Apple’s Q4 earnings preview: Can services revenue counteract weak product sales?

Entry posted by MongiIG in Market News

575 views

Being one of the "Magnificent Seven" stocks which account for the bulk of the US indices’ gains year-to-date, its upcoming earnings may play a crucial role in determining the indices’ trend into year end.

Source: Bloomberg

Source: Bloomberg

When does Apple Inc report earnings?

Apple Inc is set to release its quarter four (Q4) financial results on 2 November 2023, after market closes.

Apple’s earnings – what to expect

Current market expectations are for Apple’s Q4 revenue to decline marginally by 1% year-on-year to US$89.3 billion versus US$90.1 billion a year ago.

On the other hand, earnings per share (EPS) is expected to be at US$1.39, up 7.7% year-on-year and 10.3% from the previous quarter. Its Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margin is expected to improve to 32.2% as well, up slightly from the previous quarter’s 31.9%.

Being one of the "Magnificent Seven" stocks which account for the bulk of the US indices’ gains year-to-date, its upcoming earnings may play a crucial role in determining the indices’ trend into year end.

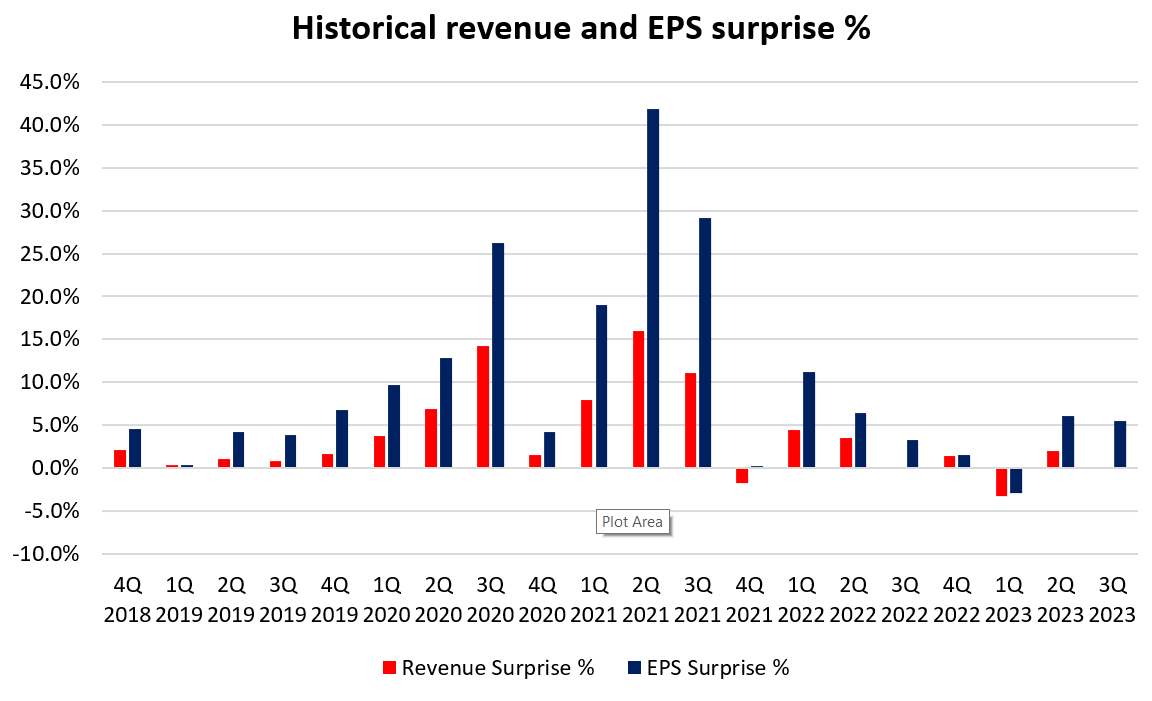

Apple generally has a strong record of outperformance, only failing to meet earnings estimates once over the past 20 quarters. That said, recent sell-off in big tech share prices despite delivering top and bottom beat reflects that market participants also have a high bar as to whether current earnings momentum can be maintained ahead.

Source: Refinitiv

Source: Refinitiv

Apple’s hardware product sales may continue to struggle

The Greater China market accounts for one-fifth of Apple’s revenue last year and thus far, there are not much conviction that demand on that front can hold up just yet. A report from Counterpoint Research suggests that iPhone 15 sales for the first 17 days of sales in China has underperformed last year’s iPhone 14 (an estimated 4.5% lower). Unit sales of the higher-end Pro Max and Pro are down 14% and 11% versus last year.

Apart from attributing the weaker iPhone demand to cautious Chinese consumers, Huawei’s newly launched Mate 60 series has also proved to be strong competition. Reports suggest that Huawei’s smartphone sales growth has increased 37% year-on-year in Q3 2023 (versus Apple’s estimated 10% decline), as its new Kirin chips as a response to US tech sanctions seem to be well-received. If China’s recent efforts to restrict the use of iPhones for government officials and employees at state-owned enterprises were true, further US-China tech decoupling may remain a risk to China’s iPhone demand ahead.

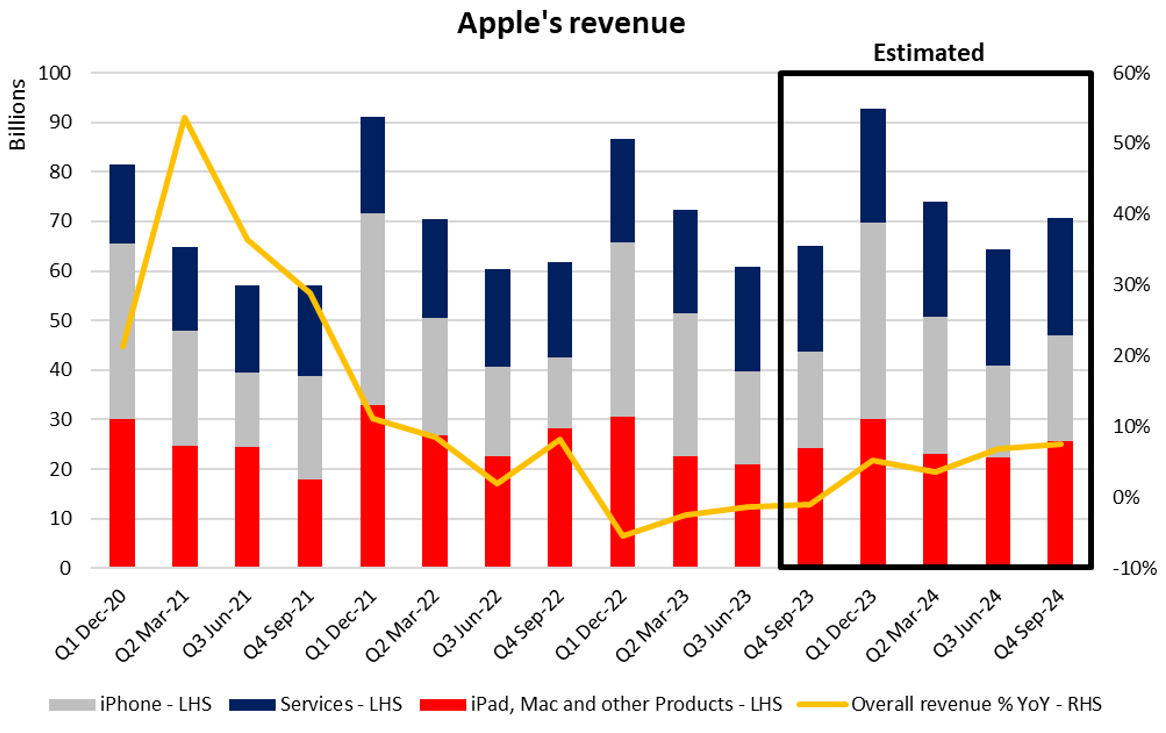

The bright side is that on the other end of the globe, reception for the iPhone 15 series in the US (Apple’s main market) may offer some cushion with estimated double-digit increases from a year ago. Current expectations are that the overall net effect may still drive a slightly lukewarm 2.4% year-on-year increase in iPhone revenue for the Q3 2023 results. On the other hand, other hardware products are expected to weigh for longer, with further contraction to be presented from a year ago (estimated iPad -14.6%, Mac -24.7%, other products -2.2%).

Source: Refinitiv

Source: Refinitiv

Services business to remain the bright spot

Perhaps not much of a surprise, in line with the prevailing trend, expectations are for the growth in Apple’s services business to continue accelerating to 11.4% year-on-year in Q3 2023, up from the previous quarter’s 8.2%. This segment has been the crown jewel for Apple in recent years, being its highest-growth and highest-margin business, along with a recurring revenue-generating model. It includes subscriptions, warranties, licensing fees and Apple Pay.

Thus far, growth in its paid subscriptions continues to show strong momentum, rising by 150 million in the last year to surpass the one-billion mark and setting an all-time revenue record in the last reporting quarter.

Guidance for growth catalysts on watch, but more for longer term

Any guidance around Apple’s growth catalysts will also remain on watch to diversify the company’s revenue stream further away from iPhone sales (48.5% of total revenue) over the longer term. It has previously announced its Apple Vision Pro headset, which is expected to launch early next year.

Apple is also tapping on its huge user base to include financial services as part of its ecosystem, offering a high-yield saving account program for Apple Card holders. Previous quarter’s guidance showed that customers were already making more than $10 billion in deposits.

More notably, its work on generative Artificial Intelligence (AI) may be in greater focus. Given that the company is reportedly working on multiple AI models across several teams and investing millions of dollars per day, any fresh updates on any generative AI tools, models or services will be on close watch.

Technical analysis – Trading below its 200-day MA for the first time since March 2023

Apple’s share price has broken below its Ichimoku cloud support on the daily chart back in August this year and subsequent attempts to reclaim the cloud zone have been unsuccessful ever since. That seems to keep a downward bias intact for now, with its weekly Relative Strength Index (RSI) crossing below the key 50 level last week, while its closely-watched 200-day moving average (MA) has also given way.

Buyers will now face the arduous task of having to reclaim the 200-day MA back in order to provide some conviction of near-term upside. Failing which, prices may potentially head lower to retest the US$161.04 level, where a near-term lower channel trendline may coincide with a key Fibonacci retracement level.

Source: IG charts

Source: IG charts

This information has been prepared by IG, a trading name of IG Markets Limited. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients. See full non-independent research disclaimer and quarterly summary.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now