Q2 US reporting season: strong EPS growth expected to show a profit cycle in full swing

Entry posted by ArvinIG in Analyst article

440 views

A strong period for US corporate earnings is expected as companies reflect the continued recovery in the US economy, with further growth expected in coming quarters.

Source: Bloomberg

When is US reporting season?

US reporting season will kick off the week beginning 12 July and will extend to the middle of August.

The market data that matters:

| EPS Growth Expected (YoY) | Revenue Growth Expected (YoY) | Current Price-to- Earnings | Est. FY1 Price-to earnings | Current Dividend Yield |

| 59.80% | 19.50% | 30.64 | 22.75 | 1.34% |

Source: Bloomberg Intelligence

What is the market expecting out of this earnings season?

Sell side analysts are tipping a bumper earnings period for S&P 500 companies. As the economic recovery hits full stride, Bloomberg Intelligence currently estimates that earning per share (EPS) ought to grow by 59.8% this quarter on a year-over-year (YoY) basis.

If realized, the increase will be the biggest jump in profit growth for a quarter since the end of 2010, as company earnings surge back from the depths of the Covid-19 recession one year ago. The sectoral outperformers in quarter two (Q2) are expected to reflect this cyclical rebound in US economic growth.

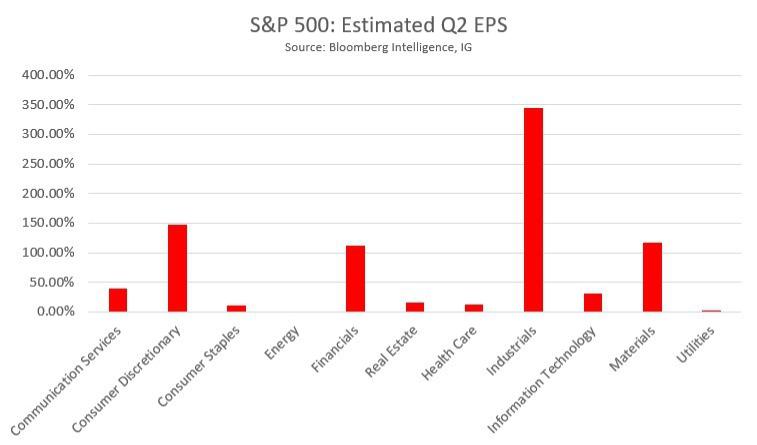

Industrials are tipped to deliver 344.2% EPS growth, consumer discretionary expected to deliver 147.9% EPS growth, while materials stocks are forecast to deliver 117.6% EPS growth for the quarter.

Source: Bloomberg Intelligence, IG

The key questions this reporting period

How much longer can the good times last?

Analysts are estimating an extraordinary period of profit growth across the S&P500, as the base effects of last year’s earnings recession combined with a roaring US economy in the last quarter propel EPS growth to decade long highs. Given the likely strong results and lofty expectations, a central concern this earnings season will be how much longer companies expect the strong growth to last, as the economic cycle begins to mature.

As it stands, the greatest rate of growth in profits for the cycle is expected to be realized in Q2, however analysts have still been upgrading the outlook for future profits, with the top of the profit cycle still seemingly to come.

Has the market already priced-in the strong profit growth?

In recent quarters, market prices have proven less receptive to earnings growth and earnings beats across the S&P500. High prices and rich valuations have meant that a lot of good news has already been baked into the mark before the commencement of earning season, as investors chase yield in risky assets, in a market environment flooded by central bank liquidity.

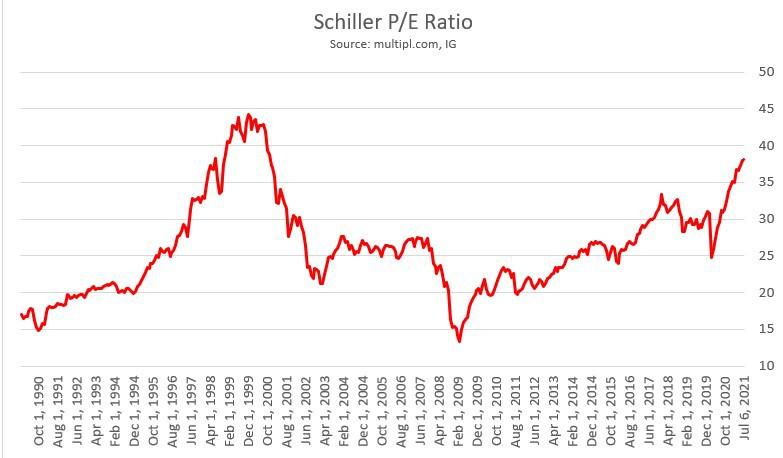

The situation will be no different in Q2, with the bar set very high for companies to surprise to the upside, with market multiples, such as the Schiller price earnings (P/E) Ratio, suggesting that current valuations across the S&P500 are as stretched as at any point since the Dot.com crash.

Source: multipl.com, IG

How big of a risk is inflation to the fundamental outlook?

Although implied expectations of future inflation in financial markets have recently diminished, there will remain a high degree of interest this earnings season in what corporates say about inflation pressures going forward. In particular, market participants will be keeping a close watch on what company management says about ongoing supply disruptions, along with persistent labour market shortages.

There are some fears that these greater cost pressures could lead to some combination of higher inflation, or lower profitability for companies. At least in the last quarter, such pressures are tipped to have remained relatively contained, with Bloomberg Intelligence tipping robust 12.4 per cent margins for S&P500 companies in Q2.

How could this earnings season impact the S&P500?

As it always does, the performance of the S&P 500 this earnings season will come down to whether company profits exceed estimates, and by how much. With valuations rich, questions about future growth rife, and some level of fear about future Federal Reserve (Fed) policy, there’s some risk that prices are fully discounting the explosive profits set to be posted this quarter.

Nevertheless, with the earnings upgrade cycle in full swing, and in any absolute sense, monetary policy remaining accommodative, the trend clearly remains skewed to the upside for the S&P500. Given the relatively rich premium over the 20-daily moving average (DMA), and a relative strength index (RSI) holding tentatively above 70, perhaps short-term risk-to-reward is skewed to the downside. But in this market, it’s likely any pullback for the S&P500 is an opportunity to buy the dip.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now