Singapore’s outlook: What to watch in 2023?

Entry posted by MongiIG in Market News

793 views

After retracing close to 15% from its March 2022 peak, the STI has put up a strong showing in Q4 2022. What are the key themes to watch in 2023?

Source: Bloomberg

Source: Bloomberg

After retracing close to 15% from its March 2022 peak, the Straits Times Index (STI) has put up a strong showing in quarter four (Q4) 2022, recovering more than half of its losses since late-October. That makes the STI one of the few indices to deliver a positive year-to-date performance, with a return of 4.7% at the time of writing. Heading into 2023, here are some key themes to watch.

Economic outlook under threat from external conditions: Down but not out

As an open economy, the global moderation in economic conditions could continue to have a negative impact on growth in 2023. Recent forecasts from the Ministry of Trade and Industry (MTI) point towards gross domestic product (GDP) growth of 0.5-2.5% next year, which is significantly lower than the 10-year historical average of 3.3%. That said, there may be some pockets of optimism that at least for now, a recession is not the base case for Singapore, while key markets such as the US and Europe are under higher recession risks.

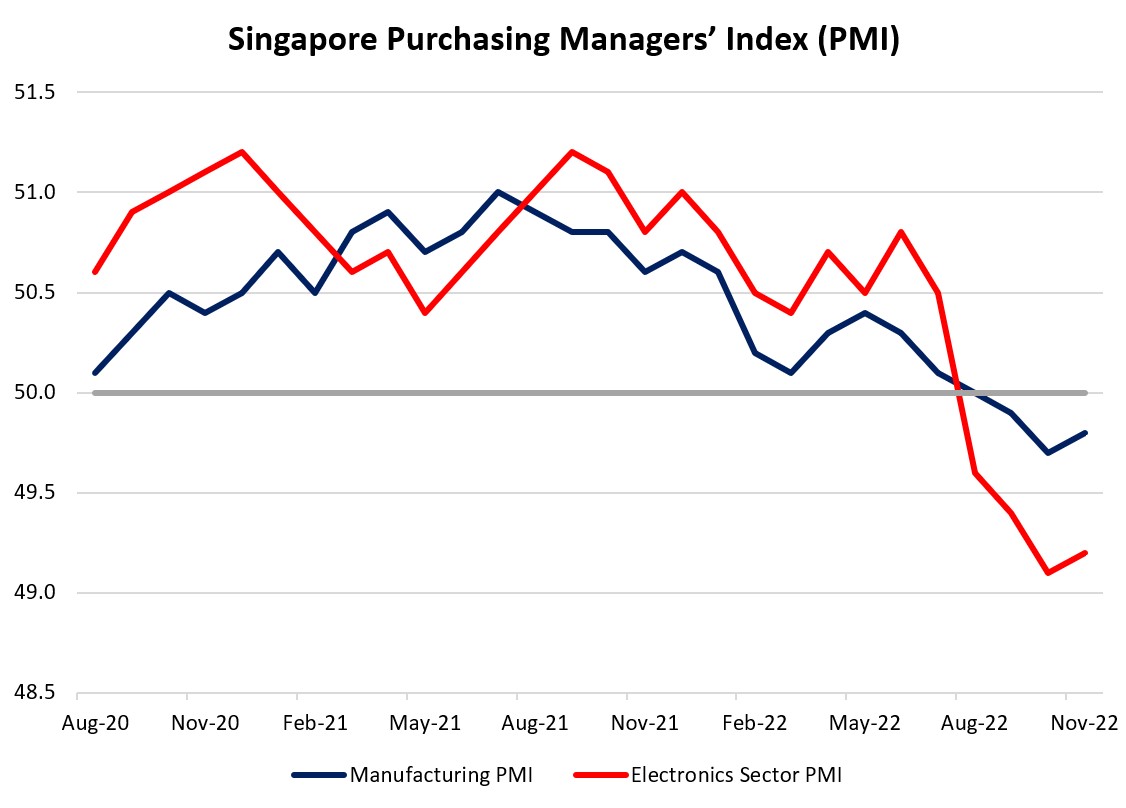

Looking ahead, Singapore’s Purchasing Managers' Index (PMI) figures has reflected the third straight month of contraction in manufacturing activities in November, which could likely remain under pressure into first half (1H) of 2023. This comes as global interest rates continues to push into restrictive territory, albeit at a slower pace, while lagged responses to tighter policies continue to seep into economic conditions. Further moderation in corporate earnings may pose a headwind for risk-taking. However, the outlook could brighten into second half (2H) of 2023. Current Refinitiv estimates are for US headline inflation to head towards 5.9% by quarter one (Q1) 2023 and 4.0% by quarter two (Q2) 2023, which could bring less pressure for the Federal Reserve (Fed) to defend their higher-for-longer rate stance. Any supportive signs that the worst-is-over in corporate earnings will remain on watch as well.

Source: Singapore Institute of Purchasing and Materials Management (SIPMM)

Source: Singapore Institute of Purchasing and Materials Management (SIPMM)

China’s reopening as big theme in 2023

Closer to home, while there are ongoing progress towards a gradual reopening in China, intermittent virus waves as a result of easing measures may still pose some risks to consumer spending recovery and disruptions to factory activities in the near term. The upcoming festive Chinese New Year could draw in some temporary measures from authorities to mitigate healthcare overload as well. But nevertheless, the greater shift in focus from authorities towards economic conditions marks a positive step over the longer term, which could aid to provide some cushion for Singapore’s exports and international travel. Since 2013, China has been Singapore’s largest trading partner.

Institutional fund flow: Financials preferred over REITs this year. Will the narrative change in 2023?

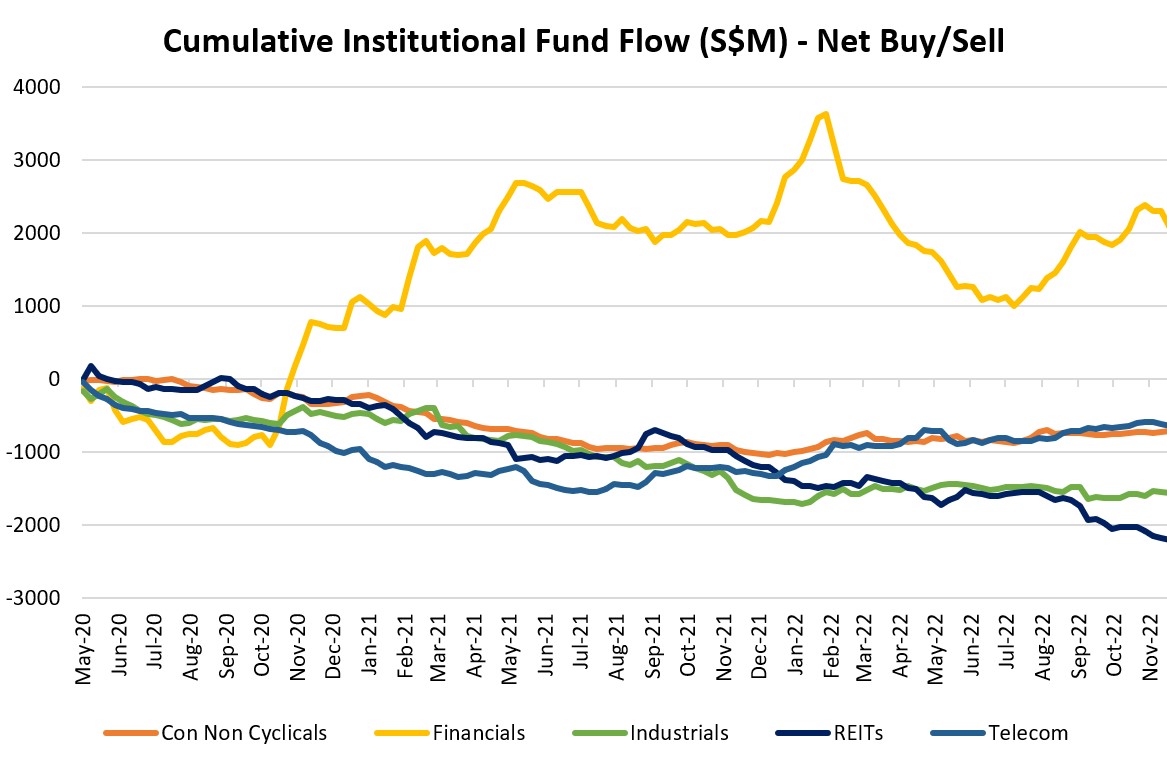

This year, the narrative for higher-for-longer rates has seen institutional net inflows leaning towards financials while REITs are largely being shunned. This comes as local banks are able to enjoy higher net interest margins in an interest rate upcycle environment, while higher debt costs are perceived to be a headwind for REITs. Going into 2023, this brings into question whether a potential peak in interest rates will bring the much-needed clarity to draw inflows back into the REITs sector. Year-to-date, performance for the iEdge S-REIT Index remains underwater by 16.3%, with increasing number of more stable REITs delivering dividend yields in the 5-7% range. Greater clarity on the eventual terminal interest rate and any less bad than feared economic environment could be on watch in 2023 to draw renewed traction back into the sector.

Source: SGX, IG

Source: SGX, IG

Technical analysis: Straits Times Index still hanging below pre-Covid levels

Despite the recent 11% rebound since late-October this year, the STI is still hanging just below its pre-Covid level at the 3,287 level. A bullish break above a downward trendline was met with a period of consolidation, as the index fell into a tight range between the 3,320 upper bound and the 3,230 lower bound. Any break in either direction could be on watch ahead, which could signal a clearer direction of control.

Source: IG charts

Source: IG charts

Technical analysis: USD/SGD struggles for upside

With further unwinding of bullish bets in the US dollar on the peak hawkishness narrative, the USD/SGD has hit its nine-month low. Recent dip-buying efforts with the formation of a bullish hammer candlestick last week came short-lived as sellers were quick to challenge the 1.341 level once more. Technical conditions are treading in oversold territory, but a fundamental catalyst supportive of US dollar upside seems much needed at current point of time. The upcoming Fed meeting will be on close watch ahead. Failure for the USD/SGD to defend the 1.341 level over the coming days could prompt a move towards the 1.320 level next, which marks its lows back in 2021.

Source: IG charts

Source: IG charts

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now