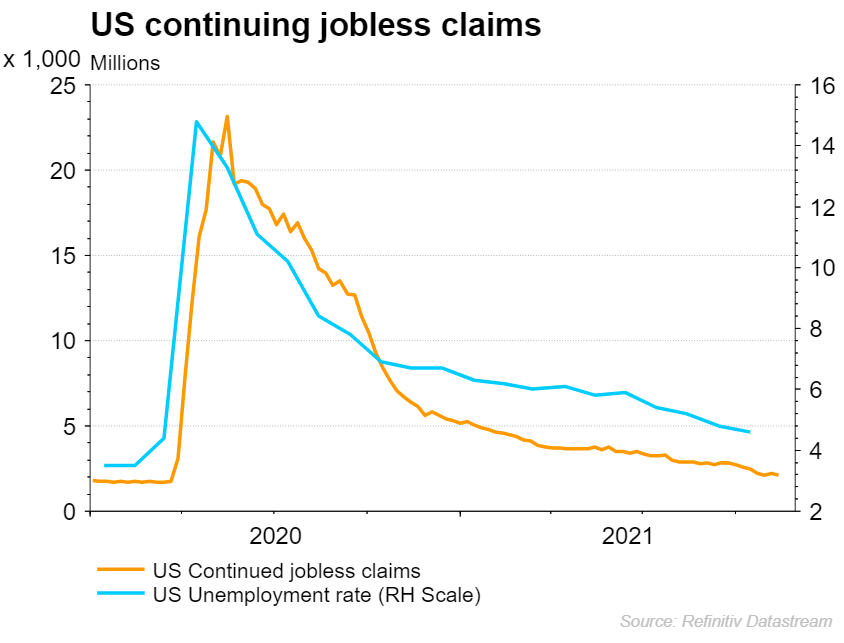

Continuing jobless claims

Continuing claims provides us with a good proxy for unemployment, with the latest surveys supporting the idea that unemployment will head lower on Friday.

Source: Refinitiv

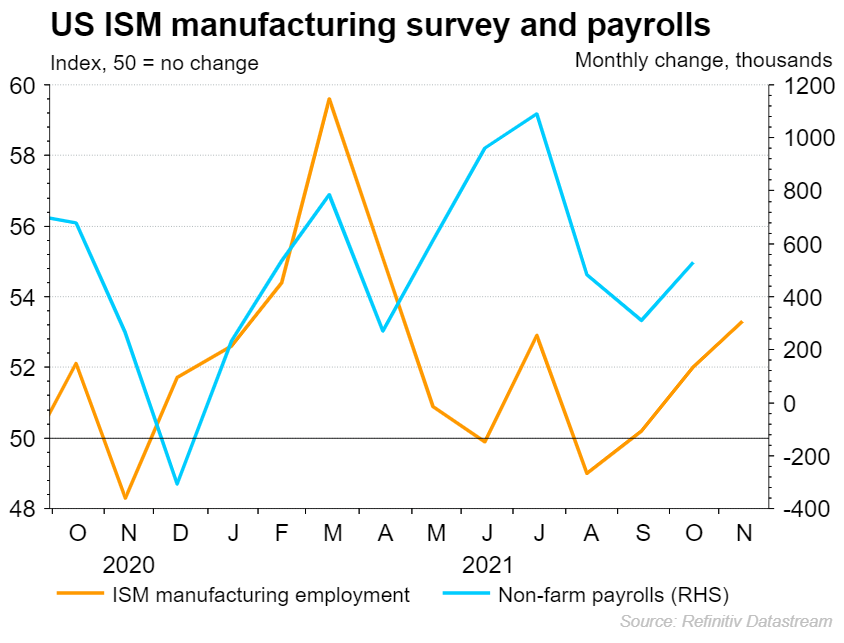

ISM manufacturing PMI

The latest ISM manufacturing PMI saw another improved reading for the employment element. With the employment PMI figure rising to a seven-month high of 53.3, it is clear that the manufacturing sector is enjoying continued improvements in November. Unfortunately, the services sector ISM PMI is not released until Friday afternoon.

Source: Refinitiv

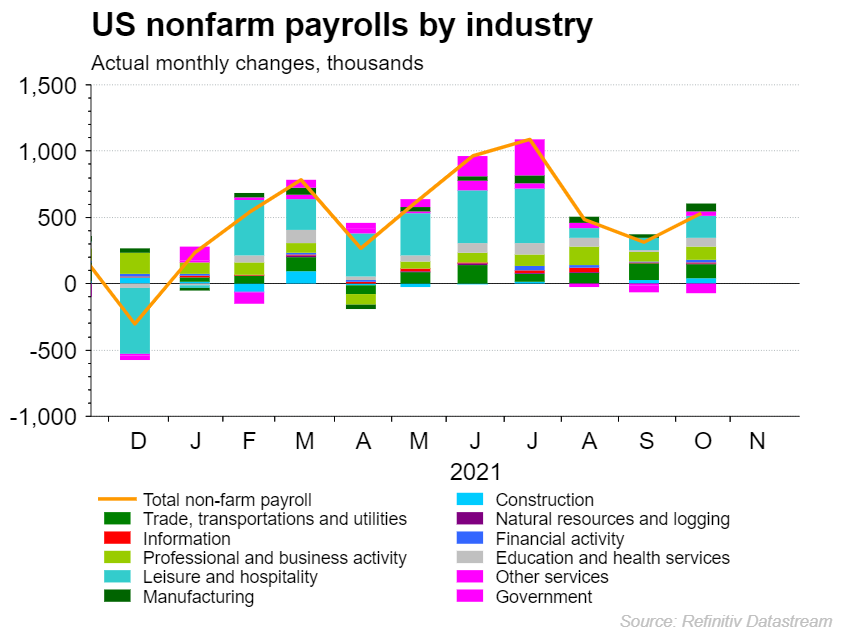

Non-farm payrolls

Last month saw a welcome boost for the headline payrolls figure, with a reading of 531,000 representing the highest figure in three-months. Notably, the services sector accounted for much of that October rebound. On this occasion, markets are expecting a figure around 550,000.

Source: Refinitiv

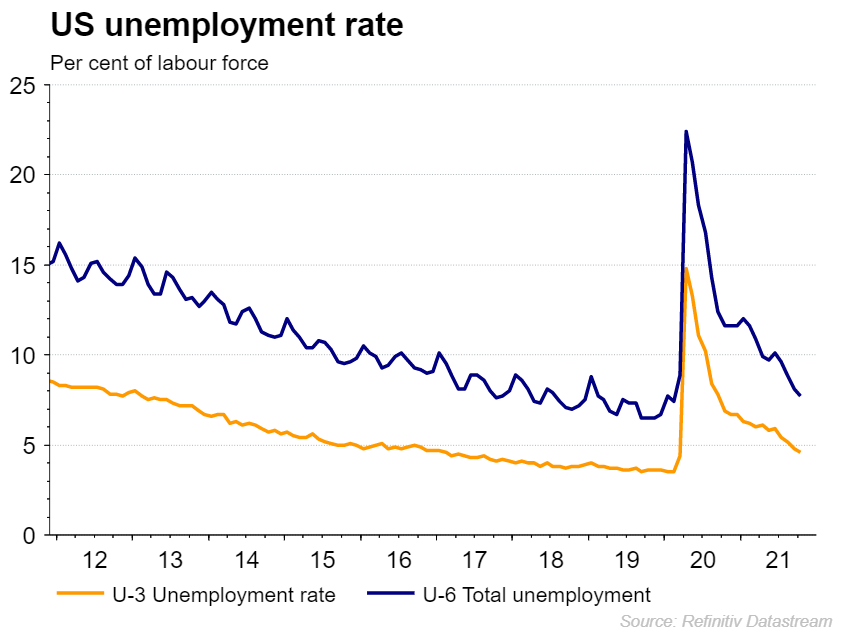

Unemployment

From an unemployment perspective, the downward trajectory remains in place after a welcome drop down to 4.6% last month. As we have seen, both the continuing claims, and the conference board ratio, signal the potential for further downside to come. Elevated job openings coupled with a drop off in government benefits provide the environment where further reductions in unemployment look highly likely.

As things stand, U-3 unemployment (headline) is expected to decline to 4.5%. However, with a low participation rate, it also makes sense to keep an eye out for the wider U-6 measure of unemployment which provides a more comprehensive gauge accounting for many that would have dropped out of the headline reading.

Source: Refinitiv

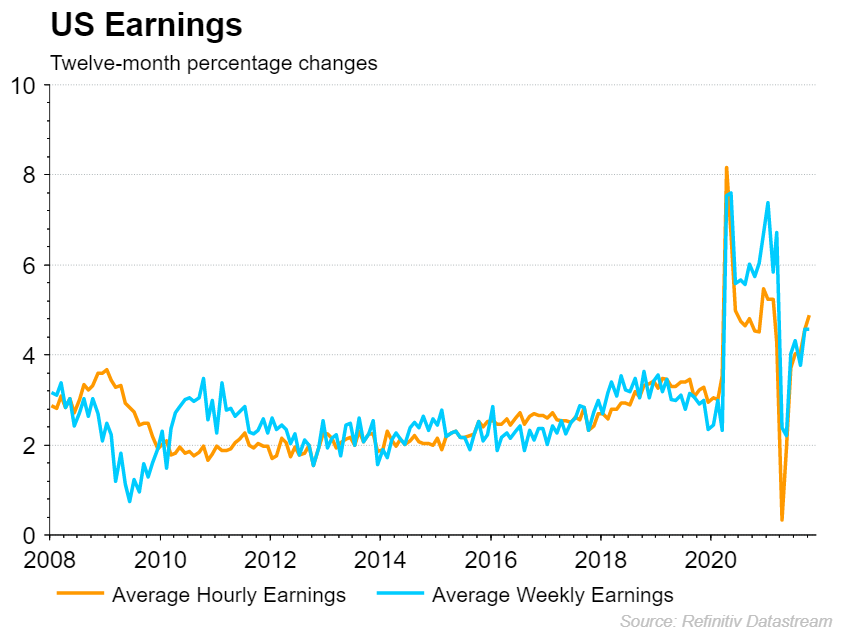

Wages

US earnings remain elevated, providing further ground for higher inflation. The annual average earnings figure stands at 4.9%, but the elevated level of vacancies do support further upside. Markets are expecting a figure of 5%.

Source: Refinitiv

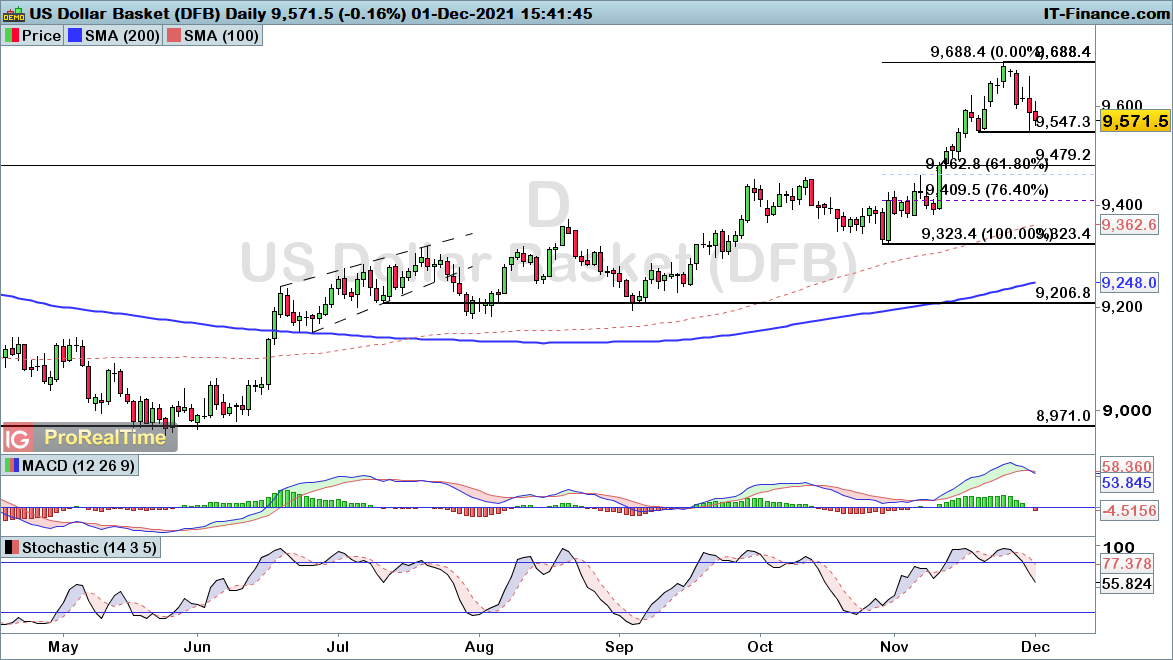

Dollar index technical analysis

The dollar index has been hit hard after a repricing of expectations for tighter monetary policy. Until we know the true economic repercussions from this latest Covid-19 variant, we are likely to see traders second guess the Fed outlook going forward.

A strong jobs report could help build the case for tighter monetary policy, but always remember that the Omicron updates will play the dominant role in dictating markets over the coming weeks. Near-term support comes in the form of the 95.47 swing low, which if broken would lead to a wider retracement of the 92.23 to 96.88 rally. Nonetheless, the wider uptrend does remain intact, with the bulls likely to come back in a meaningful way should Omicron fears turn out to be overblown.

Source: ProRealTime

DJIA technical analysis

The Dow Jones has also been under pressure of late, with traders caught between the potential for monetary tightening or Covid-19 restrictions.

We do still remain within an uptrend despite the price having slipped back into the 200-day simple moving average (SMA). This points towards a heightened risk of a wider reversal for index in the event that price falls below 3353. Until then, the uptrend does still remain intact.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now