EasyJet earnings previews: is now the right time to buy?

Entry posted by MongiIG in Market News

1,285 views

Fundamental and technical outlook on the easyJet share price ahead of Tuesday’s full-year earnings.

Source: Bloomberg

Source: Bloomberg

What to expect from easyJet’s full-year earnings

The recent financial performance of easyJet has been a mixed bag. While the airline reported a "record summer" and forecasted a strong pre-tax profit for fourth quarter (Q4), the full-year profit outlook fell short of expectations. Factors such as strike actions and increased competition have contributed to this disparity. Additionally, rising global fuel prices, triggered by the Hamas attack in October, have negatively impacted passenger numbers.

However, there are signs of improvement in the industry. Ryanair, one of easyJet's major competitors, has forecasted a record annual profit, citing a significant increase in airfares during the warmer months. This positive outlook for Ryanair reflects an overall recovery in the air travel sector.

On Tuesday, easyJet will confirm its annual profit before tax within the previously provided range. This announcement will be crucial for shareholders, as the airline's board has committed to distributing 10% of profits after tax to them. However, analysts and investors will likely be more interested in easyJet's forecasts for 2024, considering the impact of rising fuel prices and the war in Palestine on the airline's performance and demand for winter sun destinations.

EasyJet's hedging strategy will also play a vital role in navigating the challenges posed by rising fuel prices. The company has already secured hedging for a significant portion of its fuel needs for the first and second halves of fiscal year 2024.

The recovery of easyJet is a complex endeavour, given the fierce competition in the short-haul market and the difficulty of passing on rising costs to passengers. However, the airline's management has been proactive in maintaining a competitive edge. Strategic moves, such as upgrading the fleet through a substantial Airbus order and expanding the easyJet holidays operation, demonstrate their commitment to success.

It is worth noting, though, that easyJet has posted three consecutive years of losses, although these losses have been narrowing from £1.03bn in 2021 to £208m in 2022. The company's anticipated pre-tax profits of between £440m and £460m for the current year mark another step in the right direction. From a valuation perspective, easyJet's shares appear to be good value, with relatively low forward price-to-earnings (P/E) ratios of 8.6 times earnings and 7.2 times for 2024 as well as an expected yield of over 3% for 2024. After all, easyJet was posting steadily rising profits before the pandemic struck.

Looking at easyJet's competitors, both Ryanair and Wizz Air have reported an increase in passenger numbers, indicating a rebound in air traffic. Ryanair, in particular, has shown resilience in its financial performance and passenger volumes. Its robust traffic growth and improved load factor have contributed to a significant increase in profit after tax.

easyJet analyst ratings

Data from Reuters Refinitiv shows that of the 20 analysts who currently cover easyJet, two have a ‘strong buy’, nine a ‘buy’, seven a ‘hold’, one a ‘sell’ and one a ‘strong sell’ rating. The average analyst recommendation thus sits between a ‘buy’ and a ‘hold’ with a mean target price at 639.74 pence, approximately 56% higher than the current price (as of 27 November 2023).

Source: Refinitiv

Source: Refinitiv

easyJet technical analysis

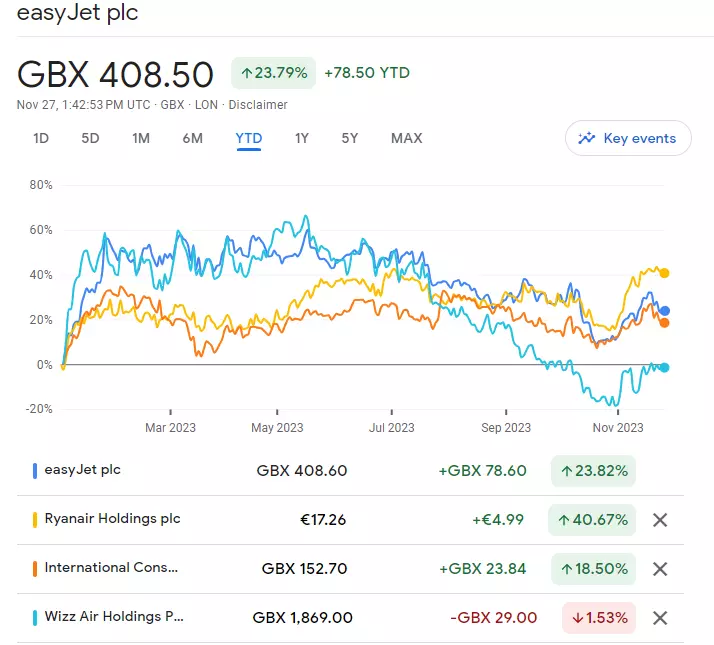

The easyJet share price, which has risen by around 24% year-to-date, not only greatly outperforms the FTSE 100 but also British Airways’ owner International Consolidated Airlines Group (IAG) and budget airline Wizzair but lags its direct competitor Ryanair with its 40% year-to-date gains.

Source: Google Analytics

Source: Google Analytics

When looking at a monthly candlestick chart the easyJet share price is trading around its 2020 pandemic lows but so far remains above its October 2022 decade low at 276.9 pence.

For a long-term bullish reversal to occur, a rise and ideally a monthly close above the current November peak at 445.6p would need to occur. In this case the 2020-to-2023 downtrend line would be broken through as well with the May peak at 534.8p being back in sight.

easyJet Monthly Candlestick Chart

Source: TradingView

Source: TradingView

For the shorter-term October-to-November uptrend to remain valid, the easyJet share price needs to hold above its mid-November low at 390.5p on a daily chart closing basis. Failure there could lead to the October trough at 350.0p being revisited.

EasyJet Daily Candlestick Chart

Source: TradingView

Source: TradingView

Immediate resistance between the October and current November highs at 445.6p to 450.7p will need to be overcome, and ideally the August-to-September peaks at 462p to 464.4p for a bullish reversal to become longer-term plausible.

This information has been prepared by IG, a trading name of IG Markets Limited. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients. See full non-independent research disclaimer and quarterly summary.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now