Investor Spotlight: US earnings season update

Entry posted by MongiIG in Market News

1,023 views

A review of last week, and a look at the week ahead: corporate earnings are beginning to reflect recession risks.

This issue of Investor Spotlight is brought to you by IG, with Kyle Rodda, Market Analyst and ausbiz presenter.

Corporate earnings are beginning to reflect recession risks. In this week’s Investor Spotlight, we review last week’s earnings, check in on the overall performance of the S&P 500, and look ahead to the big results for the week.

Reviewing last week’s results

The middle of the earning season, wedged between the tech giants and big consumer stocks, can sometimes bring with it a lull.

Following the shocking performances of the likes of Alphabet, Amazon and Microsoft, investors have become nervous about what the rest of the reporting period will look like.

Uber

Uber was arguably the major bellwether to report its quarterly earnings last week. The company delivered a strong result for the quarter, driven by rising demand for travel and leisure as the restriction of the pandemic subsided.

Monthly active users rose 14%, underpinning revenues of $8.34 billion. The bottom line result was weaker than expected, with the company reporting a loss of $0.61 per share. However, it was the guidance that satisfied the markets, with Uber’s guidance for Q4 operating profits exceeding forecasts.

Uber shares clearly remain within a downtrend. However, there are signs of a possible reversal, with the weekly RSI moving higher and the price carving out a series of higher lows.

Uber weekly chart

Source: IG

Source: IG

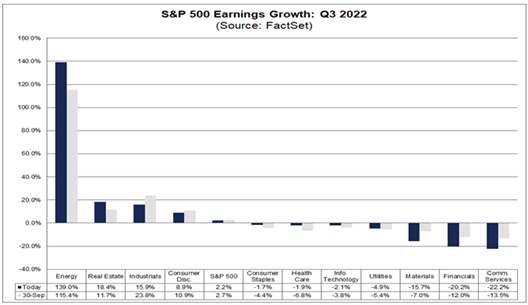

Checking in on the S&P500

It has been a disappointing reporting period for Wall Street so far. As of November 4th, data compiled by Fact Set suggests that EPS growth for Q3 ought to come in at a paltry 2.2%. This comes despite stronger than forecast revenues, with corporate bottom lines compressed by a higher cost environment.

Source: FactSet

Source: FactSet

Seven of eleven sectors will likely post negative earnings growth for the quarter. Energy companies, whose profits have been padded by surging energy prices amidst the war in Ukraine, will be the only sector to markedly outperform expectations.

71% of firms have exceeded analyst estimates, which is below the long-run average.

Of most concern is the lowering of guidance by companies, as many management teams brace for slowing demand. The same numbers produced by FactSet suggest analysts are now forecasting a one percent contraction in earnings for the fourth quarter.

Despite a week of earnings season, the S&P 500 has rallied throughout the reporting period, thanks to hopes of a slower rise in US interest rates.

The index remains in a downtrend, with key support at 3500 and major resistance at 3900.

S&P 500 weekly chart

Source: IG

Source: IG

The week ahead

It will be another relatively light week on the earnings calendar, as investors steel themselves for the likes of Walmart and Home Depot at the end of the reporting season.

The big name for the week will be Walt Disney Co., which will report after the bell on Wednesday, AEST. According to Reuters data, analysts are forecasting annual earnings growth of 47.23% with EPS tipped to be $0.54 for the quarter. Revenue is expected to climb 14.64% to $US21.25 billion.

The company's results will be used as a barometer for leisure spending, consumer confidence and travel, along with a read on the streaming wars. Guidance will therefore be crucial, especially as quarterly EPS is forecast to decline for this quarter, but pick up again going forward, despite the risk of a recession in the US.

Like the broader market, Walt Disney remains in a downtrend. Strong support has emerged at

$90.00, with a resistance zone between $110 and $115.

Disney weekly chart

Source: IG

Source: IG

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now