Bank of Japan (BoJ) preview: Clarification to be sought for BoJ Governor’s previous comments

Entry posted by MongiIG in Market News

331 views

The BoJ is set to hold their monetary meeting across 21 – 22 September 2023, with focus on any further tweaks in BoJ Governor Kazuo Ueda’s tone, following July adjustment.

Source: Bloomberg

Source: Bloomberg

What to expect at the upcoming Bank of Japan (BoJ) meeting?

The BoJ is set to hold their monetary meeting across 21 – 22 September 2023, with wide consensus for its short-term interest rate target to be kept unchanged at -0.1% and that for the 10-year bond yield around 0%.

But with the BoJ Governor Kazuo Ueda floating the idea that the central bank could have enough data by year-end to determine whether to end negative rates, market participants seem to perceive it as an imminent rate raise into early-2024. The absence of fresh economic projections at the upcoming meeting may leave greater weight to the communications at the press conference to determine if such timeline of a policy pivot is validated or market participants could have potentially misinterpreted Kazuo Ueda's previous comments.

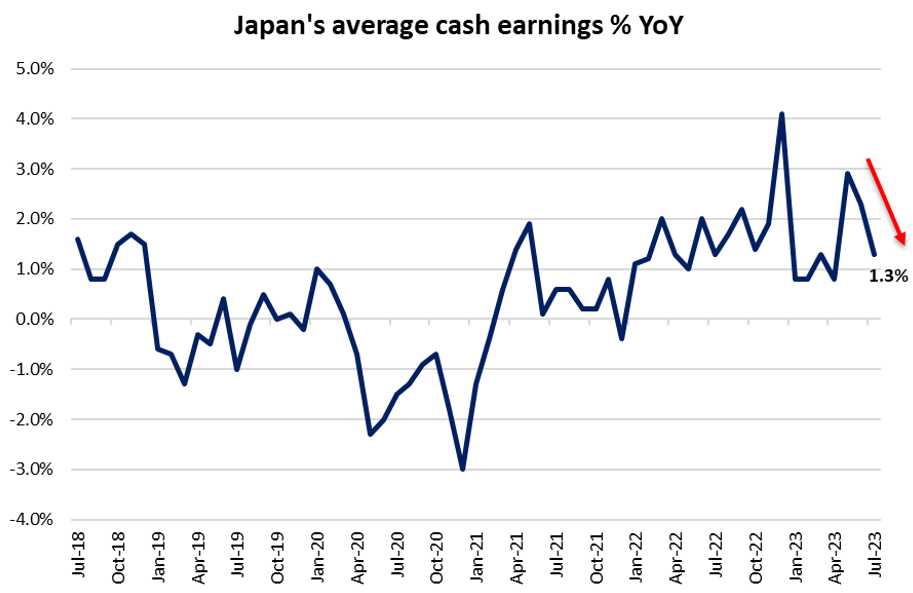

Current market rate expectations are leaning towards a 55% probability that the BoJ may end its negative interest rate in the first quarter of 2024. With that, any upward build in wage pressures towards the rest of the year will be on watch to determine if the central bank’s ‘sustainable wage growth’ condition for a policy change is met.

Source: Refinitiv, as of 20 September 2023.

Source: Refinitiv, as of 20 September 2023.

Japanese 10-year bond yields at fresh nine-year high, but policy normalisation may be gradual

A fresh nine-year high in Japanese 10-year government bond yields reflects hawkish expectations in place for an eventual policy normalisation, but current muted moves in the implied volatility for the 10-year government bonds futures suggest that any policy changes may not take place at the upcoming meeting potentially just yet.

Instead, market participants will be keeping an eye on any further tweaks in tone coming from the BoJ Governor Kazuo Ueda. Back at its July meeting, he guided for more flexibility around its yield curve control (YCC) scheme, referring to the plus-minus 0.5% band around its 10-year bond yields target as just “references”. The central bank has also offered to purchase 10-year JGBs at 1.0% every business day through fixed rate operations.

Source: TradingView

Source: TradingView

Given that the BoJ still emphasised on patience in its policy stance, phasing out its YCC policy may still be a gradual process in their view, which may call for some wait-and-see at the upcoming meeting given earlier tweaks in July. This is further supported by recent moderation in wage pressures, which does not provide any conviction around the condition of sustainable wage growth just yet.

While Japan’s core-core inflation has remained sticky at 4.3% in July, but excluding energy costs, the other core segments are still on a broadly moderating trend, offering some room for policymakers to hold their fire, at least for now. In July, Japan’s core inflation came in at a four-month low of 3.1% year-on-year.

Source: Refinitiv

Source: Refinitiv

USD/JPY: Heading to a new year-to-date high

The USD/JPY has registered a new year-to-date high this week, with the pair surpassing the 145.00-145.80 range, where the BoJ had intervened with US$19.7 billion of yen-buying back in September 2022. That has prompted speculations of more intervention, although any excitement could easily die down without the lack of any concrete follow-through.

Having traded in an upward channel since the start of the year, further Fed-BoJ policy divergence displayed this week may leave a retest of the 150.00 level in sight, as a key resistance to overcome. This is where the upper channel trendline resides, while it also marks a key psychological level where the BoJ intervened with a larger US$42.4 billion worth of yen-buying in October 2022, which triggered the formation of a near-term top for the USD/JPY.

On the downside, the 145.80 level will serve as an immediate support level to hold. Staying above its Ichimoku cloud pattern and various moving averages on the daily chart still leaves an upward trend intact for the pair, although recent lower highs on relative strength index (RSI) may point to some near-term exhaustion/indecision for now.

Source: IG charts

Source: IG charts

Nikkei 225: Bullish flag formation remains in place

After a short blip early this month, the Nikkei 225 index has seemingly found support off the lower edge of its Ichimoku cloud on the daily chart to trigger a break above a near-term descending channel consolidation pattern. On the broader scale, a bullish flag formation seems to remain in place.

Any pushback against recent hawkish bets at the upcoming meeting could likely be met with a positive reaction in the index, which may leave its year-to-date high at the 34,000 level on watch for a retest ahead. On the downside, the upper channel trendline may now serve as a resistance-turned-support at the 32,800 level for buyers to defend.

Source: IG charts

Source: IG charts

This information has been prepared by IG, a trading name of IG Markets Limited. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients. See full non-independent research disclaimer and quarterly summary.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now