Microsoft’s Q2 earnings preview: Further moderation in earnings expected

Entry posted by MongiIG in Market News

492 views

Current market expectations are for Microsoft’s upcoming Q2 revenue to deliver its slowest year-on-year growth since June 2017.

Source: Bloomberg

Source: Bloomberg

When does Microsoft Corp report earnings?

Microsoft Corp is set to release its quarter two (Q2) financial results on 24 January 2023, after market closes.

Microsoft’s earnings – what to expect

Current market expectations are for Microsoft’s upcoming Q2 revenue to come in at $53.0 billion, up 2.4% year-on-year (YoY). If it holds true, this will be the slowest YoY top-line growth since June 2017. Earnings per share are expected to come in at $2.31, which is a 6.7% contraction from the previous year. This will be the weakest earnings growth since 2016.

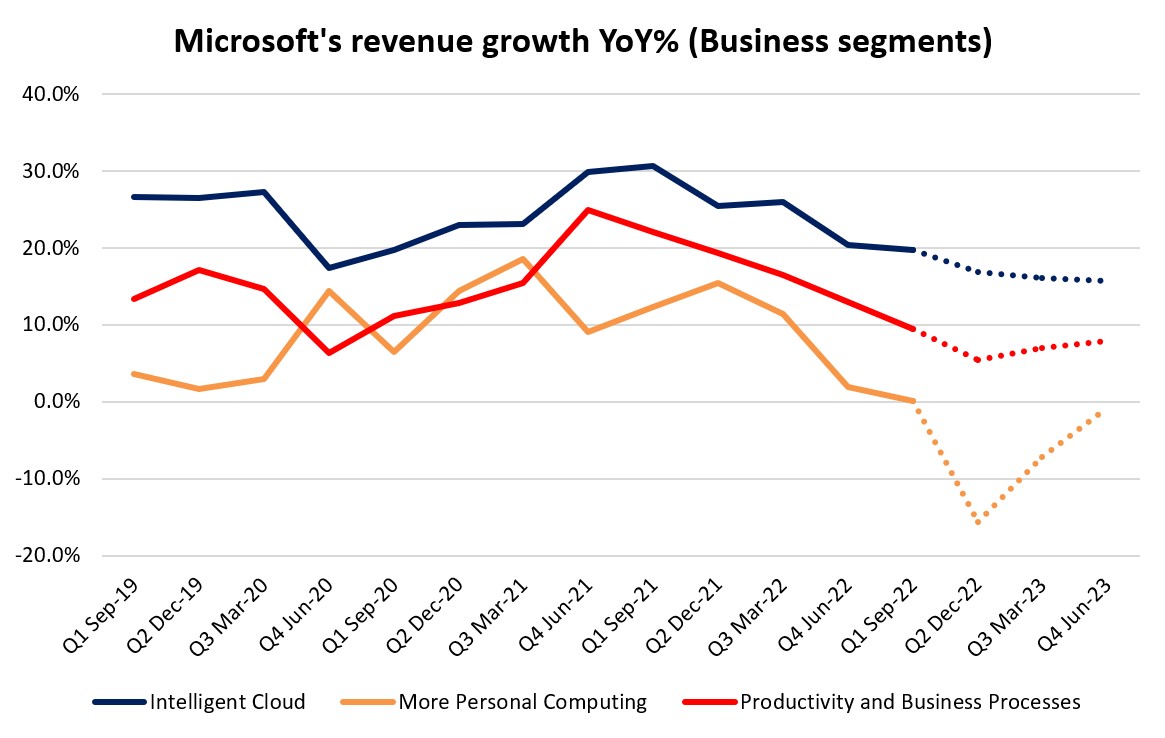

Weakness in PC market to remain a drag on earnings at upcoming results

As the pandemic boom seems to be largely behind us now, preliminary results from the International Data Corporation suggest that despite the fourth quarter of 2022 being a popular holiday season for spending, global shipments for traditional PCs were still down 28.1% from the prior year. This sharp moderation in the PC market may continue to provide a negative backdrop for Microsoft’s upcoming results, with a direct impact on its Windows operating system businesses and productivity software. Refinitiv estimates suggest that revenue for its ‘More Personal Computing’ segment may plunge into a 15.6% contraction from a year ago, following a flat 0.1% growth in the previous quarter. Likewise, its ‘Productivity and Business Processes’ segment is also expected to moderate further to 5.4% growth from previous 9.5%. Both segments account for a combined 60% of Microsoft’s overall revenue.

Perhaps the pocket of optimism is that the beaten-down expectations provides a lower watermark for outperformance to support some near-term relief, although past instances suggest that post-results gains over the past year were not sustaining over the longer term. A bottoming out in terms of corporate earnings will remain a key theme to watch. For now, estimates suggest that the upcoming Q2 2022 results could be the worst for Microsoft, but much will be dependent on the company’s forward guidance to provide the much-needed conviction.

Source: Refinitiv

Source: Refinitiv

Can cloud spending hold up amid cutback in corporate budget?

Much focus will be placed on Microsoft’s crown jewel (Intelligent Cloud segment) to do the heavy-lifting for earnings once more, considering that the segment takes up a whopping 41% of overall revenue and is also its fastest-growing business. With still-elevated costs and uncertain economic demand, companies worldwide have largely cut back on their growth plans to defend their margins, which saw the annual growth rate for worldwide cloud infrastructure services expenditure falling below 30% for the first time. That has a direct impact on Microsoft’s Azure as well, where revenue growth has moderated over the past two quarters (from 26.0% to 19.8% YoY). Further slowdown to 16.9% YoY is expected to be reflected in the upcoming results, as one may recall that the previous quarter had presented another 125 basis-point (bp) of tightening from the Federal Reserve (Fed).

The bright side is that the segment is still expected to be able to deliver a double-digit YoY growth (15-18%) over the next few quarters amid the downbeat environment. Growth could slow but the longer-term upward trend remains intact, as companies may still prioritise digital transformation in their reduced budget to prepare for subsequent recovery. A 9% retracement in the US dollar during the period measured could also improve overseas earnings when converted to local currency terms, with Microsoft deriving almost half (48%) of its overall revenue out of the US.

Source: Refinitiv

Source: Refinitiv

Layoffs in Microsoft support downbeat growth picture in the near term

Joining the ranks of Amazon, Twitter, Meta Platforms and Salesforce in the tech sector, further cost-cutting measures in the form of workforce reduction were also announced by Microsoft recently. While the layoffs may affect less than 5% of Microsoft’s overall workforce, the key takeaway here is that these big tech companies, which are deemed to be the more resilient and stable front in the US economy, are also caving in to economic pressure. Finding evidence to support the worst-is-over stance in earnings will be key to watch through 2023, but for now, it seems unlikely to show up in the current quarter just yet.

Technical analysis – 200-day moving average limiting reversal to the upside

After falling below its 200-day moving average (MA) back in February last year, the bears have since taken control, with two previous attempts to break above the resistance line failing to find the much-needed success for a trend reversal. The lower highs and lower lows presented over the past year continues to point to an overall downward bias for now, with share price recently finding resistance at the $214.30 level. This level marks a key 50% Fibonacci retracement from its Covid-19 bottom to its November 2021 top. Further downside will leave the $212.75 level on watch. Perhaps one may watch for any formation of a bullish divergence in moving average convergence/divergence (MACD) to support a build-up in short-term longs. Over the past one year, a bullish MACD divergence has preceded bear market rallies for Microsoft’s share price on three occasions.

Source: IG charts

Source: IG charts

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now