US non-farms preview: jobs growth to slow, but wage growth holding firm

Entry posted by MongiIG in Market News

667 views

While the headline number of jobs created in May is expected to be slightly weaker, a rise in wages over the month suggests the employment picture is still healthy.

Source: Bloomberg

Source: Bloomberg

What to expect from the US non-farm payrolls (NFP) report?

325,000 jobs are expected to have been created in the jobs report this week, a slowdown from the 428,000 in the May report.

However, the unemployment rate is forecast to fall to 3.5% from 3.6%, continuing the steady improvement from the pandemic period.

Meanwhile, in a potentially more important development, wages are expected to rise 0.4% over the month, from 0.3%, a sign that inflationary pressures are set to continue.

What does this mean for markets and Fed policy?

For the moment, the US economy continues to add jobs, a clearly positive sign. The slowdown from last month’s figures should not be unduly concerning, especially with the unemployment rate at such a low ebb. Seasonal variations affect job creation, and for the time being the US Federal Reserve's (Fed) confidence in the outlook remains well-founded.

Thus the Fed’s requirement to maintain full employment, part of its ‘dual mandate, is still being met. This leaves the focus on inflation, which is expected to keep rising in the months to come, albeit at perhaps a slower pace.

It is unlikely that this month’s NFP figure will cause any change to Fed policy. Even a stronger reading on jobs or wages will not really move the dial in terms of the pace of tightening, and, as is usually the case when the economy is so strong, it would take a big miss on the headline figures to really prompt even a short-term reassessment of their monetary policy outlook.

Markets should therefore remain relatively unmoved by this week’s number, assuming it does not surprise too dramatically in either direction. The dollar is still strong, and has begun to recover from some weakness over the last month. Meanwhile, stocks have rebounded from their lows, but nervousness persists as investors fret about a further weakening in earnings.

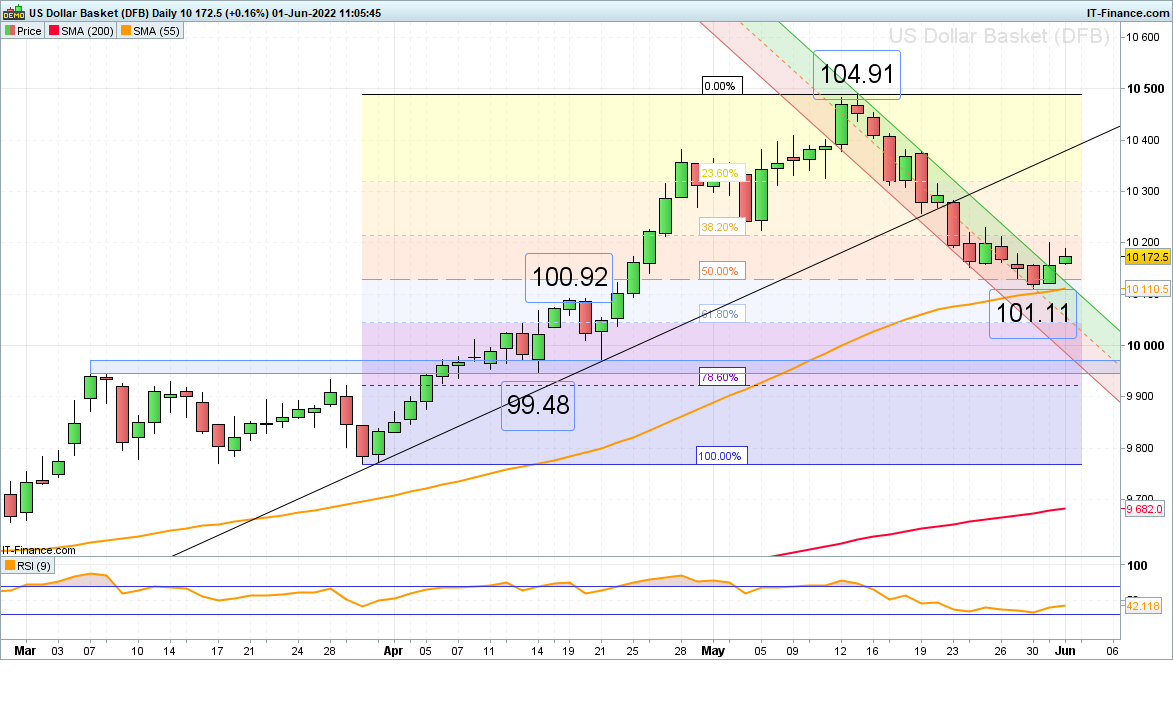

US dollar outlook

The US Dollar Index’s (DXY) swift two-week decline from its 104.91 mid-May high levelled out slightly above the 55-day simple moving average (SMA), now at 101.10, and the late April high at 100.92, around the 50% retracement of the April-to-May ascent, as US investors have entered the fray following Monday’s Memorial Day holiday.

The index has been declining these past couple of weeks as investors have become increasingly hopeful that the Fed might not raise rates as aggressively as previously thought.

The publication of the Eurozone’s record inflation at 8.1% for May on Tuesday, the highest reading in the euro’s existence, unnerved investors, though, and pushed the US Dollar Index higher, so far to 102.01.

Provided that the 101.01 to 100.92 region continues to offer support, the 5 May low and 25 May high at 102.25 to 102.29 will be in focus. Only a rise and daily chart close above this minor resistance area would indicate that the previous uptrend has resumed.

A slip through the 100.92 20 April high would engage the 99.70 to 99.46 region, consisting of the March high, mid- and 21 April lows, however.

Source: ProRealTime

Source: ProRealTime

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now