US jobs preview: Will employment start to falter after technical recession?

Entry posted by ArvinIG in Analyst article

592 views

The US jobs report provides markets with a key update for markets as they seek to gauge whether the US economic decline is impacting the jobs market.

Source: Bloomberg

The July US jobs report is due to be released at 1.30pm, on Friday 5 August (UK time). Coming at a time when markets are enjoying a welcome boost from a largely better-than-expected earnings season, we see the focus come back to the current state of the economy on Friday. Traders will be wondering whether this recent rebound in stocks marks the bottom for markets, yet much of that will be determined by the inflation and wider economic statistics that determine how the Federal Reserve (Fed) reacts going forward.

With the US recently entering a ‘technical recession’ of two consecutive negative gross domestic product (GDP) readings, some stipulate that we will only enter a real recession once we see a significant uptick in unemployment. For traders, the fact that a stronger economic picture allows for greater monetary tightening from the Fed means that the reaction to a better-than-expected jobs data could be negative for stocks, yet positive for the dollar.

With markets fearing a worrying that we could be on the cusp of a collapse in the jobs market, traders will be watching this report closely across a number of factors. Taking a look at some of the secondary surveys can give us an insight into exactly what we might see when the headline figures emerge on Friday.

What do other employment surveys tell us?

It is often useful to look out for clues within alternate employment readings, with the Conference Board survey, jobless claims, and ISM purchasing managers' index (PMI) surveys all worth analysing ahead of the main event.

Conference board survey

Let's look at the latest ‘Conference Board’ survey for July, with the ratio between those finding it difficult to obtain work vs easy to obtain work providing a good proxy for unemployment. As the chart shows, the Conference Board ratio has been reversing upwards over the past four months. With that ratio up to the highest level in almost a year, there is a clear risk that we will soon see unemployment turn upwards.

ADP payrolls

ADP are taking a break from publishing their employment report, with the firm expected to return to action next month.

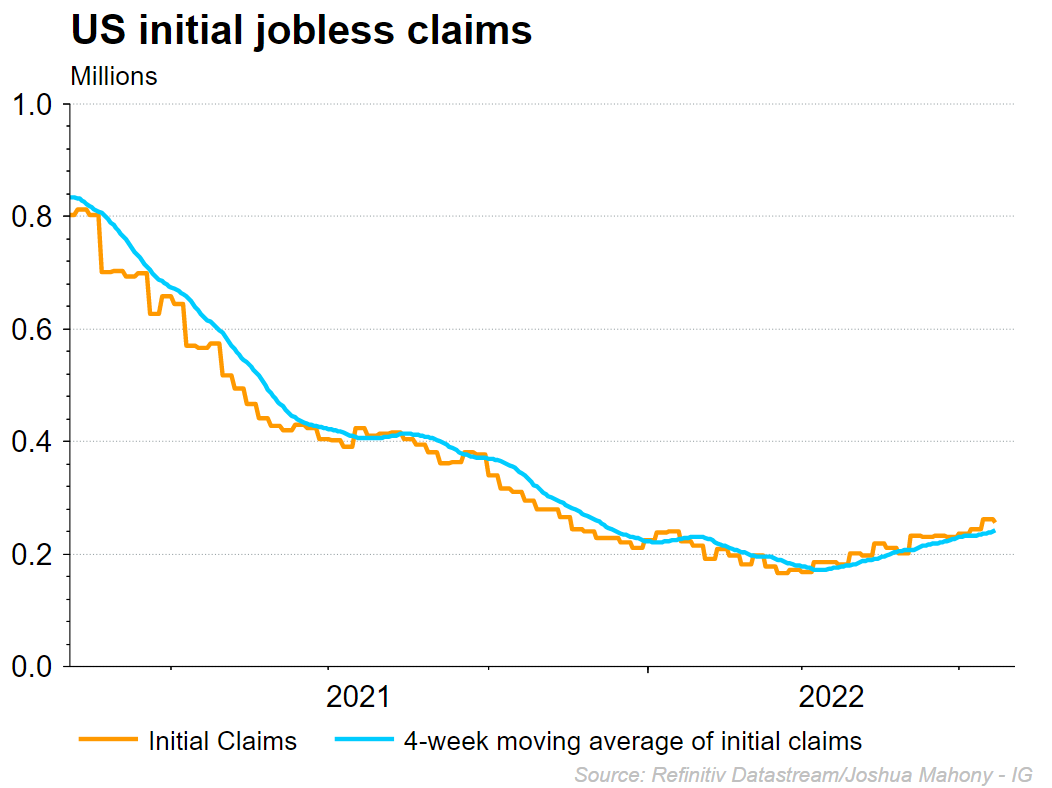

Initial jobless claims

Initial claims have been on the rise over since bottoming out in April, with that trend continuing to take place. The push higher in jobless claims does bring expectations that we could see payrolls drift lower and unemployment could tick higher.

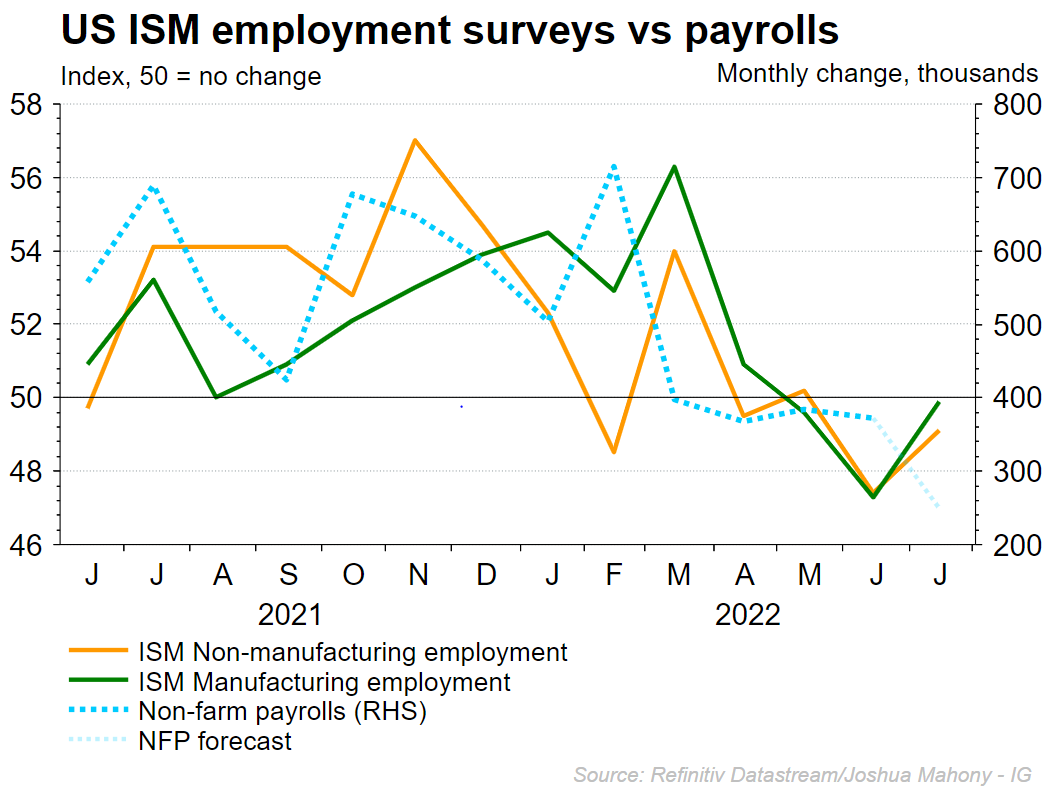

ISM PMI surveys

The latest ISM surveys have seen a welcome rise across both manufacturing and services employment readings. It is useful to utilize the ISM survey owing to the fact that they do separate out the employment element unlike the headline release. While both readings have managed to push higher in July, we can see that they remain in contraction territory. Nonetheless, with the contraction in manufacturing and services employment apparently easing, it could signal that the decline in payrolls could be less severe than expected.

US employment breakdown

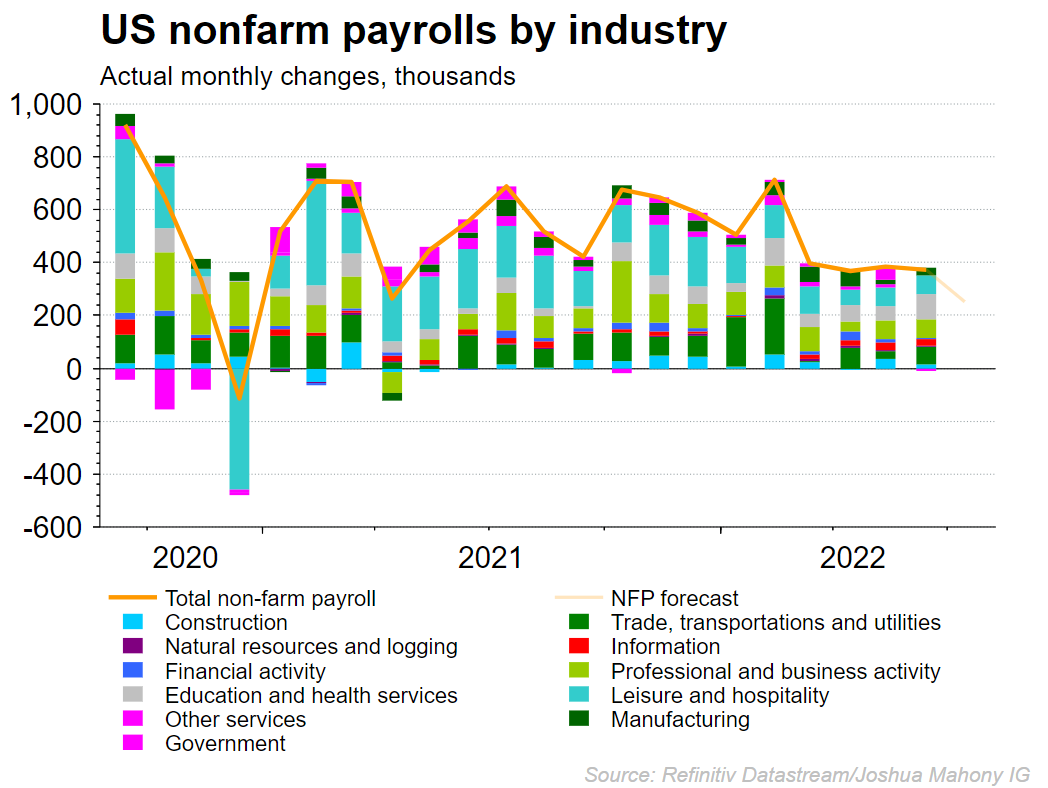

It is important to understand the relative importance of the services and manufacturing sector when gauging the two ISM surveys above. We can see below that service-related jobs account for almost 75% of all US jobs, with manufacturing representing just 10% of employment in the country according to the latest jobs report. With that in mind, it makes sense to attach greater importance to the services sector employment outlook over those elsewhere. This has become increasingly the case over the course of the Covid-19 pandemic.

Non-farm Payrolls

The headline non-farm payrolls figure is expected to fall back this month, with markets predicting a figure of 250,000 after the last reading of 372,000. Coming off the back of four readings within the 300,000 - 400,000 range, a figure of 250,000 would be a notable shift from the recent norm.

Unemployment

From an unemployment perspective, markets are expecting to see the rate remain at 3.6% for the fifth consecutive month. However, the move higher for both the Conference Board ratio and unemployment claims do signal a potential uptick before long. When that does finally break, markets will likely pay close attention as it would signal the potential beginning of an employment crisis that we are yet to see.

US earnings

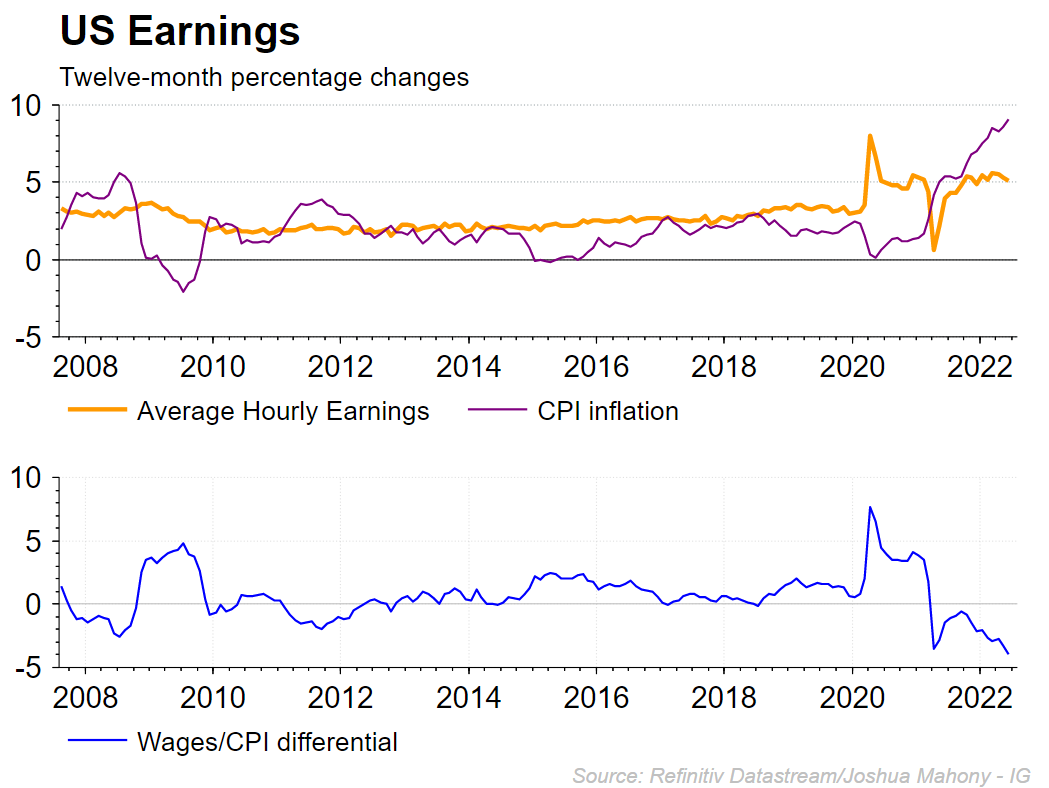

US wages will be keenly followed as a proxy for cost push inflation going forward. We have seen wild swings across this metric throughout Covid-19 pandemic, but much of that has been associated with the sharp decline and rise in jobs throughout the services sector. This time we are looking out for whether businesses will be seeking to compensate their workers for the rising prices seen throughout the economy.

The second section within the chart highlights the gap between headline inflation and wage growth, with the current relationship providing the widest divergence in more than 15 years. That highlights the historical squeeze we are seeing on disposable income in the US. Markets are expecting to see wage growth to remain at 5.1%, but any significant divergence could be taken as a clue over inflationary pressures going forward.

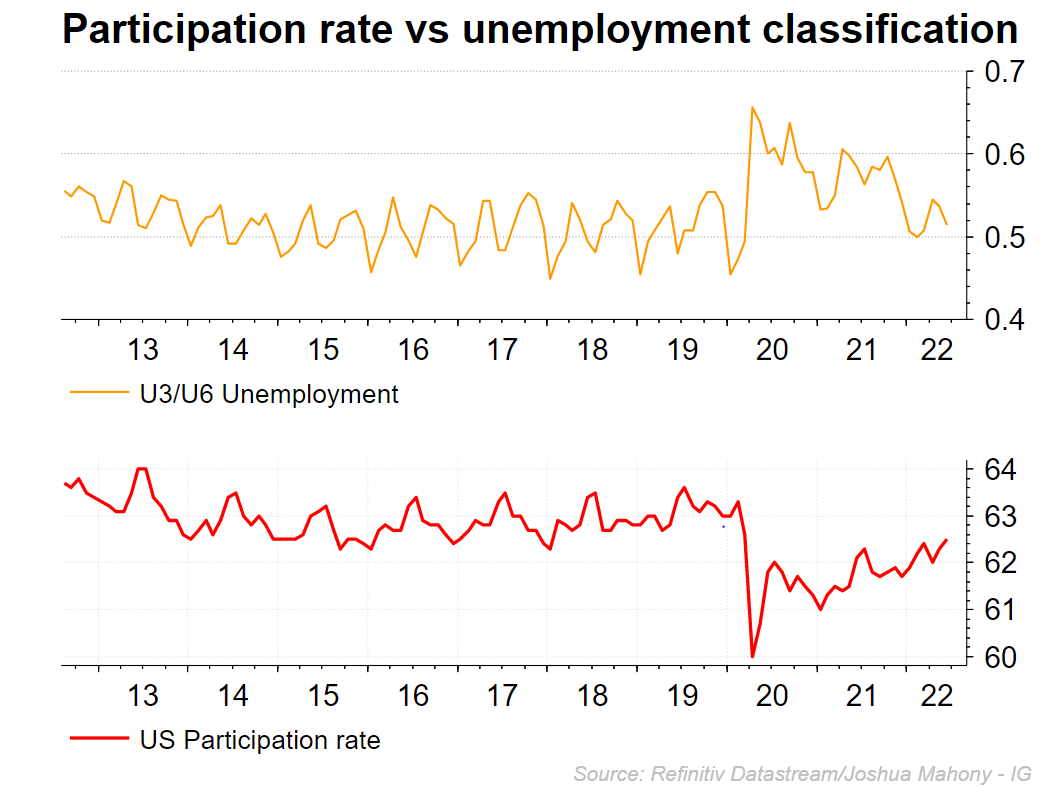

Participation rate

The recent cost of living crisis has ramped up pressure on households as disposable income levels are squeezed in response to rising costs. However, this looks like it could help drive workers back into employment, pushing the participation rate higher. The chart below highlights how we have seen the participation rate move upwards after the initial collapse around the inception of the Covid-19 pandemic.

Markets are expecting to see the participation rate remain at 62.2% at this meeting. Notably, we can see that the ratio between U-6 unemployment (% of those looking for work) and U-3 unemployment (% of all workers) provides method of measuring participation in the jobs market.

Dollar index technical analysis

The dollar index has been on the back foot of late, with risk assets on the rise at the expense of havens like the greenback. While Nancy Pelosi has done her best to hamper that move, we are seeing the bears come back into play at the 76.4% Fibonacci resistance level here. With the stochastic rolling over from overbought territory, there is a good chance we see some weakness for the dollar. A break through the 107.14 level would be required to negate that bearish short-term outlook.

Source: ProRealTime

DJIA technical analysis

The Dow continues to climb as we head up towards the crucial 33461 resistance level. A break above that point would bring about a wider bullish outlook for the index. To the downside, we would need to break below the 31694 level to negate the recent bullish trend.

Source: ProRealTime

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now