Dow 30: futures little changed after a record close

Entry posted by MongiIG in Market News

302 views

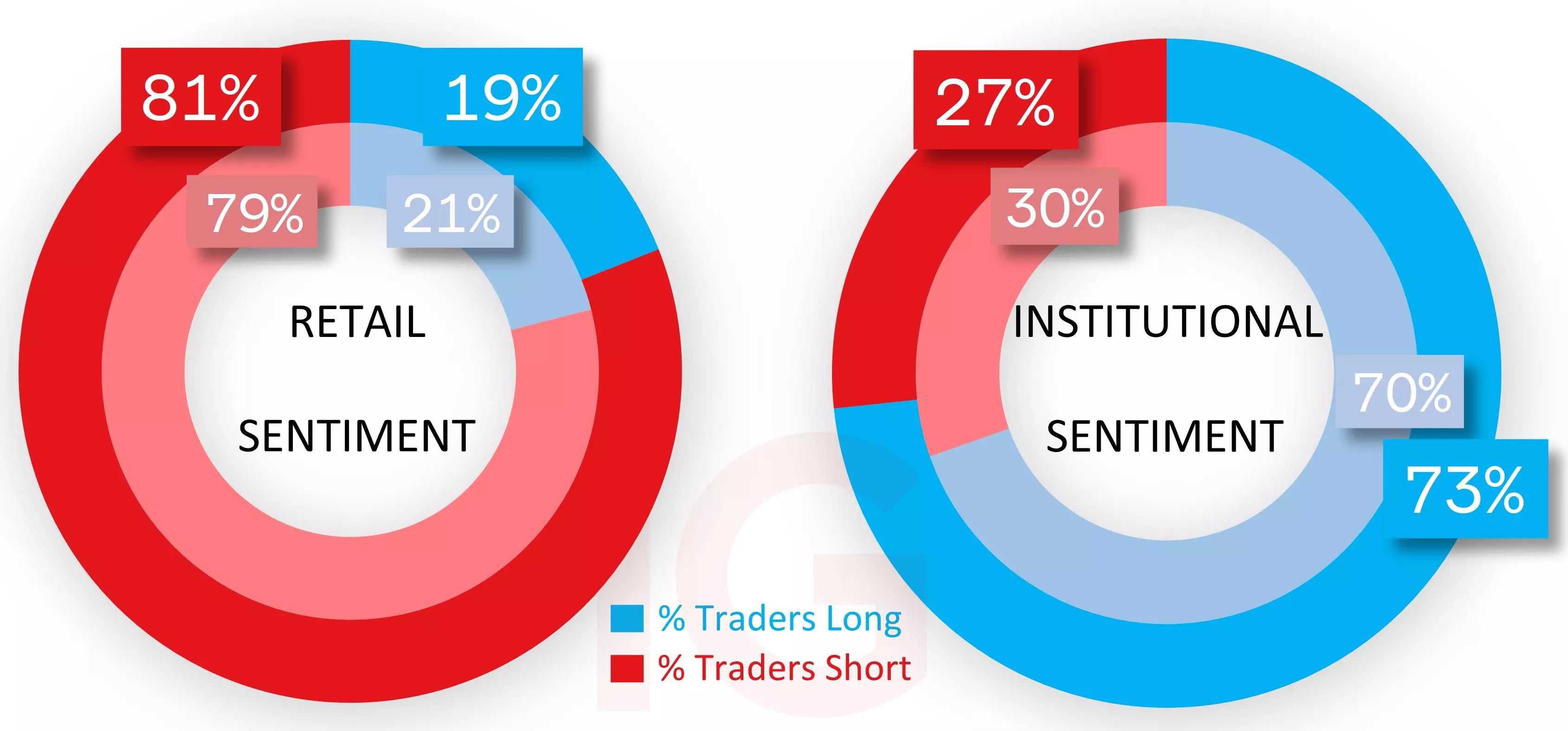

Technical overview remains bullish, and in sentiment CoT speculators upping their heavy buy bias.

Source: Bloomberg

Source: Bloomberg

Strong headline labor data

Plenty to digest last Friday out of the US: (1) Non-Farm Payrolls (NFP) for the month of January showed growth of 353K, smashing the roughly 180K estimates with higher revisions for the two months that preceded it; (2) the unemployment rate held at 3.7% instead of rising, but household survey divergence again as it showed a drop of 31K, and the U6 was a notch higher at 7.2%; (3) the labor force participation rate held at 62.5%; (4) the employment-population ratio was a notch higher at 60.2%; and (5) wage growth month-on-month (m/m) was a much hotter 0.6%, taking it higher year-on-year (y/y) to 4.5%, but came with weakness in overall hours worked.

UoM's figures generally improved, and the reaction to Big Tech’s earnings was net positive

There were also revised figures out of UoM (University of Michigan), with consumer sentiment improving to 79 and, more importantly, their inflation expectations holding for the 12-month at 2.9%, even if a notch higher for the five-year to the same level. And more from Big Tech in terms of earnings last Thursday: (1) Apple’s figures beat but sales in China were disappointing, and potentially weaker iPhone sales this quarter resulted in its share price declining; (2) Amazon saw decent gains after its earnings and revenue beat, which came with strong guidance for the current quarter; and (3) Meta was the clear outperformer, with its share price closing over 20% higher after managing to beat estimates, announcing a $50bn share buyback program, and its first-ever dividend payment.

Key stock indices enjoyed another positive weekly finish, while over in the bond market, we saw mixed performance for Treasury yields that finished lower on the further end (even after Friday’s jump) while the more policy-sensitive closed higher, and market pricing (CME’s FedWatch) with far more clarity on a hold this March.

Week ahead: Services PMIs, auctions, Fed member speak, and more earnings

As for the week ahead, it’s a relatively quiet one when looking at the data, and where it’ll be busier for some early on. We’ll get services PMIs (Purchasing Managers’ Index) later today out of the US from both S&P Global and ISM (Institute for Supply Management), both expected to remain in expansionary territory. There’s also the Federal Reserve’s (Fed) loan officer survey for the fourth quarter of last year to see how bank lending and conditions have been faring. A few auctions over the next three days with the 3-year tomorrow, 10-year on Wednesday, and 30-year on Thursday, and Fed member speak on all three days, earlier its chairman Powell in an interview on reducing “interest rates carefully” with a strong economy. We’ve got the weekly items like inventory data, mortgage applications, and claims, but that aside and on the earnings front in the US, there are a few notable ones including McDonald’s today, Eli Lilly and Uber tomorrow, Disney on Wednesday, ConocoPhillips on Thursday, and PepsiCo on Friday.

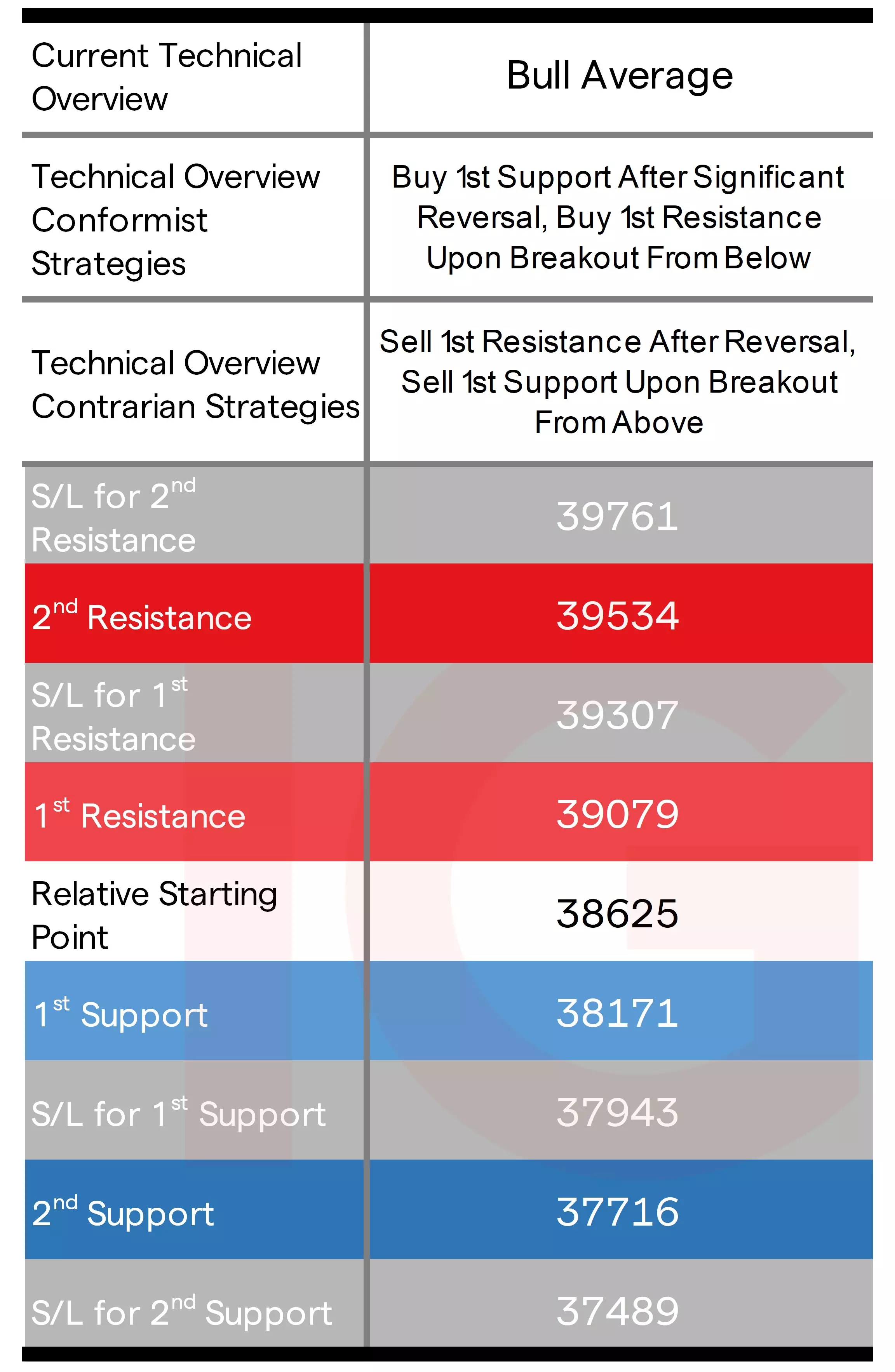

Dow technical analysis, overview, strategies, and levels

Its previous weekly 1st resistance level might have initially held, favoring contrarian sell-after-reversals, but the moves after going past it and stopping them out give conformist buy-breakouts the eventual win. The higher close keeps key technical indicators green, and so too does its overview as bullish in both weekly and daily time frames.

Source: IG

Source: IG

IG client* and CoT** sentiment for the Dow

IG clients remain in extreme sell territory and have raised that bias to start the week off at 81%. Although is lower than the more extreme levels seen prior, there will likely be further caution on shorts getting in until a more pronounced pullback in price is witnessed. CoT speculators are an opposite majority buy and have raised their heavy long bias again, this time to 73% (longs 6,790 lots, shorts 21), momentum likely raising it while shorts generally holding.

Source: IG

Source: IG

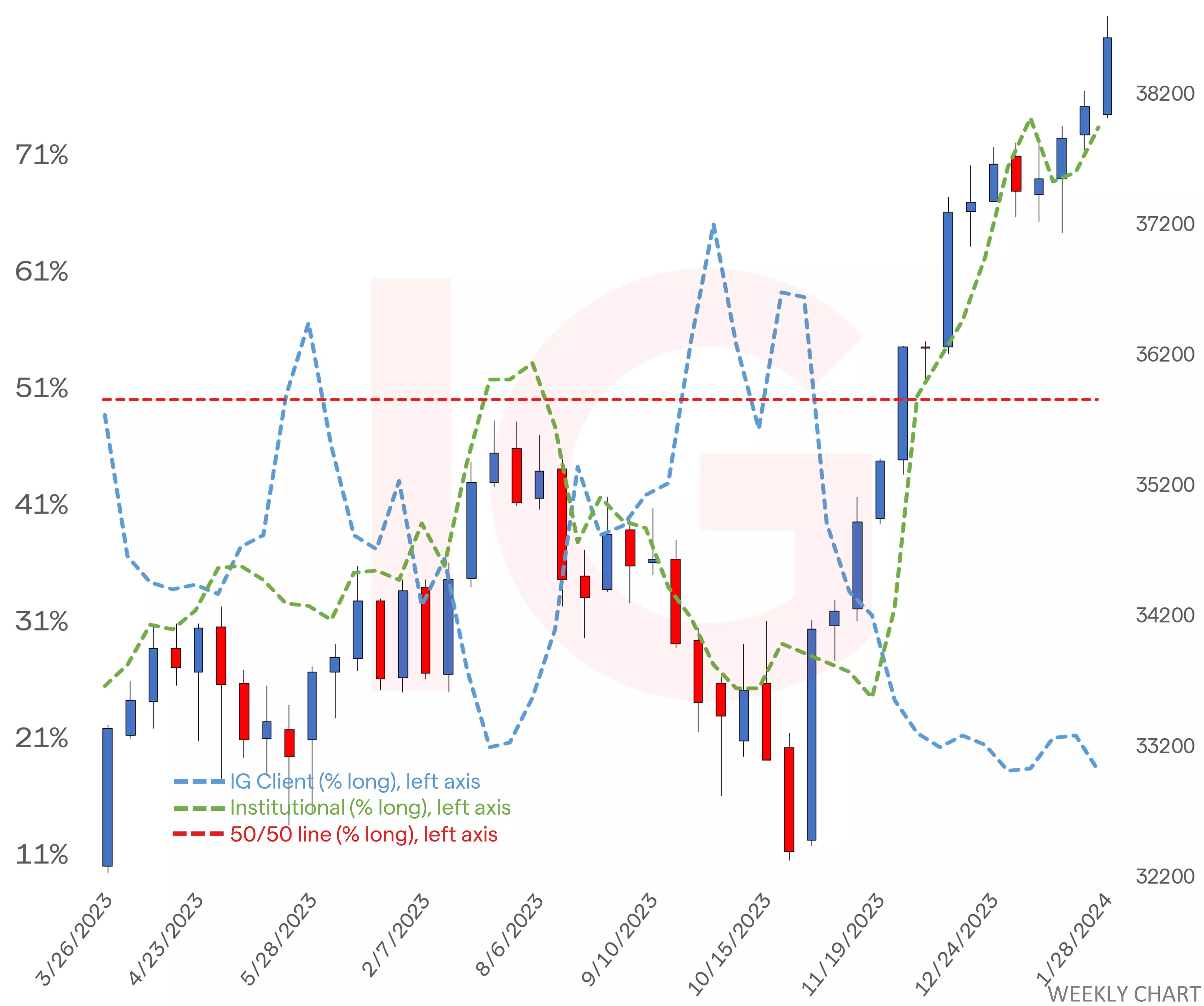

Dow chart with retail and institutional sentiment

Source: IG

Source: IG

- *The percentage of IG client accounts with positions in this market that are currently long or short. Calculated to the nearest 1%, as of the start of this week for the outer circle. Inner circle is from the start of last week.

- **CoT sentiment taken from the CFTC’s Commitment of Traders report, outer circle is latest report released on Friday with the positions as of last Tuesday, inner circle from the report prior.

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now