Quiet economic calendar and Fed blackout period sees S&P 500 in a holding pattern

Entry posted by MongiIG in Market News

591 views

Major US indices eked out slight gains overnight but the sharp paring back of early gains and the in-tandem rise of the VIX suggests that some caution remains.

Source: Bloomberg

Source: Bloomberg

Market Recap

Major US indices eked out slight gains (DJIA +0.05%; S&P 500 +0.31%; Nasdaq +0.40%) overnight but the sharp paring back of early gains and the in-tandem rise of the VIX suggests that some caution remains. Ahead of the US Consumer Price Index (CPI) data release later this week, a drop in Treasuries saw the US 10-year yield reclaiming back above the 3% mark. This may potentially reflect some positioning for the upside risks to inflation ahead and the impending policy tightening moves to contain it, with the continued rise in bond yields translating into headwinds for risk sentiments.

While rate-sensitive growth stocks tend to come under pressure with surging yields, some pockets of resilience came from a 2% rise in Amazon’s share price during its first trading day after its 20-for-1 stock split. That may have lifted share prices for Alphabet and Tesla as well, with Alphabet stock split to be effective on 1 July while Tesla previously announced that it would ask shareholders to approve a split later this year. Other corporate news on watch include Twitter (-1.5%), with Elon Musk threatening to pull out of the takeover deal unless the company can prove that bots make up less than 5% of its users.

Overall, the relatively quiet schedule on the economic calendar yesterday and the ongoing Fed blackout period continue to see US equity markets trading in a holding pattern, with the symmetrical triangle pattern for the S&P 500 on the four-hour chart suggesting near-term market indecision. While some may see the formation of a bullish pennant which bodes well for S&P 500’s upside as a continuation pattern, one may potentially watch for any high-volume breakout of the triangle pattern over the coming days, which may provide greater clarity on where sentiments are headed.

Source: IG charts

Source: IG charts

Asia Open

Asian stocks look set for a weak open, with Nikkei -0.09%, ASX -0.67% and KOSPI -0.94% at the time of writing. Overnight, US-listed Chinese shares saw a boost from China’s ongoing economic reopening, along with a report suggesting that Chinese regulators are concluding its probe into DiDi. The Nasdaq Golden Dragon China Index is up more than 5%, although market confidence remains capped by the muted risk environment in Wall Street. DiDi shares were up more than 60% at the market opening before closing the US session with a 24% gain. The day ahead will bring focus to the Reserve Bank of Australia (RBA) interest rate decision as the key market event in the Asia session today.

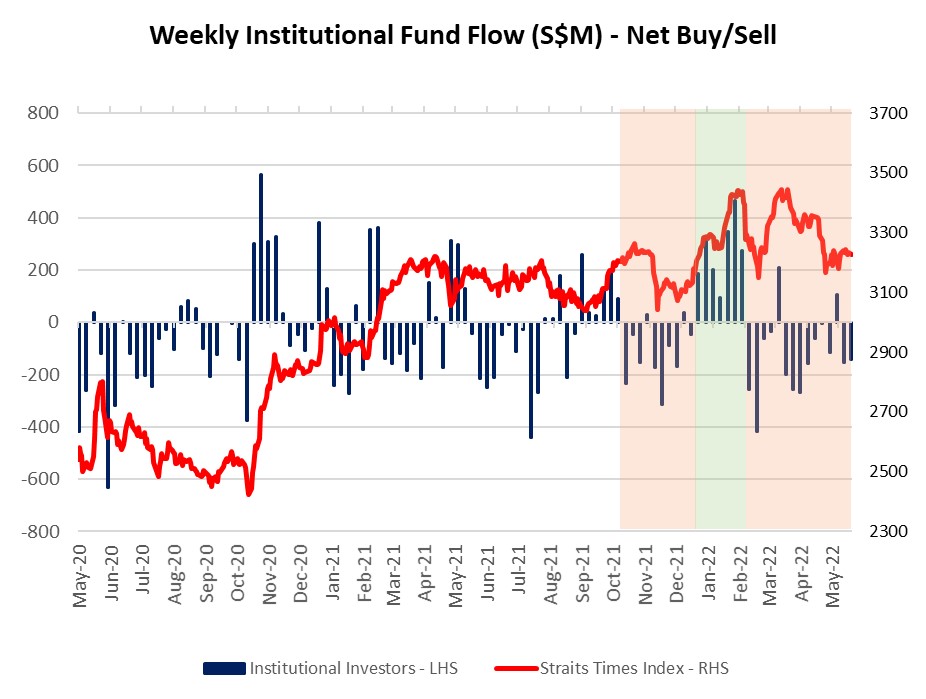

The latest SGX fund flow data revealed another week of net outflows from institutional investors in the STI, which may suggest that some reservations remain. The financial sector continues to see its 14th consecutive week of net outflows, with the cumulative fund positioning for the sector at the lowest level since March last year. On the technical front, the STI has been trading in a consolidation pattern over the past one month, which denotes some wait-and-see sentiments for now. A break out of the consolidation zone in either direction may potentially be looked upon as a signal for either the buyers or the sellers taking greater control.

Source: SGX, IG

Source: SGX, IG

Source: IG charts

Source: IG charts

On the watchlist: AUD/USD on watch ahead of RBA interest rate decision

Ahead of the RBA interest rate decision, the AUD/USD saw some easing overnight as a rise in US Treasury yields translated into strength for the US dollar. That said, the near-term upward trend remains intact for now, with the higher highs and higher lows formed since mid-May this year, with much to depend on the outcome of the RBA’s decision later. A 25 basis-point hike is largely expected by the markets based on the cash rate futures, while a 40 basis-point hike will be on watch to provide a hawkish surprise. Policy guidance ahead will also be in focus to drive expectations for subsequent meetings. Near-term, resistance for the AUD/USD stands at 0.727, where a key 38.2% Fibonacci retracement level is in place, while support may be found at the 0.710 level.

Source: IG charts

Source: IG charts

Monday: DJIA +0.05%; S&P 500 +0.31%; Nasdaq +0.40%, DAX +1.34%, FTSE +1.00%

.jpeg.98f0cfe51803b4af23bc6b06b29ba6ff.jpeg)

1 Comment

Recommended Comments

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now