Disney's share price falls post-results release

Entry posted by MongiIG in Market News

1,362 views

Disney's share has fallen into results, although parks and experiences returns to profitability and subscribers to streaming services increase.

Source: Bloomberg

Source: Bloomberg

Walt Disney Company

The Walt Disney Company has released results for the second fiscal quarter (Q2 2022) and six months (1H22) ending 2 April 2022.

The financial highlights from the company are as follows:

- Revenues for the quarter and six months grew 23% and 29%, respectively

- Diluted earnings per share (EPS) from continuing operations for the quarter decreased to $0.26 from $0.50 in the prior-year quarter

- Diluted EPS for the quarter increased to $1.08 from $0.79 in the prior-year quarter

- EPS from continuing operations for the six months ended April 2, 2022 increased to $0.89 from $0.52 in the prior-year period

- EPS for the six months increased to $2.14 from $1.11 in the prior-year period

Streaming costs weigh on Disney’s income although subscriber numbers grow

Disney’s Media and Entertainment Distribution segment saw a 9% increase in year-on-year revenue for the quarter, although the group's operating income from this division fell 32% from the prior year’s comparative period.

The direct-to-consumer sub-sector, which includes ESPN+, Disney+ and Hulu streaming services, saw its operating loss increase from $0.3 billion in the second quarter (Q2) of 2021 to $0.9bn in Q2 2022.

However, while we have seen increased production and expansion costs weighing on profitability, the group has managed to increase subscriber numbers for the quarter.

Disney+ saw a 33% year-on-year increase to total 137.7 million subscribers, ESPN+ a 62% increase to reach 22.3m subscribers and Hulu a 10% increase to total 45.6m subscribers.

Disney’s Parks, Experiences and Products segments return to profitability

The Disney Parks, Experiences and Products segment saw operating income improve dramatically to $1.75bn in Q2 2022 from an operating loss of $406m in the prior year’s comparative period.

The return to profitability was primary driven by the company’s domestic parks and experiences operations, although the reported operating loss from its international operations also improved (by 29%) from the comparative quarter last year.

The international parks and experiences operations are expected to find renewed pressure in the upcoming quarter on the back of hard lockdown restrictions in Asia.

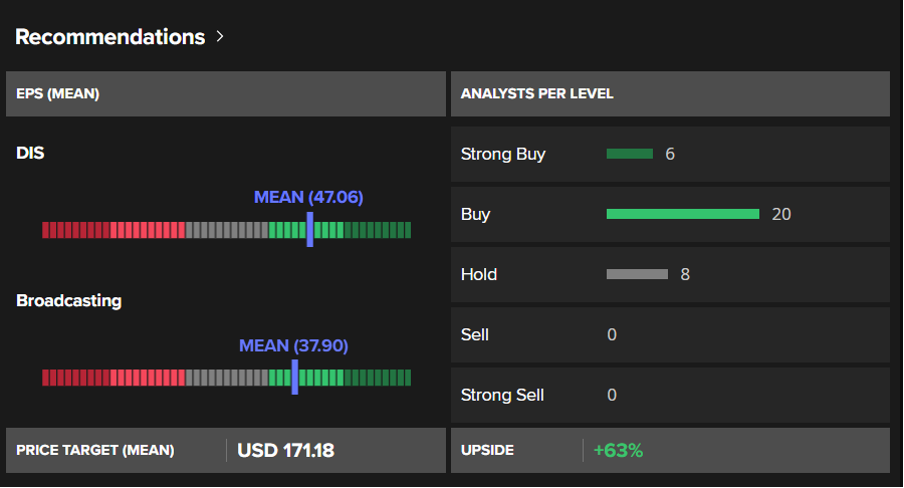

Broker price targets and ratings changes for Disney

Following the results release we have seen some re-ratings and affirmations of the stock, a summary of which is as follows:

- Credit Suisse has maintained an outperform rating

- Keybanc has maintained an overweight rating

- Guggenheim has cut the target price for the Disney share price from $150 to $110

- Rosenblatt has cut the target price for the Disney share price from $177 to $174

- Bank of America Global Research has cut their price target from $191 to $140

- MoffetNathanson has cut their price target from $130 to $125

Source: Refinitiv

Source: Refinitiv

As of the 12th of May 2022 a Refinitiv consensus of 34 broker ratings continue to suggest a ‘buy’ on the stock, with a long-term price target mean of $171.18.

The long-term price target suggests that the current price of The Walt Disney Company trades at a 63.% discount to a longer term fair value assumption.

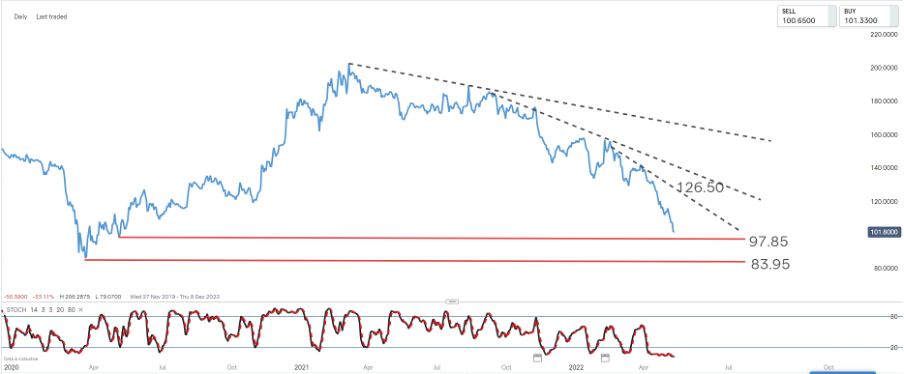

The Walt Disney Company – technical view

Source: ProRealTime

Source: ProRealTime

The share price of Disney has continued to fall partly in lieu of the global selloff in equities we have seen.

The price is currently approaching historical support at the $97.85 level, a break of which (confirmed with a close) would further target $83.95 as the next level of support. The steepening trendlines do, however, suggest that the accelerating downtrend might be reaching a point of capitulation. This is further supported by the share having traded in oversold territory for a prolonged period.

Should a rebound occur from oversold territory, trendline resistance at 126.50 provides an upside target for the share price. However, in lieu of the longer term downtrend which remains in play, our preference is to look for short entry into a rebound, until such time as at least trendline resistance is broken.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now