Covid Worries Don’t Capsize Markets Just Yet, But Watch the Dow and US Dollar

Entry posted by MongiIG in Market News

1,297 views

S&P 500, NASDAQ 100, DOW, COVID AND DOLLAR TALKING POINTS

- The S&P 500 led ‘risk assets’ on a broad slump in sentiment this past Friday which found fundamental blame in news of the Omicron Covid variant

- Markets made a bid to recovery this past session, but the Dow and the DAX didn’t seem to muster the same enthusiasm as speculative favorites like the SPX and Nasdaq

- A full recovery in risk trends is almost assumed given seasonal conditions and post-Covid momentum, but the Dollar may offer a more insightful nuance

RECOVERING FROM A LOW LIQUIDITY, HIGH FUNDAMENTAL RISK PLUNGE

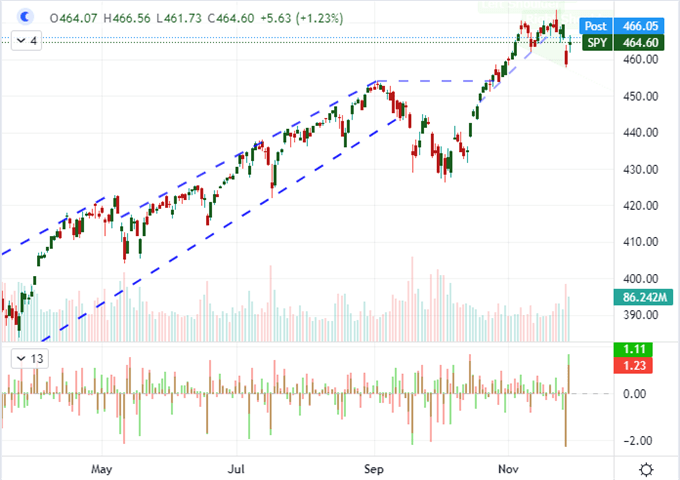

Risk-oriented assets took a dive late last week. Market conditions thinned by the holiday conditions in the US would play as critical a role as the well placed (or poorly placed depending on your viewpoint) reports that a new variant of the Coronavirus had put global experts and leaders on high alert. By the close of the week, the drained US equity market notched its biggest loss in at least nine months for the largest indices, but the damage certainly spread much further. Breadth of risk aversion is a far more convincing sign in my book of generalized fear rather than a particularly impressive performance from a singular assets. With the markets filling out to start this new trading week, traders were eagerly awaiting signs that the reliable dip-buying routine would kick back in. The S&P 500 followed its -2.3 percent plunge (the worst single-day loss since late February) with a 1.3 percent Monday rally based largely on the biggest opening gap (0.74 percent) since March 9th. That doesn’t fully recover Friday’s cumulative lost ground, but it speaks to greater confidence than most other measures of ‘risk’.

Chart of SPY S&P 500 ETF with Volume, 1-Day Range and Gaps (Daily)

Chart Created on Tradingview Platform

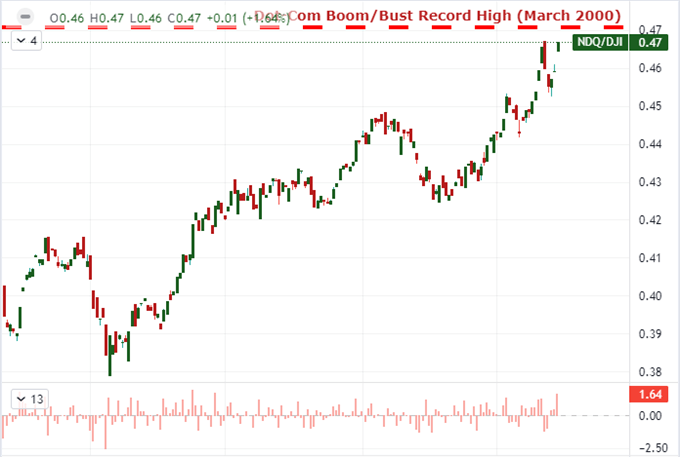

First and foremost, I draw concern with the recognition that the blue-chip Dow mustered far less a rebound than its more growth-oriented and ‘diamond hand’ favored counterparts. The 0.68 percent Monday rebound falls well short of a comprehensive recovery compared to the SPX or the Nasdaq 100’s 2.3 percent charge. That should raise concern. With his disparity in recovery, the Nasdaq 100 to Dow ratio has posted its single biggest rally in five months and pushed us to the precipice of the Dot-com boom/bust peak set back in March 2000. The disparity doesn’t stop there. Looking at international equities, we find the likes of the German DAX, the UK’s FTSE 100 and Japan’s Nikkei 225 are far less ambitious in their recovery – it comes as no surprise that they have been flagging in their following the SPX. Further out, other risk-leaning assets are performing even worse. Emerging market, junk bonds, carry trade and commodities with a risk-orientation are all struggling. That seriously undermines my confidence that this will be a steadfast climb into the close the year.

Chart of Nasdaq to Dow Ratio With 1-Day Rate of Change (Daily)

Chart Created on Tradingview Platform

THE FUNDAMENTAL RISKS AGAINST SEASONAL EXPECTATIONS

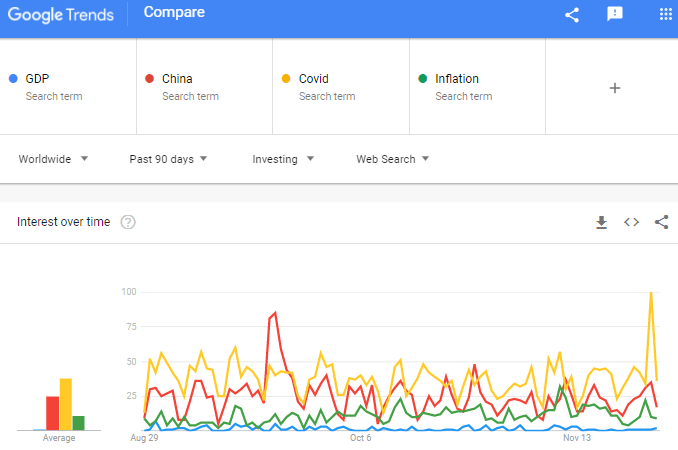

Important to weighing the amount of pressure being exerted on speculative intent is keeping close track of the dominant fundamental themes unfolding in the open markets. While fears around the Omicron variant of the Coronavirus have ebbed somewhat relative to Friday’s peak panic, the threat remains prominent. There is differing reports as to the virulency of the new variant, and we were already in the middle of a fourth worldwide wave of the pandemic in terms of new cases. The scope of market impact from this new feature of the ongoing economic suppression depends on the response from the world’s leaders. Dozens of countries have placed travel bans on southern African countries with Omicron outbreaks and heads like President Joe Biden issued warnings about the economic risk, but there haven’t been widespread economic shutdowns or trade curbs to further exacerbate the troubled supply chain. If/when that changes, the ‘buy the dip’ power will falter.

Chart of Search Interest in ‘GDP’, ‘China’, ‘Covid’ and ‘Inflation’ of Google Trends (Daily)

Chart from Google Trends

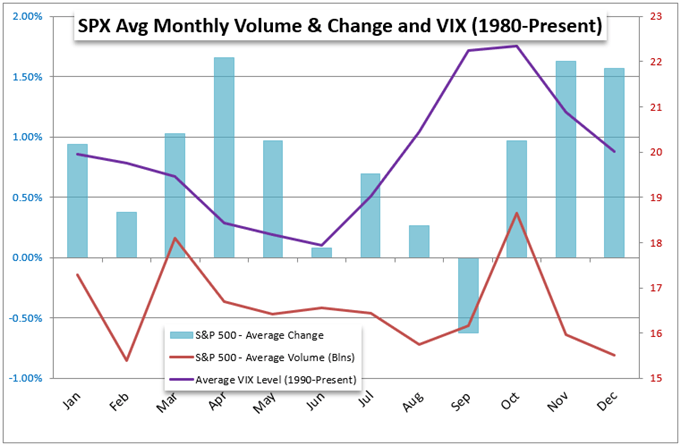

Of course, working against the unfolding fundamental threats are the seasonal assumptions that most investors carry with the year-end norms. Today is the last trading day for the month of November – with the S&P 500 close to closing out a modest gain for the period while most other benchmarks I track are not – and December historically has offered up much the same: robust gains in speculative favorites as volume and volatility deflate. Of course, the more familiar the disparity in performance across the various sentiment measures, greater the threat to a passive stability. And, as this past Friday proved, there are always exceptions to the rule…

Chart of S&P 500 Monthly Performance, Volume and Volatility

Chart Created on John Kicklighter with Data from S&P

MARKETS AND EVENT RISK TO WATCH

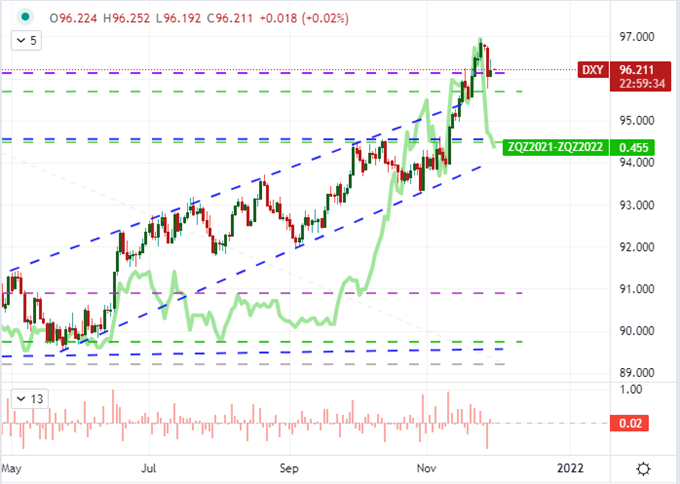

Moving into Tuesday’s trade and then into December, I will be watching the contrast in the various risk measures much more closely. If it is too difficult to monitor a dozen or more unrelated benchmarks, I think the Dow’s contrast to the S&P 500 and Nasdaq 100 provides a good first level sanity check on conviction. Another fundamental asset to speak to complications is the Dollar. Notably, the currency took a tumble this past Friday despite its usual position as a safe haven currency. It still earns the role of harbor, but it has also built up a lot of carry trade appeal in the past weeks that will bleed off before that ‘last resort’ status kicks back in. Nonetheless, interest rate forecasts will suffer should risk aversion and growth fears kick in, but seeing the Greenback’s relationship to this theme in general can speak to the scale of intensity in risk trends.

Chart of DXY Dollar Index with 1-Day Rate of Change Overlaid with Fed 2022 Implied Hikes (Daily)

Chart Created on Tradingview Platform

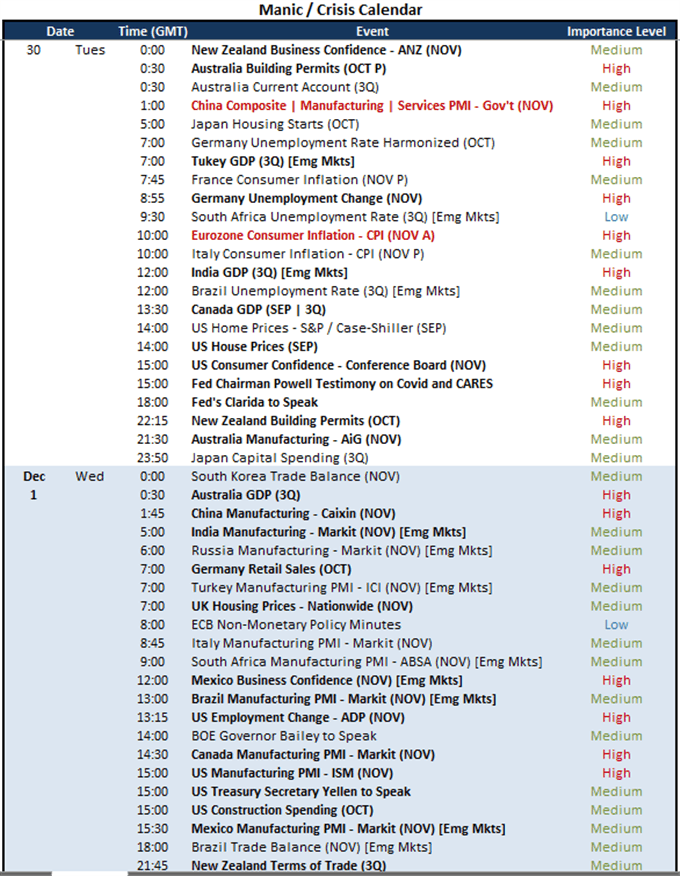

Outside of the abstraction of risk trends, Covid fears and monetary policy expectations, there is quite a bit of scheduled event risk on tap through the next 24 hours. While I will be watching Eurozone CPI, Fed speak and the US consumer sentiment survey (which has picked up on inflation pressure recently); there is also a distinct update on GDP due today. China’s government PMIs for November will start things off; but there is Turkey and India 3Q GDP figures to give key EM economy insight as well as Canada’s September and 3Q update to speak to the developed world. There is more GDP data later in the week, but this is enough to speak to a theme and not just discrete country and currency insight.

Calendar of Major Macro Event Risk Through Week End

Calendar Created by John Kicklighter

by John Kicklighter, Chief Strategist, 30th November 2021. DailyFX

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now