Key events to watch in the week ahead: 19 - 25 February 2024

Entry posted by MongiIG in Market News

1,138 views

What are some of the key events to watch next week?

Source: Bloomberg

Source: Bloomberg

This week’s overview

Despite some inflation jitters brought by a hotter-than-expected US consumer price index (CPI) print this week, Wall Street managed to regain its footing with the S&P 500 setting yet another record high. It seems like the risk rally has been left unscathed, as market participants recalibrated their rate expectations to be more in line with the Federal Reserve (Fed).

Japan’s Nikkei stole the limelight in Asia, briefly topping the 38,800 mark for the first time since January 1990 and leaving it just than 2% away from a new record high. The ASX 200 is flirting with previous record-high territory as well, while closer to home, the Straits Times Index (STI) has also seen renewed signs of life, rebounding by close to 4% since Wednesday to reclaim its 200-day moving average (MA).

As we head into the new week, here are six things on our radar.

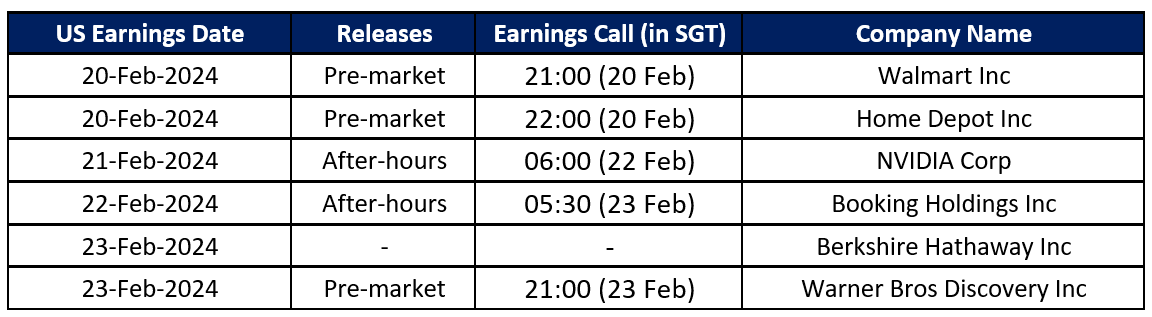

US earnings season: Walmart, Home Depot, NVIDIA, Berkshire Hathaway

The US earnings releases next week will leave spotlight on Nvidia’s results as the key risk event for markets. With Nvidia accounting for the bulk of the market rally through 2023 and into 2024, high expectations are in place, which leaves little room for error.

Thus far, corporate earnings momentum has been robust. As of 16 February 2024, 79% of S&P 500 companies have released their results, with 80% delivering an earnings beat. This rate of outperformance towers above both the 5-year average (77%) and 10-year average (74%).

Source: Refinitiv

Source: Refinitiv

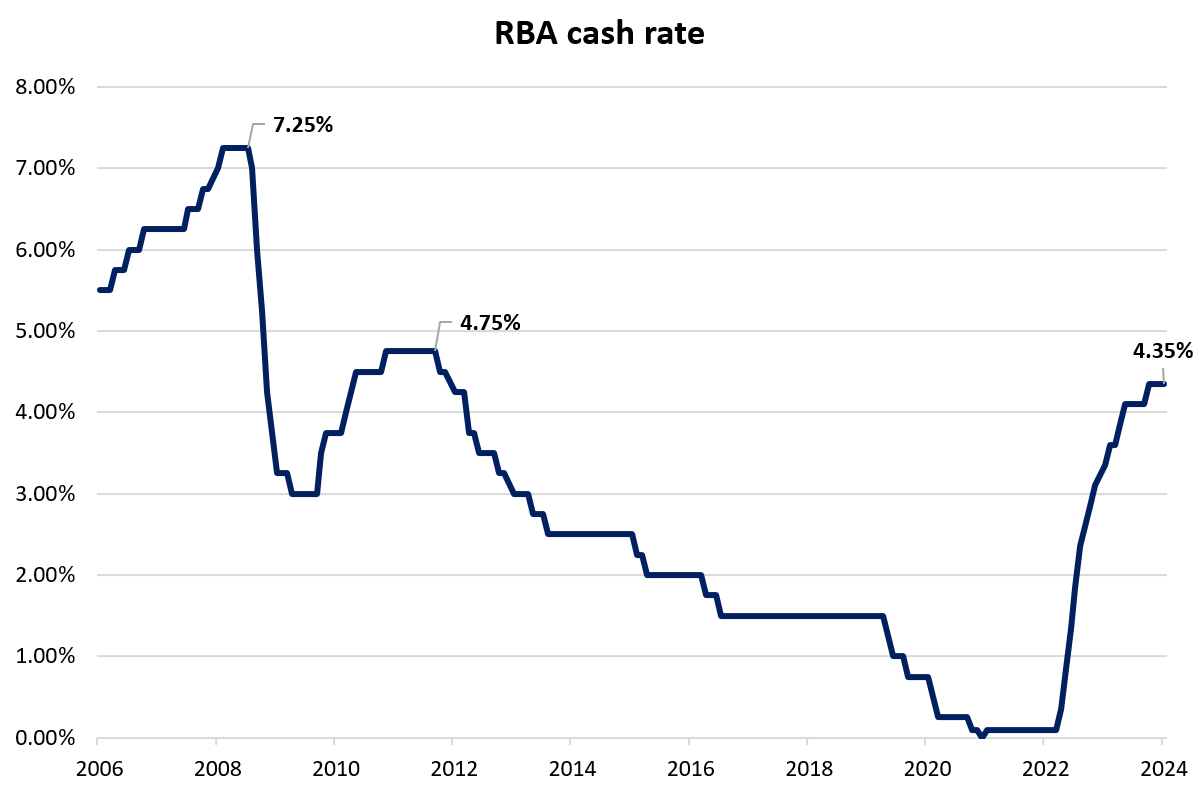

20 February 2024 (Tuesday, 8.30am SGT): Reserve Bank of Australia (RBA) meeting minutes

In its February meeting, the RBA maintained the official cash rate at 4.35% in line with expectations. The Bank observed that elevated interest rates are effectively moderating inflation and fostering a balanced supply-demand equilibrium.

"Higher interest rates are working to establish a more sustainable balance between aggregate demand and supply in the economy."

The RBA highlighted its data-driven approach, maintaining a slight tightening bias.

"The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks, and a further increase in interest rates cannot be ruled out."

Analysts will meticulously analyse the minutes for insights into the RBA Board's deliberations in February, indicators for future policy adjustments based on its tightening stance for 2024, and any indications towards a shift to a more neutral policy outlook.

Source: Refinitiv

Source: Refinitiv

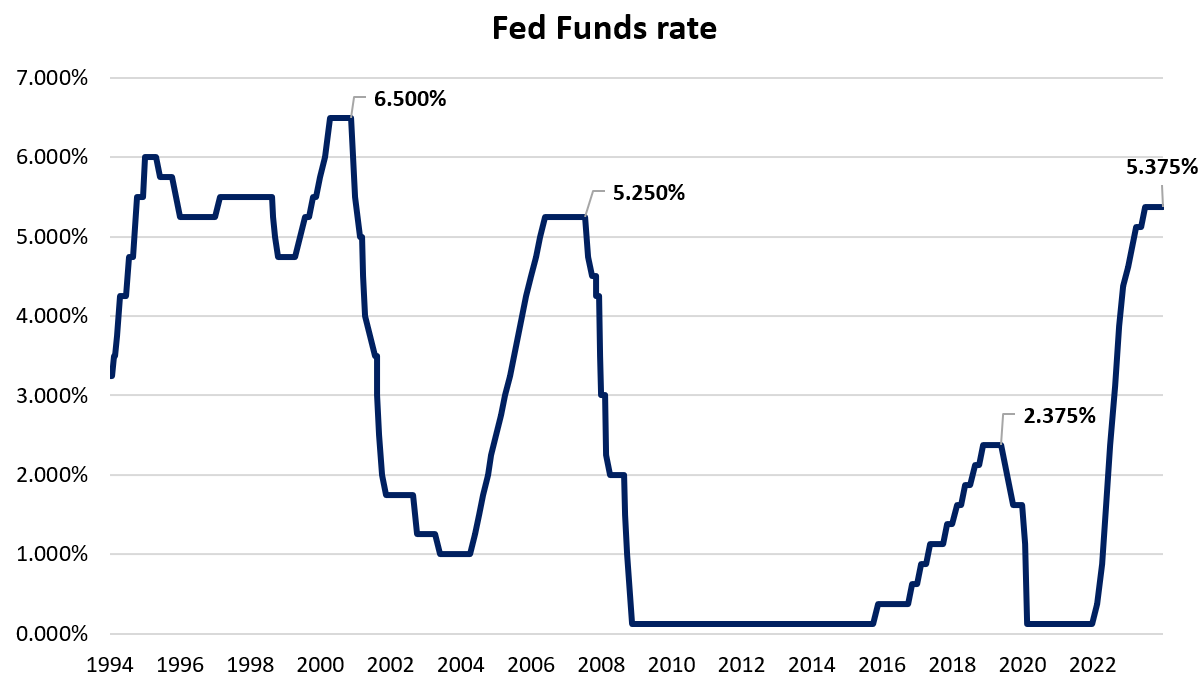

22 February 2024 (Thursday, 3am SGT): Federal Open Market Committee (FOMC) meeting minutes

In its January session, the Fed kept the Fed Funds target rate steady at 5.25%-5.50% for the fourth consecutive meeting. The Fed updated its policy stance, indicating rate cuts are on the horizon, though not immediate.

"The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent."

Analysts will thoroughly examine the minutes for insights into the Fed's balance sheet strategies, potential timing for rate reductions, its perspective on recent US economic data exceeding expectations, and perceived risks to the global economy.

Source: Refinitiv

Source: Refinitiv

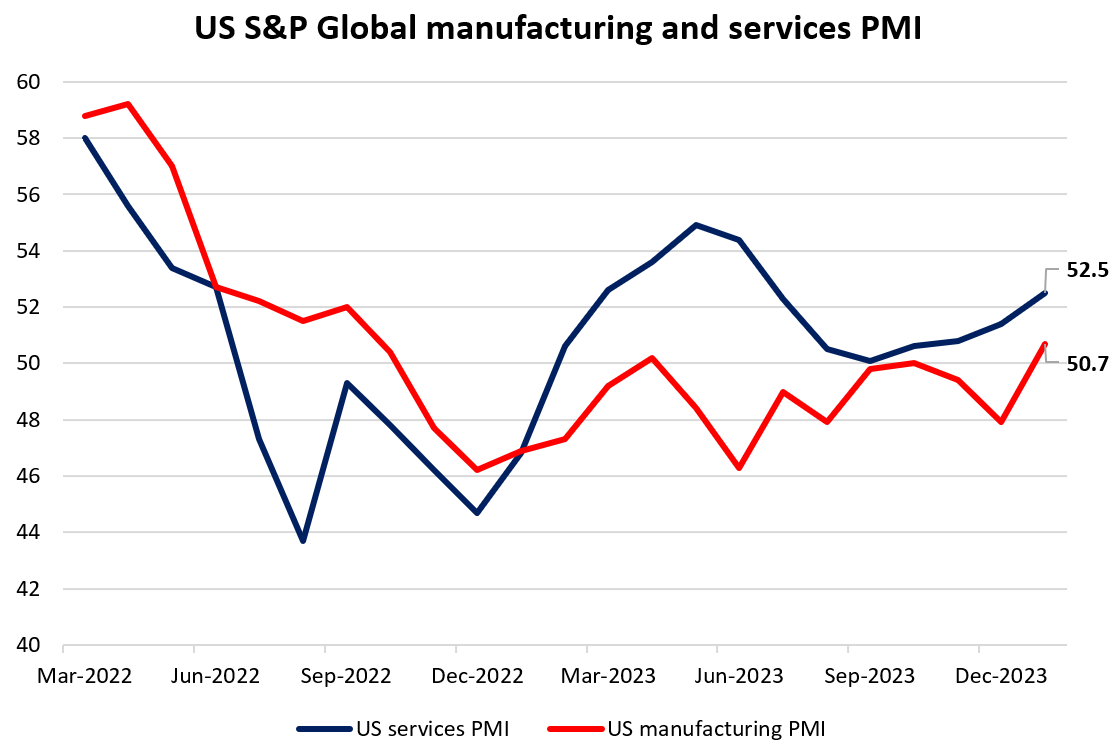

22 February 2024 (Thursday, 10.45pm SGT): S&P Global flash US Purchasing Managers' Index (PMI)

Last month, the US PMI numbers from S&P Global have revealed a stronger upturn in economic activities, with the manufacturing sector delivering its highest read since September 2022 at 50.7. Growth in services has been robust as well, delivering its fourth straight month of increase to 52.5. Overall, this brought the US composite PMI to a six-month high at 52.0.

The takeaway from the sub-components over the past months is one of lukewarm economic growth and waning cost pressures, which may be encouraging for soft landing hopes and impending rate cuts, currently priced to be leaning towards the June meeting. The upcoming read for February is expected to reinforce more of the same, with the manufacturing sector expected to ease to 50.1 from previous 50.7, while the services sector PMI may ease to 52.0 from previous 52.5.

Source: Refinitiv

Source: Refinitiv

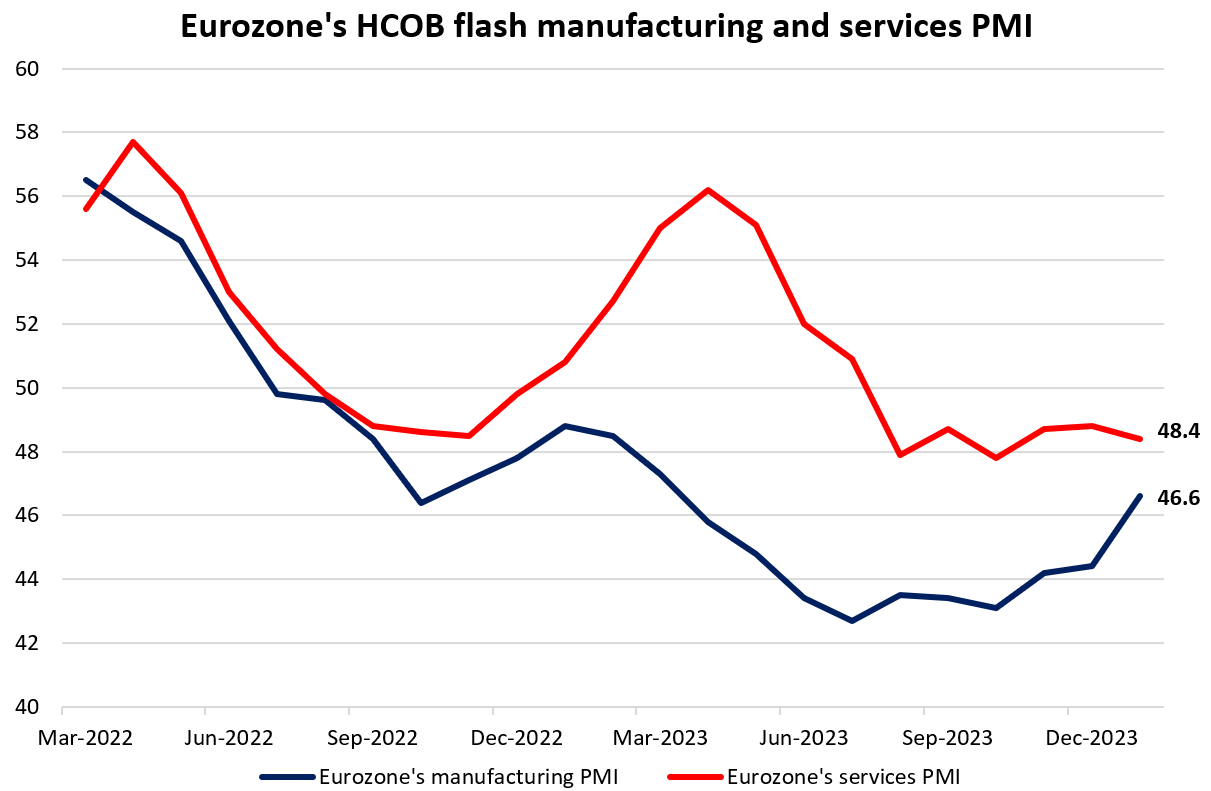

22 February 2024 (Thursday, 5pm SGT): Hamburg Commercial Bank (HCOB) Eurozone PMI

While economic conditions in the Eurozone have been in contraction territory for the eighth straight month, there are slight signs of improvement lately. From its January PMI figures, the manufacturing sector has turned in a softer contraction at 46.6, while the services side continue to stabilise around the 47-48 range, following a sharp moderation since April 2022.

The improvement is set to continue into January, with expectations for manufacturing PMI to improve to 47.0 from previous 46.6. Services PMI is expected to turn in a lesser contraction as well at 48.7 versus 48.4. The still-subdued economic conditions may likely help in the current disinflation process, potentially raising optimism about getting inflation back to the European Central Bank (ECB)’s 2% target and support upcoming cuts, potentially in June.

Source: Refinitiv

Source: Refinitiv

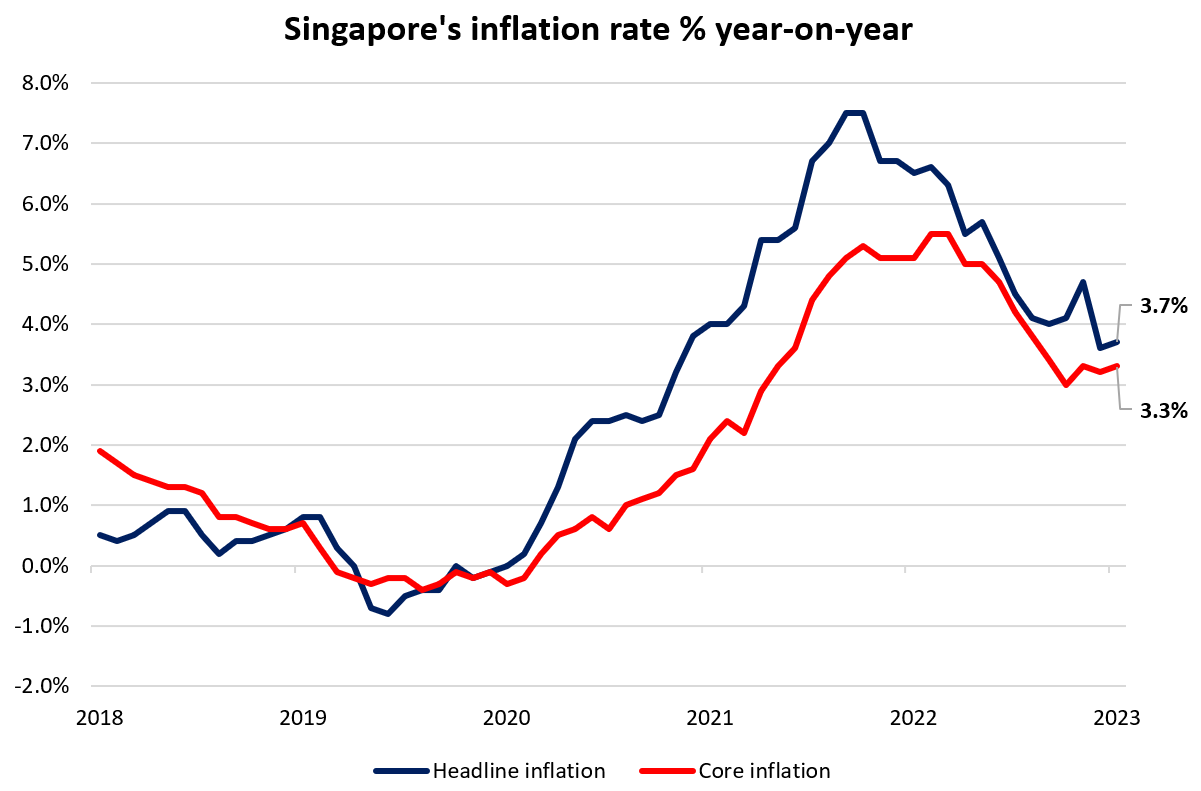

23 February 2024 (Friday, 1pm SGT): Singapore’s inflation rate

Singapore’s headline and core inflation rate has seen a surprise uptick in December 2023, attributed to a faster pace of increase in private transport costs and services inflation. While the persistence in pricing pressures is likely to continue into early 2024 to reflect the latest Goods and Services Tax (GST) rate increase, the Monetary Authority of Singapore (MAS) and Ministry of Trade & Industry (MTI) still expect a “gradual moderating trend” in core inflation over 2024.

With that, authorities may look beyond any near-term uptick in inflation as long as it continues to fall within its projected range for 2024 (3%-4% for headline, 2.5%-3% for core). For the upcoming read, consensus is for Singapore’s headline inflation to tick higher to 3.9% from previous 3.7%.

Source: Refinitiv

Source: Refinitiv

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now