Bank of Japan (BoJ) preview: no-change remains as consensus, with focus on yen intervention

Entry posted by MongiIG in Market News

677 views

The BoJ is set to hold their monetary meeting across 21 – 22 September 2022, with any hints on yen intervention likely to be the focus.

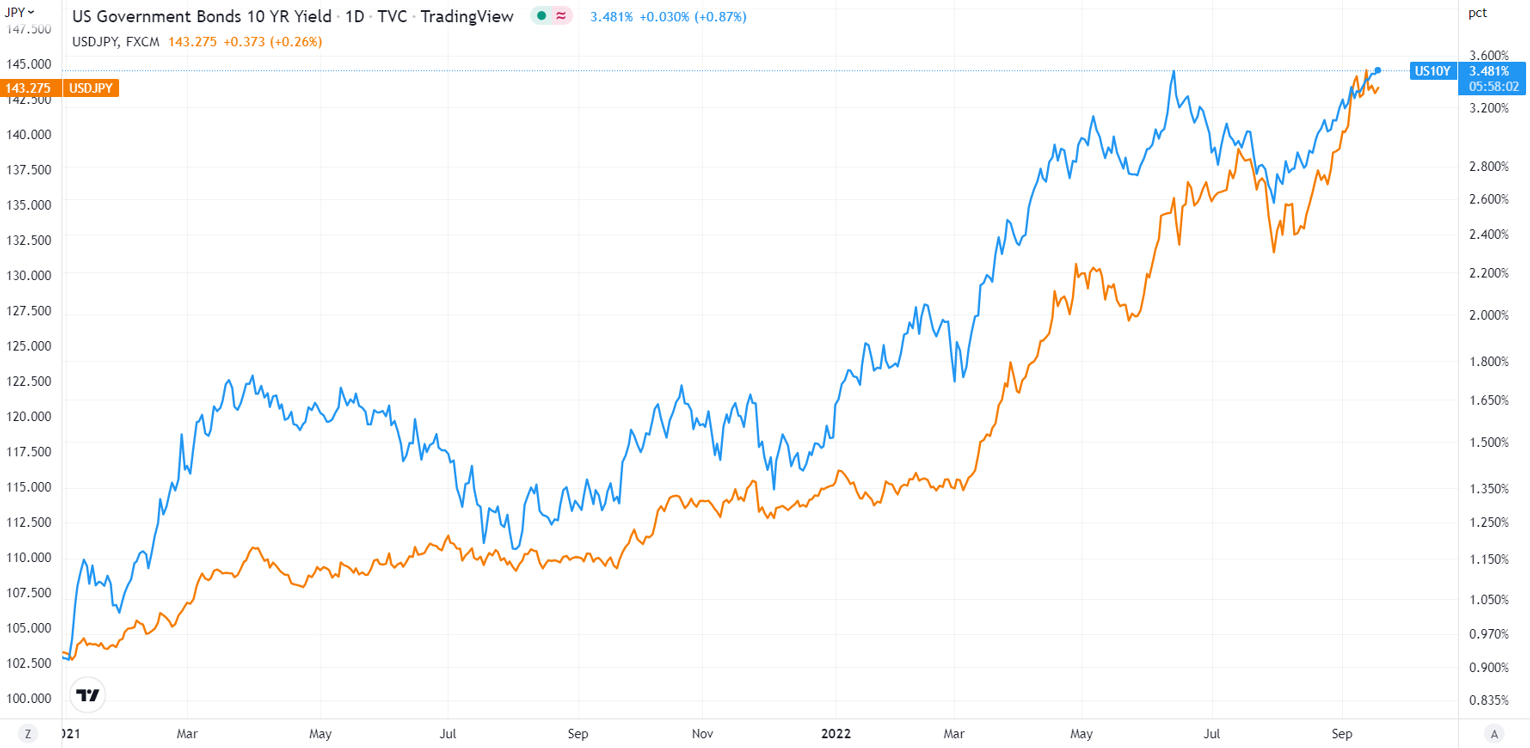

Source: Bloomberg

Source: Bloomberg

No-change in policy stance still the consensus despite 3% inflation

Despite a more aggressive shift in rate hike expectations among major economies, particularly the US Federal Reserve (Fed) after its hot inflation data, the current consensus is for the Bank of Japan (BoJ) to remain the outlier. A no-change to its accommodative monetary policies is expected in its upcoming meeting and looking further out, probability for a 0.1% increase in its short-term interest rate remains priced at a mere 11% probability in the October meeting and a 21% probability in December.

Japan’s recent headline inflation of 3% has shown a further pull-ahead from the central bank’s 2% target, which could seem to translate into more pressure for the central bank to shift away from its accommodative policies. The core aspect revealed some persistence as well, coming in slightly higher than expected at 2.8%. That said, a moderation in August import prices and a slowdown in Japan’s average wage to 1.8% year-on-year (YoY) growth from previous 2% could still be looked upon to justify the lower-for-longer policy stance. The BoJ Governor Haruhiko Kuroda previously mentioned that he wanted to see a ‘stable and sustainable rise’ in both wages and prices before considering any policy shift. Until then, pricing pressures could continue to be shrugged off as commodities-driven and temporary, with rising energy and processed food costs accounting for most of the YoY increase with its latest inflation readings. Further move above 3% for inflation rate over the coming months could increase the pressure for a policy shift, therefore market participants will be keeping a lookout for any shift in tone from policymakers.

Yen weakness remains the key focus

With the USD/JPY hovering at its 24-year high, any hints of currency intervention measures by the BoJ will be the focus of the meeting. Several jawboning attempts on the weak yen have surfaced since the start of the year, with a further step-up in rhetoric recently being a rate check conducted with banks. That said, the numerous occasions presented through the year suggests that while it may drive a knee-jerk reaction in lifting the yen, the lack of any concrete follow-through by the BoJ may eventually leave the upward trend for USD/JPY intact, with sentiments tracking closely to moves in the US 10-year Treasury yields. Concerns on the weak yen may continue to be highlighted in the meeting by policymakers, but greater follow-up action is what market participants are looking out for, which seems to be unlikely for now.

USD/JPY: some wait-and-see sentiments in the lead-up to FOMC meeting

Yield differential on policy divergence continues to be the key driver for the pair, as sentiments take its cue from the US 10-year Treasury yields with the Japan’s yield curve control policy firmly in place. A recent retest of its 24-year high at the 145.00 level was met with some consolidation, as some wait-and-see sentiments surface ahead of the Federal Open Market Committee (FOMC) meeting this week. The 145.00 level marks a peak back in 1998, where a previous round of intervention was in place to address the weak yen at the time. While a bearish moving average convergence divergence (MACD) crossover was formed on the daily chart, along with a bearish pin bar on its weekly timeframe, a close below the 141.50 level could be warranted to bring about a retracement to the 138.00 level next. Fundamentally, we may need to see signs of peak hawkishness from the Fed or a policy shift from the BoJ, in which both seems to be off the table for now. Therefore, the ongoing upward trend suggests that in the event of a retracement, looking out for the formation of a higher low could be the preferred approach.

Source: TradingView

Source: TradingView

Source: IG charts

Source: IG charts

Nikkei 225: likely to take its cue from global risk environment

With a no-change in policy stance widely expected to remain for now, the Nikkei 225 index may be more likely to take its cue from the global risk environment. There were some attempts to stabilise this morning after the 4.3% heavy sell-off last week, but the sharp paring back of earlier gains suggest that overall sentiments remain fragile. Failure for the upward trendline to hold over the coming days may prompt a move lower to the 27,000 level next, where a 38.2% Fibonacci retracement level potentially stands as the next line of support.

Source: IG charts

Source: IG charts

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now