Bank of Japan (BoJ): Near-term pushback in policy tweaks for now

Entry posted by MongiIG in Market News

1,223 views

In the recent BoJ meeting, the central bank has refrained from making further adjustments to its yield curve control policy, which brought about some unwinding of previous ‘hawkish’ bets.

Source: Bloomberg

Source: Bloomberg

Bank of Japan (BoJ) defending a no-change to its yield curve control (YCC) program for now

Speculations of further tweaks to the BoJ’s YCC program have failed to find the much-needed confirmation in today’s meeting, as the BoJ refrained from delivering further changes to its policies, at least for now. At the meeting, the short-term policy interest rate was kept unchanged at -0.1% and 10-year bond yields at around 0%. The key market focus is on the possibility for further widening of the YCC range (from current 0.5%) or even abolishing it. That did not play out this time round, which pushed back against previous ‘hawkish’ bets. Just last week, traders were still challenging the benchmark 10-year bond yield cap, which saw the BoJ having to step in with a record amount of bond-buying operations. With the BoJ displaying its resolve to continue its large-scale bond-buying, along with the recent policy no-change, it is likely to clear the air against any speculation until the next meeting on 9-10 March 2023.

However, all is not over. What’s next?

The aftermath of the meeting has brought about a ‘less hawkish’ repricing in market expectations, with the timeline for a potential rate hike from the BoJ being pushed back to the June meeting now, as compared to the April meeting being priced previously. The current no-change may suggest some wait-and-see for now, especially when the central bank’s credibility was previously brought into question with its surprise move just a month back. However, it may be a matter of time before the BoJ step away from its accommodative policies eventually. The current pushback may delay the timeline for a policy shift at best. That could still leave the potential for lower yield differentials as a catalyst for JPY’s strength, at a time where other developed central banks are heading nearer to a rate pause while the BoJ is taking on the opposite direction.

Source: Refinitiv

Source: Refinitiv

BoJ still standing by its ‘transitory’ inflation stance

From the BoJ’s latest economic projections, there are greater downside risks to growth, with the real gross domestic product (GDP) figures for fiscal 2023 and 2024 revised lower from previous forecasts. While core consumer price index (CPI) were revised slightly higher to 1.8% from the previous 1.6% in FY2023, the still-low projection suggests that there is still a large degree of pricing pressures being seen as ‘transitory’. That seems to bring about more flexibility for the BoJ to stand pat on its accommodative policies. Japan’s inflation rate figures for December will be released this Friday. Current market expectations suggest that core inflation rate will further pull ahead to 4% from the previous 3.7%. Thus far, a peak in pricing pressures is yet to be seen, and further pull-ahead in inflation above the BoJ’s target of 2% could still lead to doubts around a lower-for-longer policy outlook for the BoJ.

USD/JPY: Finding its way higher but descending channel pattern in focus

The policy no-change from the BoJ has prompted some unwinding of previous ‘hawkish’ bets in the JPY, which brought about a 2.6% upmove in the USD/JPY in today’s session. That said, the USD/JPY has been guided by a descending channel pattern since mid-November last year, with recent upside bringing the pair just 0.3% shy from the upper channel trendline resistance. Failure to overcome the trendline resistance could still leave its ongoing downward bias intact, after the pair trades below its key 200-day moving average (MA) for the first time since February 2021.

Source: IG charts

Source: IG charts

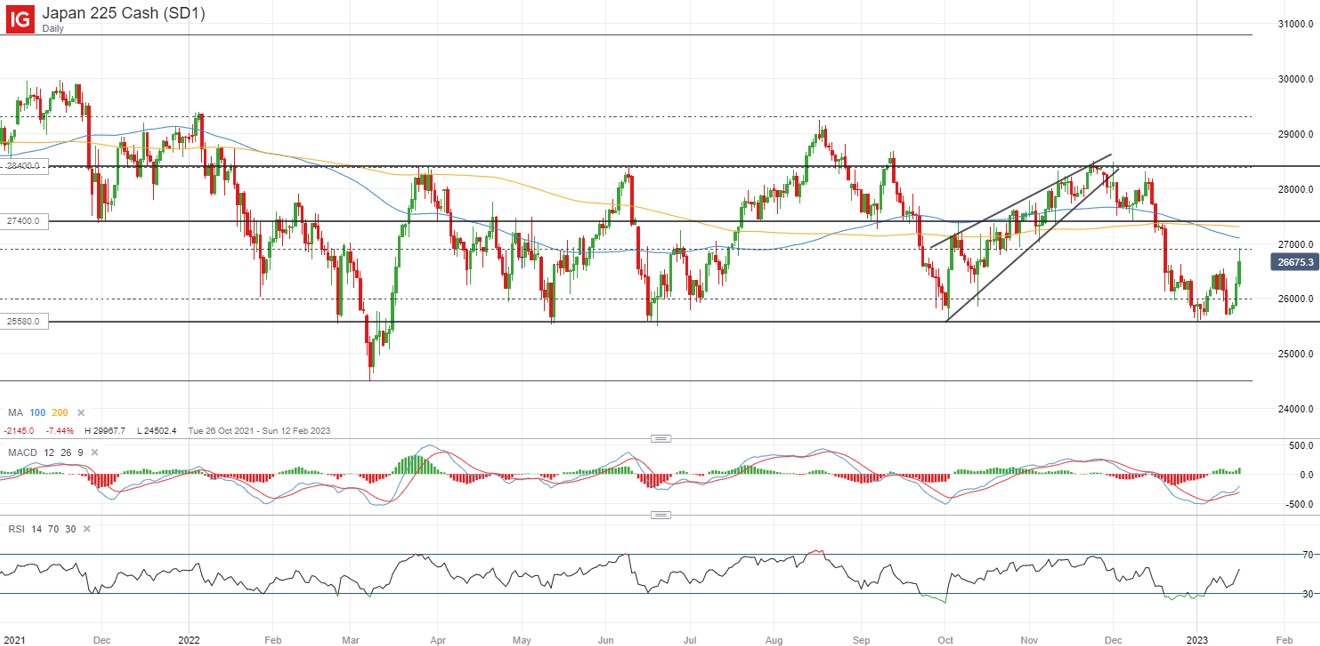

Nikkei 225: Near-term relief for equities but much awaits

After retracing more than 6% in the aftermath of BoJ’s December surprise, the Nikkei 225 has managed to pare some losses in today’s session on the policy status-quo. Market participants are finding some relief that further changes (increases) to the yield cap on the 10-year Japanese Government Bonds (JGBs) are off the table at least for now, until the next BoJ meeting on 9-10 March 2023. This provides some renewed traction for equities, which have been coming under pressure over the past month on the higher 10-year risk-free rate. The 2% surge in the index in today’s session is driving a retest of the 26,900 level, where a key 38.2% Fibonacci retracement stands. Further move above the 26,900 level could leave the 27,400 level on watch next.

Source: IG charts

Source: IG charts

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now