Ahead of the game

Entry posted by MongiIG in Market News

756 views

Your weekly financial calendar for market insights and key economic indicators for April 24, 2023.

Source: Bloomberg

Source: Bloomberg

Reading time: 4 minutes

FOLLOWING THE BANKING crisis last month, there was an expectation that central bank rate hikes would soon give way to rate cuts or, at worse, a pause. However, central bank communique this week and mixed data suggest central banks have unfinished business in their battle to tame inflation.

- RBA minutes confirmed a close decision to pause rate hike cycle, with Australian interest rate pricing in 25% chance of 25bp rate hike in May

- UK inflation remains high, with BoE expected to raise rates by 25bp to 4.50%

- US inflation expectations rose to 4.6% in April

- Fed officials have mixed views on interest rates, with Bullard favoring 5.5-5.75% range, while Bostic prefers one more rate rise then hold

- Q1 2023 earnings reports have started, with Netflix and Tesla seeing share price drops after reporting

- VIX index fell to 16.5, its lowest since Jan 2022

- RBA Review released key recommendations, including continuation of 2-3% inflation target and creation of separate Monetary Policy and Governance Boards.

↵

-

Wednesday, April 26 at 11.30am AEST: AU CPI

-

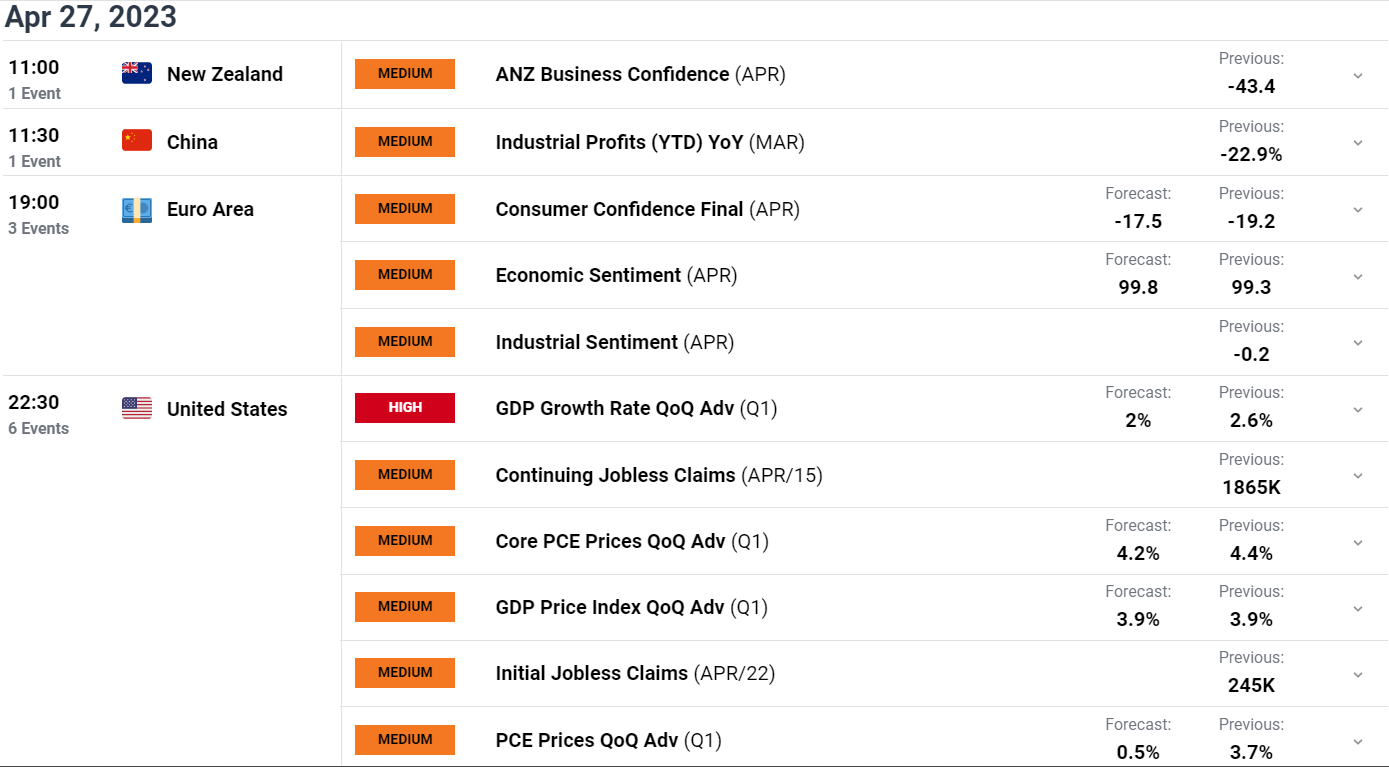

Thursday, April 27 at 11.30am AEST: ANZ Business Confidence

- Friday, April 28 (no set time): Bank of Japan Interest Rate Decision

-

Wednesday, April 26 at 12.00am AEST: Consumer Confidenc

-

Thursday, April 27 at 10.30pm AEST: Q1 GDP Advanced

-

Friday, April 28th at 10.30pm AEST: Core PCE Price Index

-

Friday, April 28th at 6:00pm AEST: EZ and DE - Q1 GDP flash

-

Friday, April 28th at 10:00pm AEST: DE - Inflation

Source: Bloomberg

Source: Bloomberg

-

Australia + NZ

Q1 2023 CPI report

Wednesday, April 26th at 11.30am AEST:

As revealed in the RBA meeting minutes for April, the Board discussed the various pros and cons of raising rates by a further 25bp on top of a substantial 350bp of rate rises or keeping rates on hold at 3.60%. “[O]n balance, [we] agreed that there was a stronger case to pause at this meeting and reassess the need for further tightening at future meetings.”

The minutes reiterated “that it was important to be clear that monetary policy may need to be tightened at subsequent meetings” and, in the final paragraph, noted the Board’s future cash rate decisions would depend on developments in the global economy, trends in household spending and the outlook for inflation and the labour market.”

The release of stronger-than-expected labour market data in mid-April confirmed that the labour market remains extremely tight. Should next week’s all-important CPI print fail to confirm that inflation is falling as quickly as anticipated, the RBA may act on its tightening bias and hike the cash rate again as soon as next month.

The key numbers:

- Headline CPI is expected to increase by 1.3% in Q1 2023 for an annual rate of 6.9%, falling from 7.8% in Q4 2022.

- Trimmed mean is expected to rise by 1.4% in Q1 2023 for an annual rate of 6.7%, falling from 6.9% in Q4 2022

Trimmed mean chart

Source: TradingEconomics

Source: TradingEconomics

-

Japan

BoJ interest rate decision

Friday, April 28th – no set time:

The new Bank of Japan Governor, Kazuo Ueda, began his five-year term earlier this month tasked with the responsibility of exiting the ultra-loose monetary policy of his predecessor Kuroda and delivering a “soft landing”.

While no adjustment to YCC policy is expected this month, a surprise move cannot be ruled out, which would send both the Nikkei and USD/JPY sharply lower.

Bank of Japan

Source: Bloomberg

Source: Bloomberg

-

US

Q1 2023 earnings reports

Earnings reports are set to flow in the coming week from Megatech companies, including Alphabet, Meta, Microsoft and Amazon, as well as Coca-Cola, PepsiCo, McDonald’s, Boeing, Exxon and Chevron.

Core PCE Price Index

Friday, April 28th at 10.30pm:

The Feds preferred measure of inflation, the Core PCE Price Index, is expected to fall to 4.6% in March from 4.7% in February. This would be the lowest reading in sixteen months.

A higher-than-expected number would all but seal the deal for a 25bp rate hike at the upcoming May FOMC meeting and raise concerns that higher rates are needed to tame inflation.

Core PCE Price Index chart

Source: TradingEconomics

Source: TradingEconomics

Economics calendar

All times shown in AEST (UTC+10) unless otherwise stated.

Source: DailyFX

Source: DailyFX

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now