US jobs preview: Are we seeking the beginning of an unemployment surge?

Entry posted by MongiIG in Market News

470 views

The US jobs report provides the latest batch of data for the Federal Reserve, with unemployment and wages particularly important going forward

Source: Bloomberg

Source: Bloomberg

The September US jobs report is due to be released at 1.30pm, on Friday 7 October (UK time). Coming amidst an inflation fuelled crisis, markets look towards this coming jobs report as a signal of economic difficulties that have thus far been absent. While we continue to see prices rise, employment has largely been solid, thus allowing the Federal Reserve to continue tightening without major cause for concern. However, traders will be keeping a close eye on developments as significant gains in earnings growth or unemployment could bring about a shift in dynamics over the inflation and monetary policy outlook.

What do other employment surveys tell us?

It is often useful to look out for clues within alternate employment readings, with the ADP, Conference board survey, jobless claims, and ISM PMI survey all worth analysing ahead of the main event.

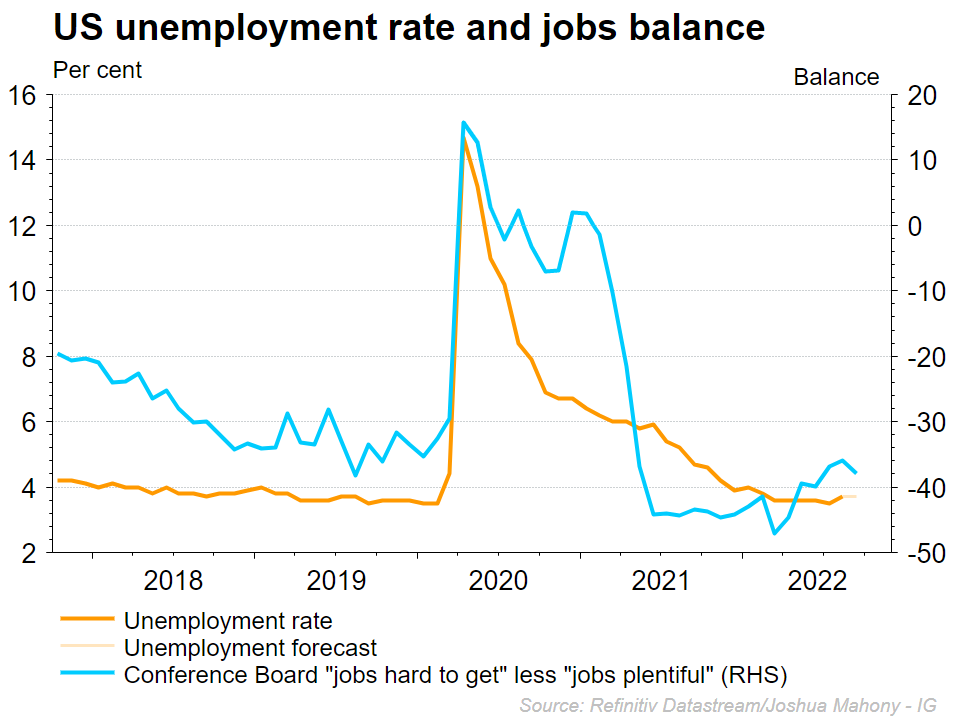

Conference board survey – The latest CB consumer confidence survey has seen a notable shift in the employment outlook, with the percent of those seeing jobs as “plentiful” rising sharply from 47.6% to 49.4%. Meanwhile, we have seen a slight decline in the number of those seeing jobs as “hard to get”. The ratio between those two has subsequently declined, easing fears around an impending upward swing in unemployment.

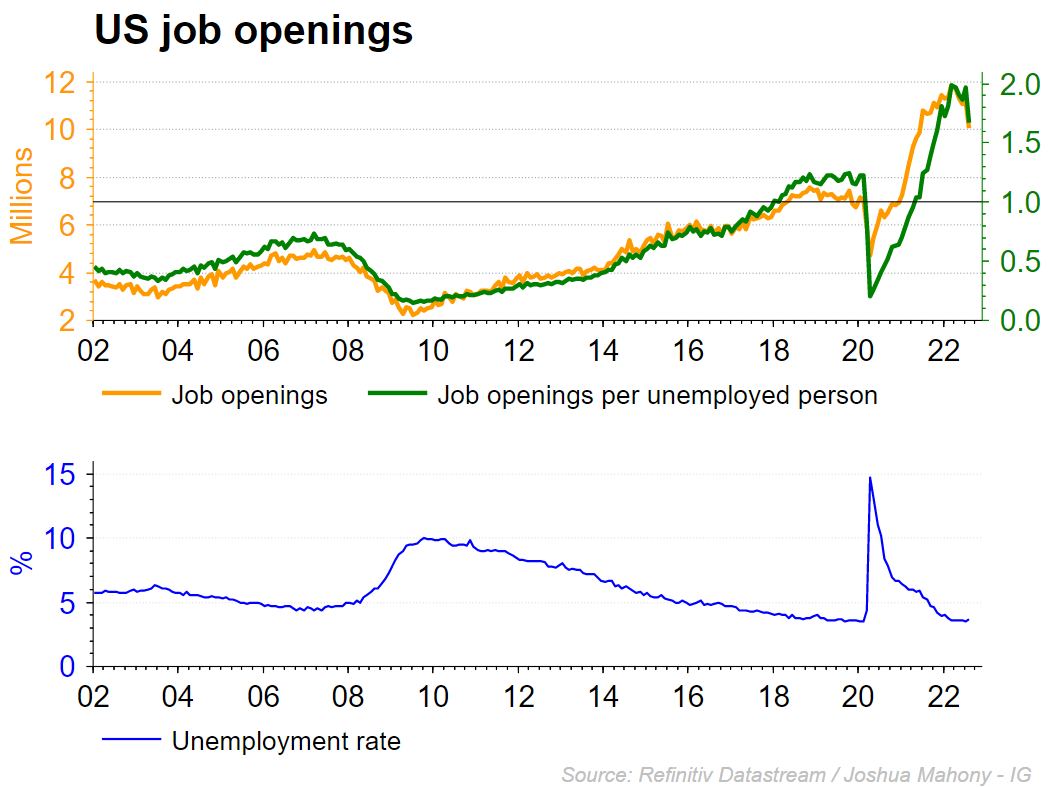

JOLTS job openings – This month has provided us with a worrying collapse in job openings, with the number of openings falling by 1.1 million in August alone. The chart below highlights how this could be a precursor to an uptick in job losses, with a strong negative correlation bringing expectations of an upward reversal in unemployment. It is also worth noting this sharp decline in openings has a significant impact on the trajectory of the ‘job openings per unemployed persons’ metric, which is followed by the Federal Reserve.

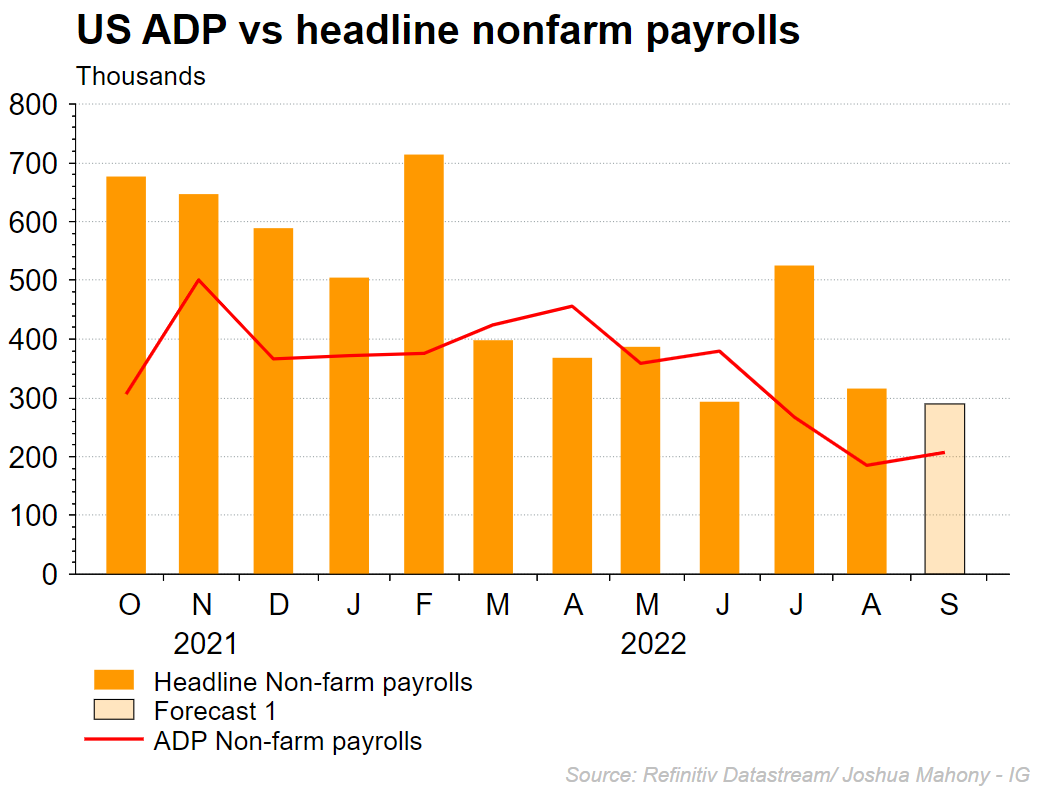

ADP payrolls – The ADP employment survey has provided a welcome rise in payrolls this month, with the figure of 208k representing an improvement on the previous figure of 185k (revised up from 132k). Having beat market expectations, this could signal the potential for an upward move for Friday’s headline NFP figure. Given the recent reconfiguration of the ADP survey, we are yet to see whether this is an improvement in its ability to guide us on where the official figure moves.

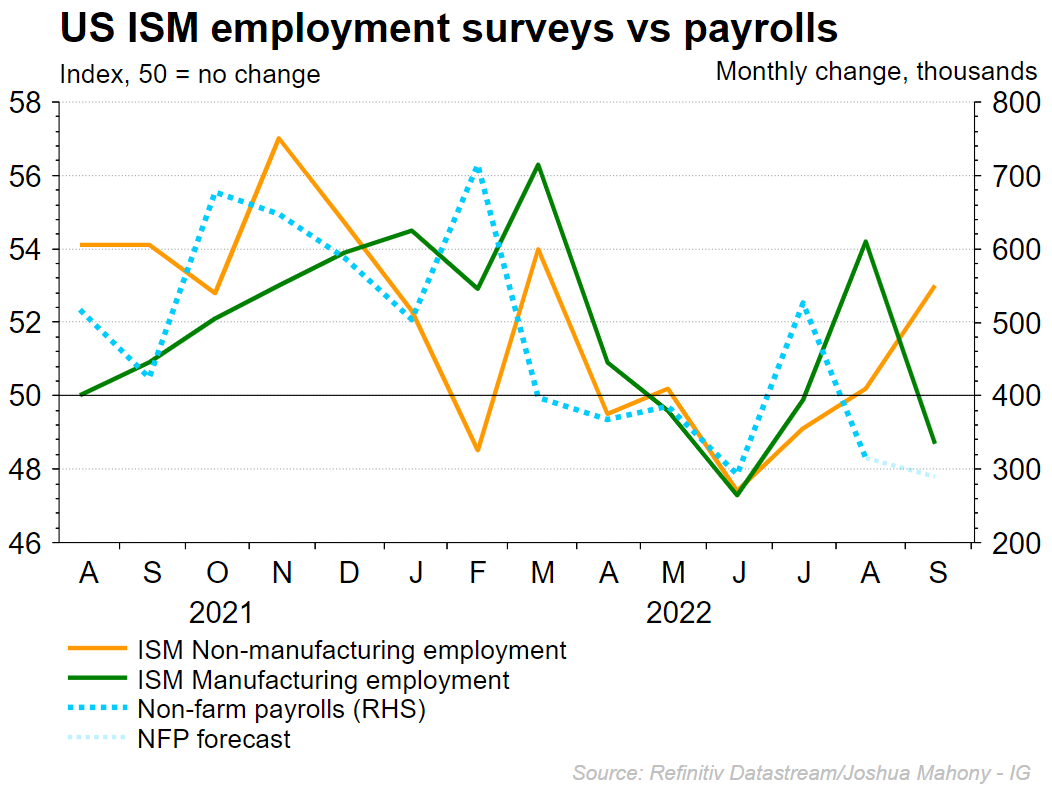

ISM PMI surveys – This month has seen a notable divergence in the ISM PMI surveys, with continued weakness in manufacturing growth standing in stark contrast to the continued strength in services. Crucially, this has also fed through into the employment elements of both reports, with manufacturing moving sharply below the 50 threshold as services surged from 50.2 to 53.0. This signals potential strength for the upcoming payrolls figure, with the vast majority of the NFP movements coming from services post-Covid.

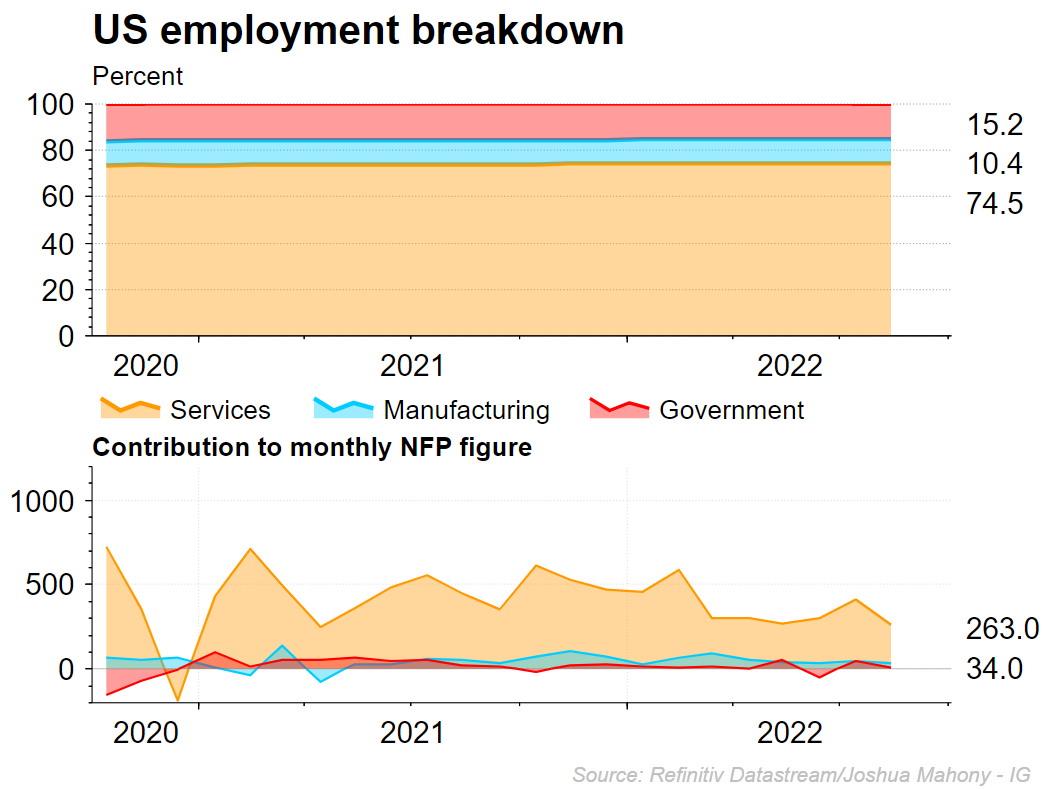

That employment breakdown can be seen below, with the vast majority of the jobs being created coming from the services sector. This means we should pay particularly close attention to the services PMI reading, which provides grounds for optimism given the strength of the latest ISM services employment gauge.

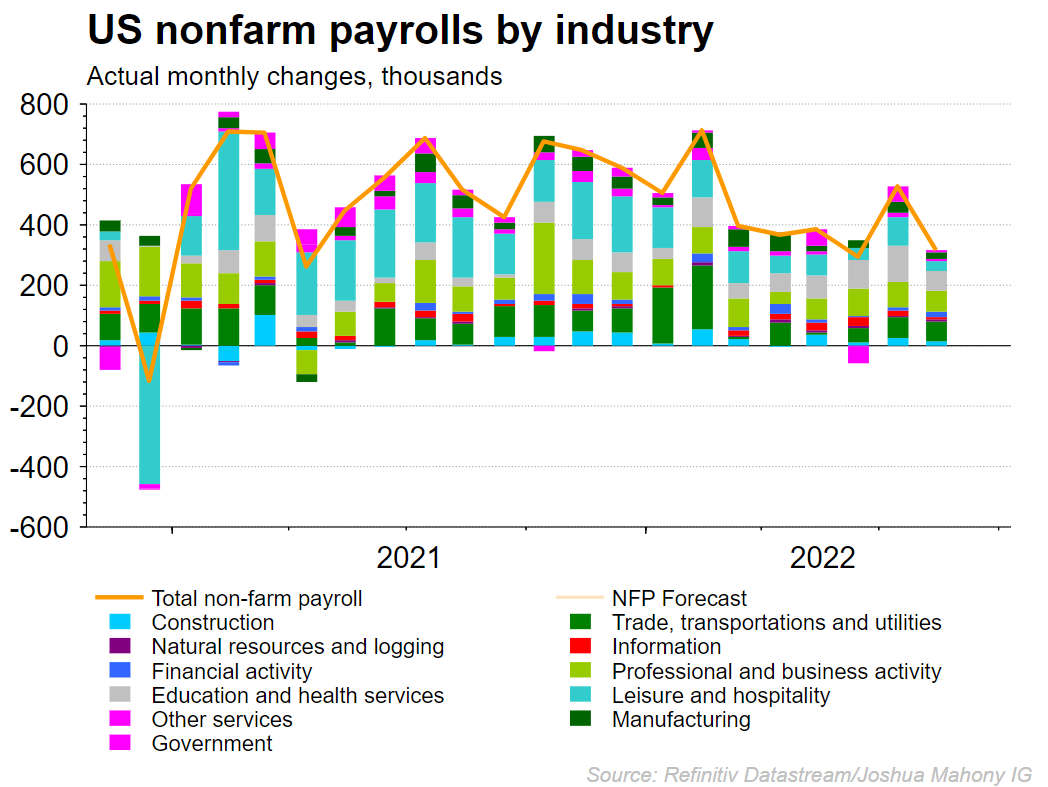

Non-farm Payrolls

The headline non-farm payrolls figure is expected to head lower this month, with predictions of a 290k figure following the 315k figure for August. That would represent the worst payrolls figure in nine-month, signalling that some of the heat is coming out of the jobs market. Nonetheless, with the ISM PMI services reading doing so well, it could point towards a potential better-than-expected figure.

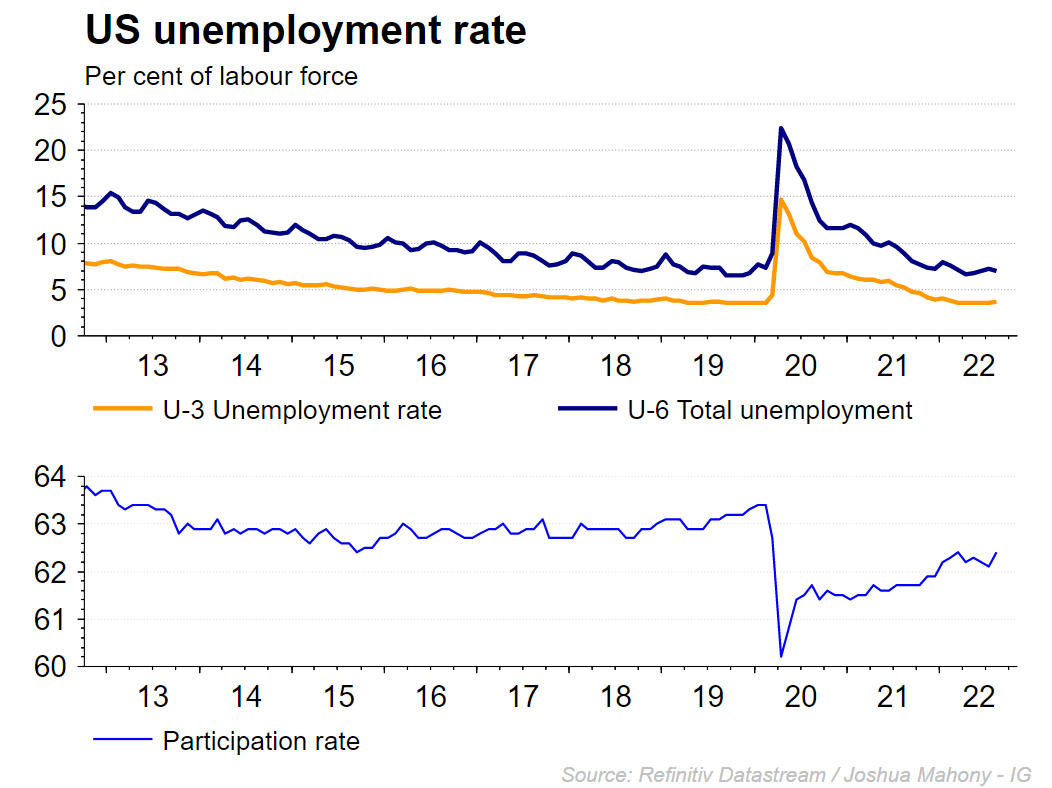

Unemployment

The unemployment rate will be watched closely at this meeting, with last month’s 0.2% rise providing the first tentative signal of an impending rise in joblessness since this crisis began. In fact, the last time we saw unemployment rise for two consecutive months was at the height of the Covid pandemic in early-2020. This month markets are expecting to see unemployment remain at 3.7%, but the reversal in the CB ratio and JOLTS data mentioned above does provide grounds for a potential upturn in unemployment.

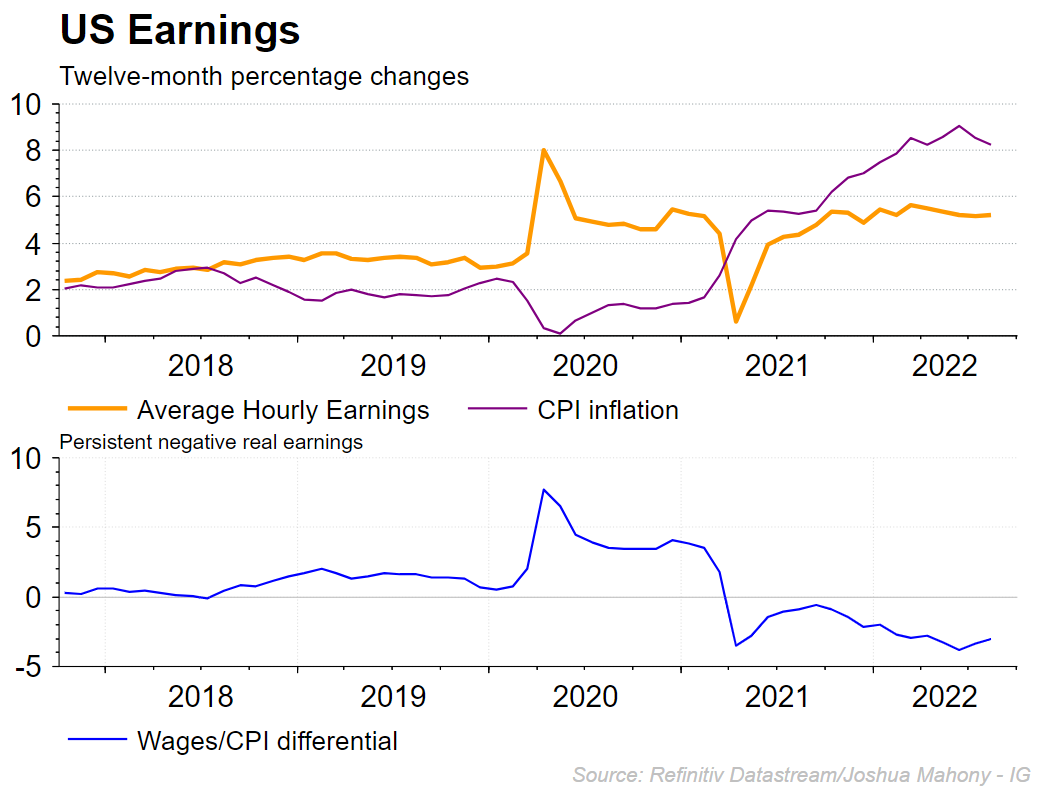

US average hourly earnings

US earnings will continue to be a key factor for traders, with inflation remaining the key indicator that will drive monetary policy going forward. Signs that we will see stubbornly high inflation due to elevated costs could have a major impact on sentiment and market pricing. The chart below highlights that we are thankfully not seeing wages keep up with inflation, with recent earnings data signalling that it could be topping out since the March figure of 5.6%. This is expected to continue, with the September figure expected to come in at 5.2% once again.

Participation rate

The participation rate is a key metric to follow, with rising prices expected to push labour force participation higher. Interestingly, we usually see unemployment and participation move in opposite directions as we can see below. However, with the potential for a rise in unemployment, there is a good chance that the participation rate rises which actually provides the basis for higher U3 unemployment. Crucially, last month highlighted how we can see unemployment rise when the participation rate introduced a new batch of jobseekers into the workplace.

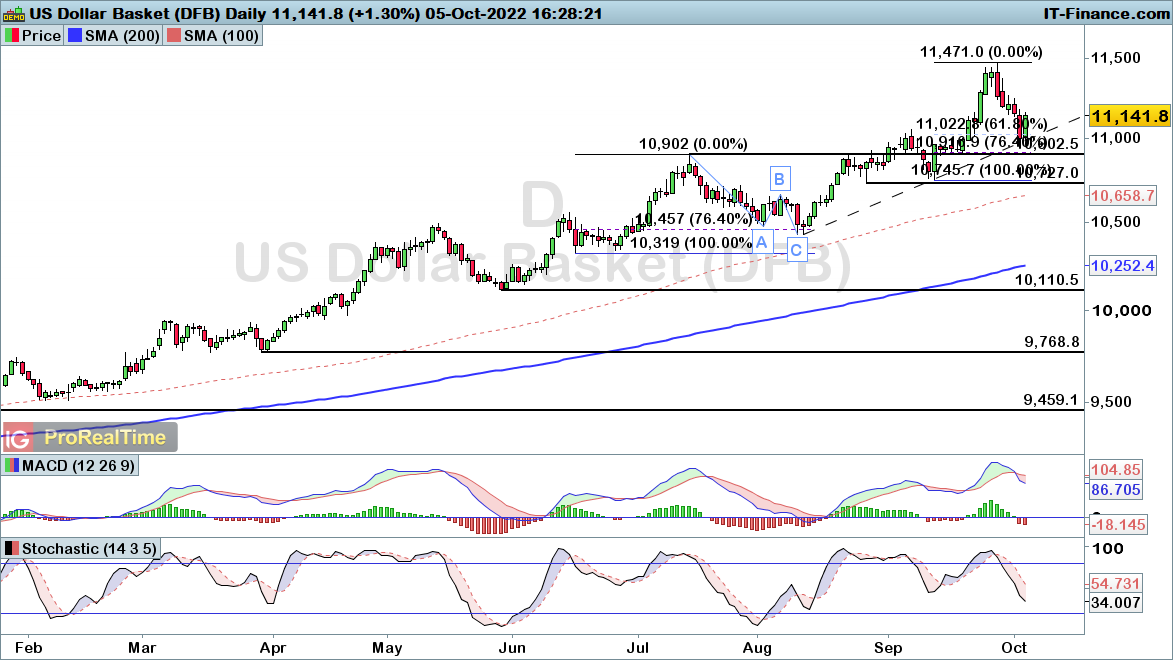

Dollar index technical analysis

The dollar has seen a bout of countertrend weakness in the lead up to this jobs report, with the dollar index falling back into the 110 mark. Crucially, that has provided us with a deep retracement which appears to have ended at an ascending trendline. With a clear uptrend expected to push higher, a bullish outlook holds unless we see price fall back below the 107.45 support level.

Source: ProRealTime

Source: ProRealTime

Nasdaq technical analysis

The Nasdaq has enjoyed a rare bout of upside as markets approach risk assets with a more positive mindset. However, the wider trend does remain intact, with further weakness expected to come into play. This rise has taken price into the 61.8% Fibonacci level at 11617. As such, with a wider bearish trend in play, further downside is expected unless price breaks through the 12069 swing-high. Should that come into play, we would be looking at a more protracted upside move for the index.

Source: ProRealTime

Source: ProRealTime

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now