Where next for Alphabet shares post Q1 results?

Entry posted by MongiIG in Market News

1,353 views

Now that Alphabet’s Q1 earnings and revenue are out of the way, what does the company’s share price potential look like when buying it at current discounted levels?

Source: Bloomberg

Source: Bloomberg

Alphabet share price

Last week, Google parent company Alphabet’s share price dropped significantly after missing expectations for earnings and revenue.

However, as the stock trades at around 20% discount year-to-date, many investors are wondering whether now might be the right time to buy it, especially given its large share buybacks underpinning the share price.

Alphabet last week said that its board of directors authorised $70 billion in share repurchases, which is a major increase from last year’s $50 billion and the $25 billion in 2019. The announcement is a significant acceleration in Alphabet’s strategy to return capital to shareholders through share buybacks.

The innovator is among the large cap tech stocks that have been suffering post-earnings, but it is continuing to invest economically in growth versus its peers. Overall, the company has a unique asset base distributed across numerous internet businesses that should support its long-term growth and profits.

Alphabet earned almost $70 billion in revenue for the first quarter (Q1) of the year, showing its financial strength and consistent revenue growth among its portfolio of properties. The company's revenue increased by 23% year-on-year (YoY) as it managed to keep its operating margin constant with strong operating income increases from almost $16.5 billion to around $20 billion.

Cloud, one of its largest new business segments, saw almost 50% growth, while Google Search, YouTube, and other business segments showed strong growth as well. It's worth noting that, despite the revenue, the company's other investments took an annualised loss of $5 billion. These have remained fairly constant over the years, though, again displaying the company's financial strength.

Alphabet thus seems to retain future earnings growth potential while it sits on a roughly $170 billion cash pile and has minimal debt, giving it the ability to opportunistically look at further acquisitions, capital-intensive projects, or simply weather a downturn.

Despite the recent weakness in technology stocks, with many still seen as substantially overvalued, Alphabet seems to be in a stronger position than its peers since it has a reasonable P/E ratio in the low 20s, backed up by double-digit revenue growth and even faster earnings growth.

Source: ProRealTime

Source: ProRealTime

What about the technical outlook?

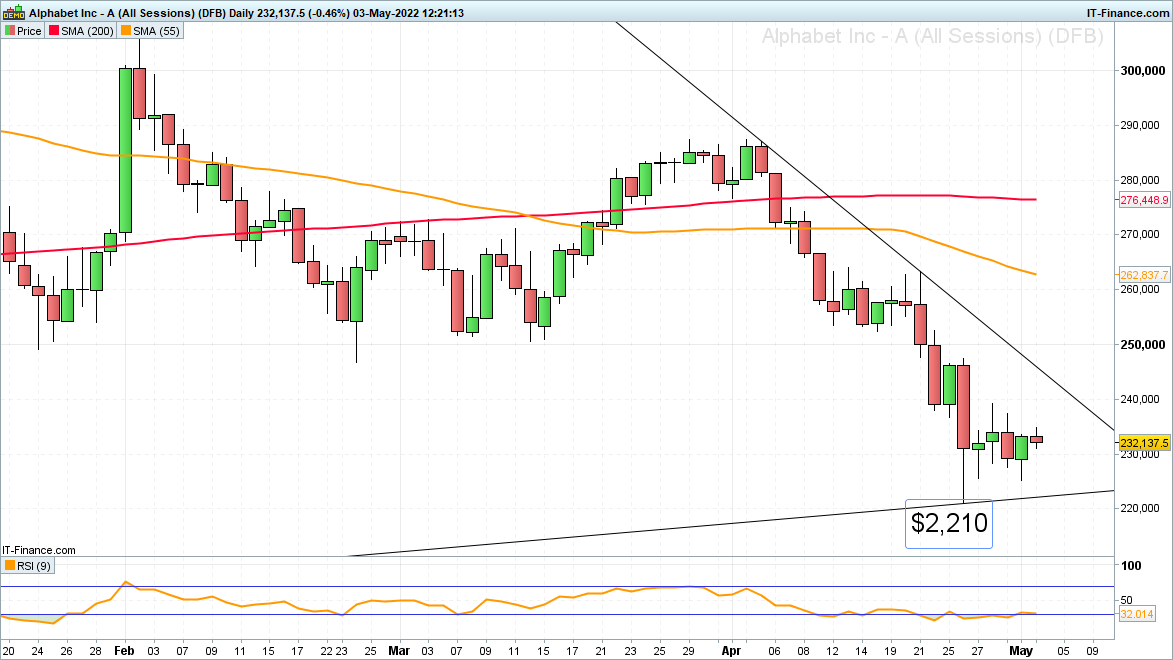

With Alphabet shares trading at one-year lows and around 25% lower than their August 2021 high, on the face of it they seem to offer a great opportunity to go long, having last week formed a minor low at $2,210, not far above the February 2021 high and May 2021 low at $2,182 to $2,145.

While this support zone underpins the share price, a double zig-zag Elliott wave corrective move lower from last year’s highs may be forming which should then be followed by a resumption of its long-term uptrend.

Source: ProRealTime

Source: ProRealTime

The first upside target zone is seen between the July 2021, January, February, and March 2022 lows at $2,466 to $2,505. This resistance area would need to be exceeded for a rise back to the 200-day simple moving average (SMA) at $2,764 to ensue. The bulls would be firmly back in control on a rise above the $2,874 March peak.

Were a drop through the February 2021 high and May 2021 low at $2,182 to $2,145 to be seen, however, the area between the 50% retracement of the 2020-to-2022 and the February-to-March 2021 lows at $2,044 to $1,992 would be targeted.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now