US indices build on further gains overnight: EUR/USD, Brent crude, USD/JPY

Entry posted by MongiIG in Market News

1,206 views

US equity indices continue to build on their gains overnight, as subscribers’ resilience from Netflix paved the way for further outperformance in growth stocks.

Source: Bloomberg

Source: Bloomberg

Market Recap

US equity indices continue to build on their gains overnight, as subscribers’ resilience from Netflix paved the way for further outperformance in growth stocks, while defensive sectors underperformed amid the improved risk environment. Earnings from Tesla post-market was met with a lukewarm reaction in share price with an uptick of around 1.3%. For Tesla, increase in selling prices and ramping up of production to address backlogs provide a positive backdrop for overall outlook, but some margin headwinds were presented with a 5% decline in its automotive gross margins. On the macroeconomic front, eyes are on the restarting of the Nord Stream 1 gas pipeline from Russia to Europe, along with some simmering tensions on the geopolitical front as Russia intends to annex parts of Ukrainian territory.

Interest rate decision from the European Central Bank (ECB) will be in focus as well. With inflation approaching double-digit territory, the ECB has previously flagged that a bigger 50 basis-point (bp) is being brought to the table for discussion. Policymakers are still largely split on the scale of rate hikes, with a 50 bp hike potentially driving a knee-jerk reaction for the EUR/USD pair to the upside. Having traded within a descending channel pattern since February this year, dip buyers have stepped in last week to reject a fall below parity. This comes along with oversold technical conditions moderating to more neutral levels, with a bullish crossover on the moving average convergence divergence (MACD) and a reversion in the relative strength index (RSI) from oversold territory. The overall downward trend seems to remain, which could leave the 1.037 level on watch for any formation of a new lower high. This is also where the upper channel resistance stands in place.

Source: IG charts

Source: IG charts

Asia Open

Asian stocks look set for a mixed open, with Nikkei -0.34%, ASX -0.15% and KOSPI +0.18% at the time of writing. After the strong showing in Wall Street over the past two days, particularly so for tech stocks, markets may take somewhat of a breather. Lingering caution persists for Chinese equities amid both virus and property sector risks, with the Nasdaq Golden Dragon China Index down 0.8% overnight.

The day ahead will put interest rate decision from the Bank of Japan (BoJ) in focus, with the BoJ expected to continue on its path of policy divergence with other global central banks. Current market expectations are unanimously pricing for a no-change and looking further out, probability of a 0.10% rate hike is priced at only 4% for the September meeting while a 25% chance is priced for the October meeting. Thus far, concerns on the rapid weakening in yen continues to be highlighted by authorities but there has been a lack of any currency interventions after months of jawboning. With oil prices down as much as 24% recently from its June peak, the ongoing pressure for a stronger yen could see some alleviation, which may aid to substantiate a no-change to upcoming policies.

Brent crude prices continue to trade in a descending channel pattern, with a firm rejection off a key 61.8% Fibonacci retracement last week potentially driving a retest of the US$106.50 level next. This is where the upper channel trendline resistance stands in place with its mid-July peak. Any breakout from the channel will be on watch, which may point to a further shift in sentiments to the upside.

Source: IG charts

Source: IG charts

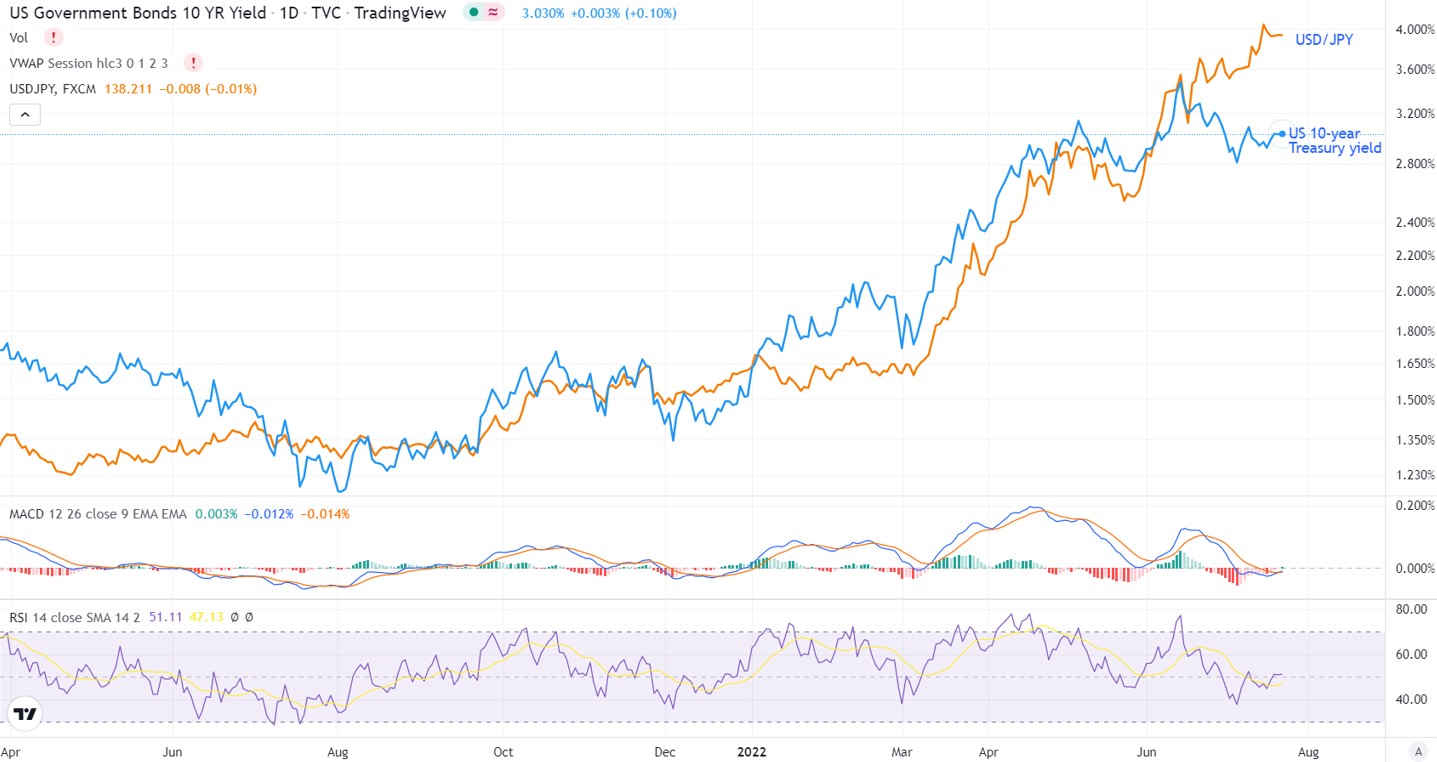

On the watchlist: Diverging relationship between US 10-year yields and USD/JPY

The USD/JPY pair tends to move hand-in-hand on a similar path to that of US 10-year yields, particularly since the start of 2021. This comes as Japan’s 10-year bond yield remains relatively well-anchored by its yield curve control (YCC) policy, while yield differentials stand as the key driver for the currency pair. That said, the relationship seems to have gone off-course lately, as gains in the US 10-year yields remain capped by recession worries while the USD/JPY continues to tick higher. This could leave the currency pair vulnerable to a near-term retracement if the relationship eventually holds and there were to be further downticks in the US Treasury yields. On the technical front, an upward channel keeps the USD/JPY in place. Further up-move could leave the 140.00 level on watch as its upper channel trendline could stand as near-term resistance to overcome.

Source: IG charts

Source: IG charts

Source: IG charts

Source: IG charts

Wednesday: DJIA +0.15%; S&P 500 +0.59%; Nasdaq +1.58%, DAX -0.20%, FTSE -0.44%

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now