Dow 30: not too far off the highs ahead of a significant week

Entry posted by MongiIG in Market News

309 views

Technicals remain bullish even as it avoids record highs, while CoT speculators are back to raising their majority buy bias.

Source: Bloomberg

Source: Bloomberg

Manufacturing data diverges, cautious Fed members, and the monetary policy report

Quite a bit to digest late last week where manufacturing data painted a conflicting picture, with ISM’s (Institute for Supply Management) PMI (Purchasing Managers’ Index) still in contracting territory and worsening to 47.8 from 49.1, even as S&P Global’s was expansionary and improved to 52.2.

Federal Reserve (Fed) members spoke remained cautious, Daly on cutting rates quickly risking inflation getting stuck, Bostic once more on easing likely appropriate this summer, Kugler “cautiously optimistic” of ongoing progress regarding “disinflation without significant deterioration of the labor market”, Williams again expecting rate cuts later this year, and Mester that the January PCE prints won’t “really change my view” regarding getting to the central bank’s inflation target but shows “there is a little more work for the Fed to do here”.

There was also the release of the Fed’s Monetary Policy Report, in it citing the banking system that “remains sound and resilient” overall but that “a few areas of risk warrant continued monitoring”.

Week ahead: Services PMIs, NFP, and the Fed’s Powell testifies

As for the week ahead, it’s a light start out of the US and picks up tomorrow with services PMIs where it’s been a story of expansionary readings be it out of S&P Global or healthier out of ISM, and noting not just the sector but its pricing component that experienced a surge last time around to 64 from 56.7 before that.

If we’re still talking about the data, expect the attention to shift towards the US labor market with ADP’s non-farm estimate and job openings out of JOLTS on Wednesday, Challenger’s job cuts and the weekly claims on Thursday, and leading up to the market-impacting Non-Farm Payrolls (NFP) on Friday. Expectations are we’ll see growth of around 190K for the month of February, and for the unemployment rate to hold at 3.7%, with added focus on any weakness under the hood after what has been divergence between the establishment and household surveys.

Plenty of central bank members speaking, but expect the attention to be on Chairman Powell’s testimony on Wednesday before the House Financial Services Committee, and if there’s anything to add when he testifies before the Senate Banking Committee the day after. On the political front, the government shutdown has been avoided, but the deadlines pushed out to just March 8 and 22 means nowhere near out of the woods even as congressional negotiators unveil a bill for funding the remainder of the fiscal year. There’s also ‘Super Tuesday’ and the State of the Union Address.

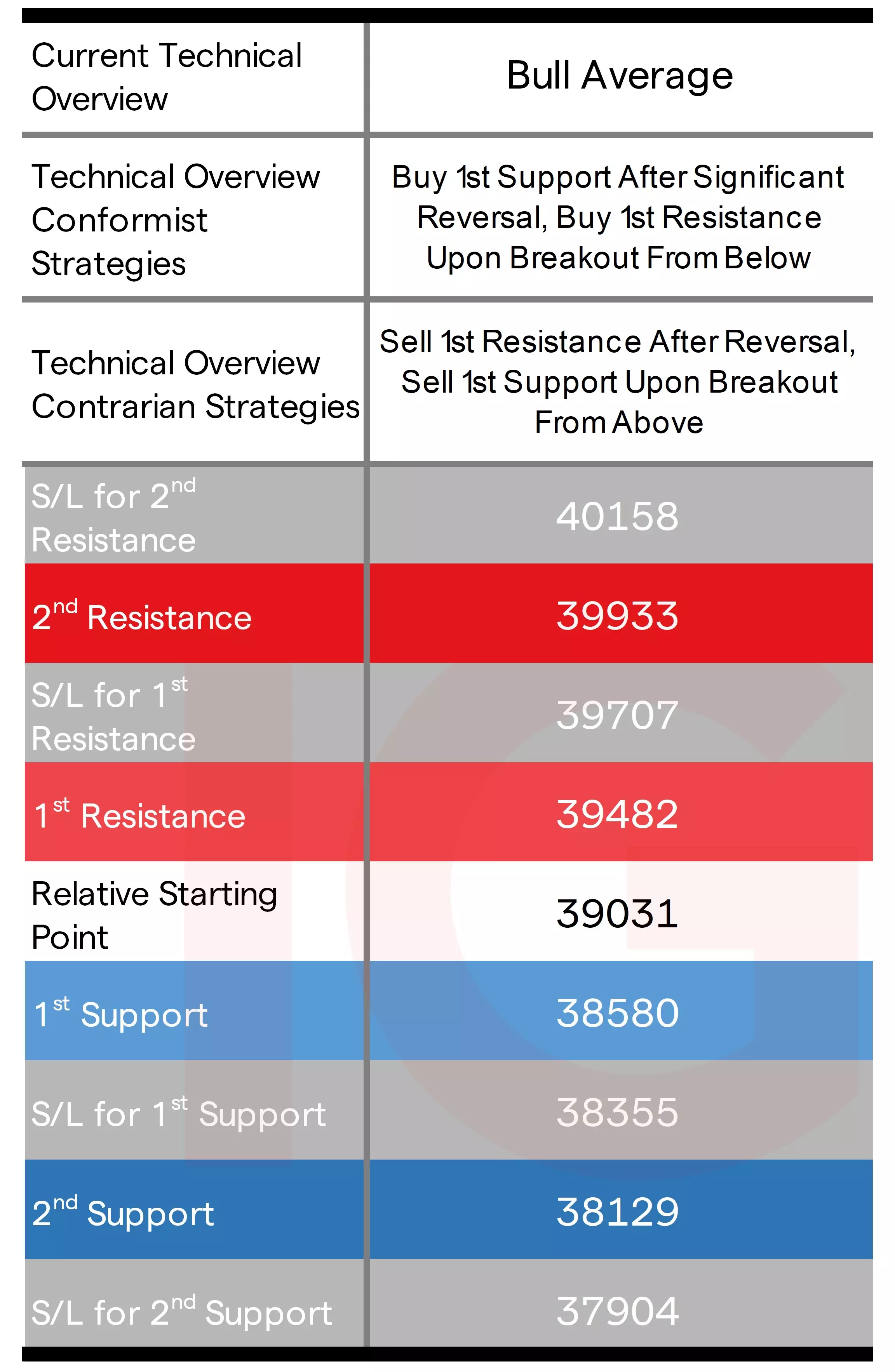

Dow technical analysis, overview, strategies, and levels

Lacking a record high meant there wasn't as much focus on this index compared to the S&P 500 and Nasdaq 100. On the weekly time frame, there was a lack of a play for both conformists and contrarians, as the intraweek lows were within its previous weekly 1st Support. As for the daily late last week, same story on Thursday. It needed Friday's gains to offer little for both conformist buy-breakouts and contrarian sell-after-reversals off the daily 1st Resistance, where it also has a 'bull average' technical overview matching the weekly, but where action within its channel can tilt the narrative more easily in the shorter term.

Source: IG

Source: IG

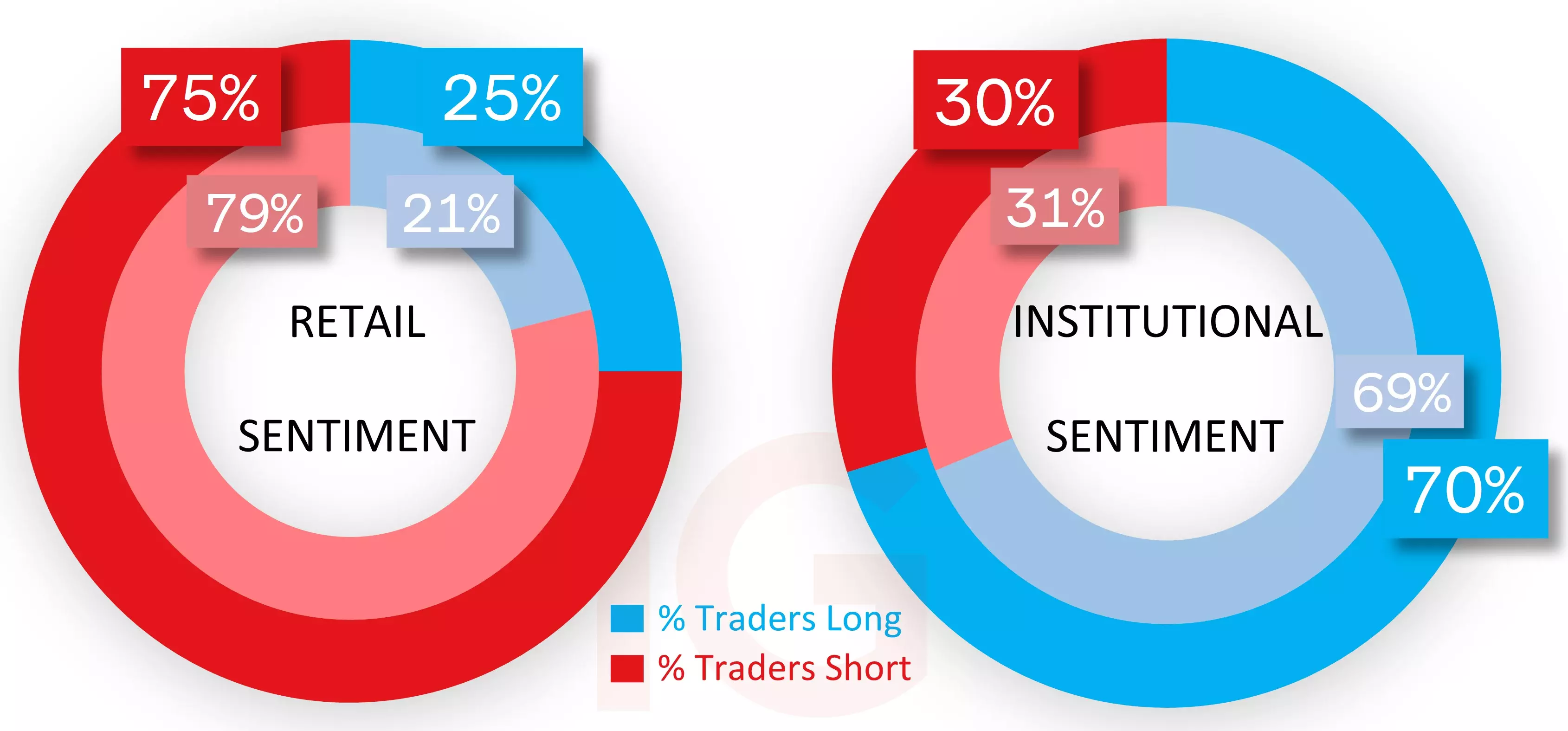

IG client* and CoT** sentiment for the Dow

CoT speculators are heavy buy and up a notch to 70% (longs +542 lots, shorts -838), yet to reverse the pullback a couple weeks ago, and in all still cautious about upping their long bias significantly further at this stage. IG clients continue to look for a chance to unwind what was extreme sell bias amongst them at the start of last week, the Dow's pullback providing partial relief.

Source: IG

Source: IG

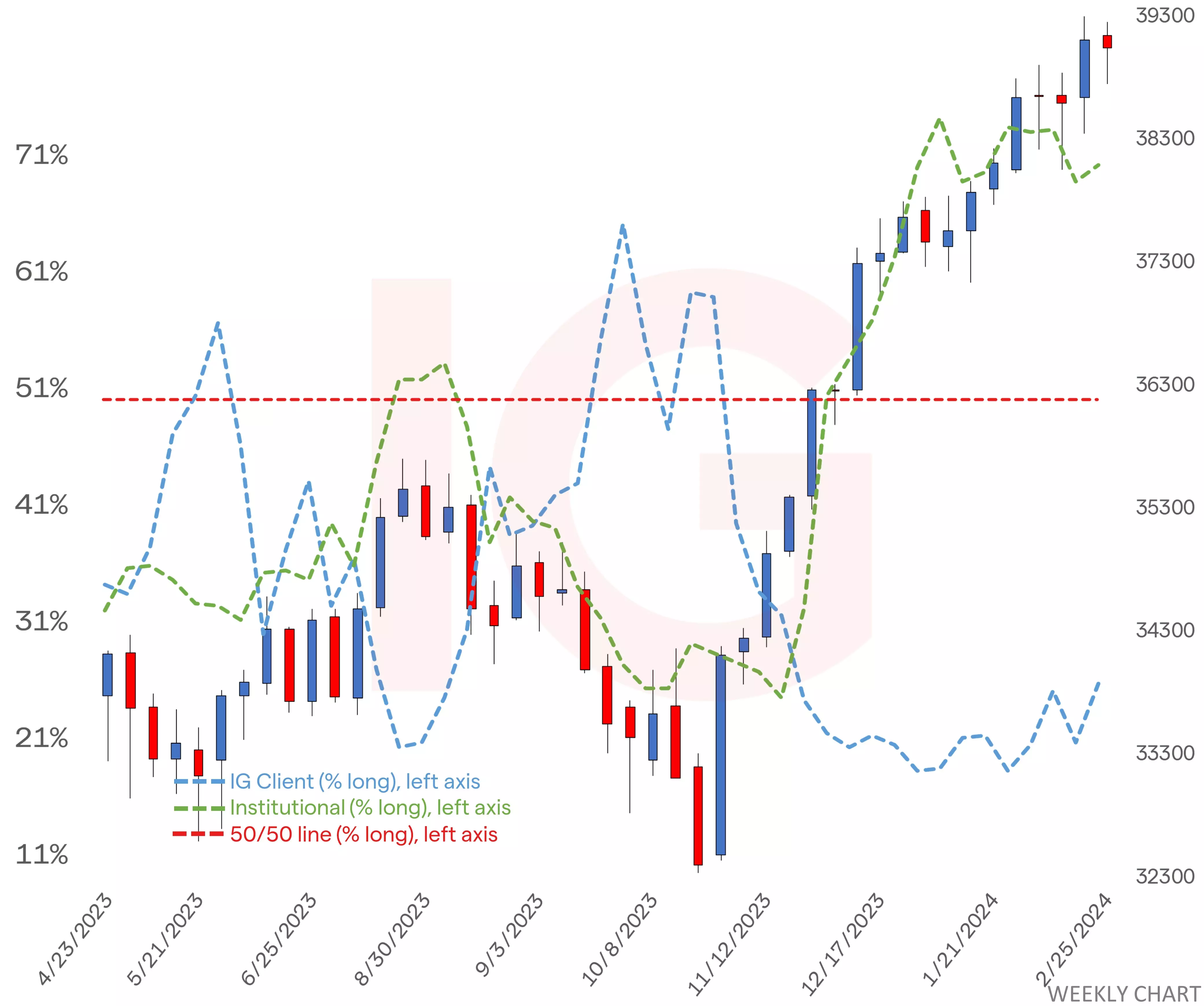

Dow chart with retail and institutional sentiment

Source: IG

Source: IG

- *The percentage of IG client accounts with positions in this market that are currently long or short. Calculated to the nearest 1%, as of the start of this week for the outer circle. Inner circle is from the start of last week.

- **CoT sentiment taken from the CFTC’s Commitment of Traders report, outer circle is latest report released on Friday with the positions as of last Tuesday, inner circle from the report prior.

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now