Tesla's Q1 2024 earnings: navigating price cuts and Chinese competition

Entry posted by MongiIG in Market News

270 views

Discover what to expect from Tesla's Q1 2024 earnings report, including production and delivery figures, competition, and new product updates. Explore what is influencing Tesla's performance and its strategies for growth.

When will Tesla report its latest earnings?

Both Tesla traders and investors nervously await Tuesday, 23 April, after market close, as that’s when they’ll be releasing their first-quarter results.

Tesla share price: forecasts from Q1 results

Traders and investors will all be hoping it can put an end to what have been successive misses in matching estimates. Tesla's share price has yet to undo losses suffered back in January when both earnings and revenue for the final quarter of last year came in below expectations. It's well beneath what it was valued at back in October when it suffered an earnings and revenue miss for the third quarter of 2023.

Tesla's latest manufacturing and delivery insights

Looking at the most recent quarter and breaking down the deliveries and production, the figures certainly disappointed and came in well below estimates that were already reduced prior. It suffered its first annual decline when it came to deliveries, at only 386,810, down 8.5% from the same period last year. Production was also lower, at 433,371, with the gap between it and deliveries widening, certainly hurting the demand narrative.

Q1 challenges: Berlin gigafactory sabotage and the competitive landscape

The belief that 'supply can create its own demand' when it comes to Tesla continues to disintegrate, or perhaps it’s the matter of the remaining market where clients are more conscious of costs that are eying the price range of its products more so than what those models entail. And it matters far more for a growth stock and a company still valued as such. We already got the warning prior regarding growth that may be "notably lower" this year compared to last year's rate of growth, and there will need to be confirmation it indeed is "between two major growth waves".

A few items took the attention when it came to the first quarter of this year including the power sabotage at its gigafactory in Berlin that impacted production there in March, but it’s really been about what the competition has been up to. Fisker might be on the way out, legacy automakers that were trying to get in on the electric vehicle (EV) action are struggling with higher costs and lower demand shifting to hybrids instead, and the biggest relief was probably that heavyweight Apple dropped its EV project. But the latter was always meant to target the premium segment, and it’s the lower segments that are becoming Tesla’s problem.

Source: Bloomberg

Source: Bloomberg

Tesla vs China: the ongoing competition

There have been ongoing price cuts from the likes of BYD as well as new model trims that carry with it lower prices as it seeks to capture a larger share of not just the EV market but from established players as well. Its latest figures for the fourth quarter of last year showed revenue climbing to a record high but net profit failing to best Q3 figures. Tesla is planning to launch its first electric pickup truck this year and there are still those looking to get in on the EV action with Xiaomi the most recent with its SU7 that is priced well beneath Tesla’s Model 3. Elsewhere, Huawei and Chery’s Luxeed S7 electric sedan finally started mass delivery.

Tesla's response: aggressive price cuts and FSD promotion

To keep up, Tesla has had to dig deep once more. Prices of all four key models (3, S, X, and Y) are down an average of about 15% for the first quarter of this year (cargurus.com) with the cuts largest for the 3 and Y while smallest for the X (and doesn’t include the discounts at the start of this quarter). The latest push was an announcement near the end of the quarter. Tesla will offer a free trial of its Full Self-Driving (FSD) for a month to US customers that have the capability. This is with the hopes it’ll entice those purchasing a Tesla into paying an additional $12,000 for the driver-assist technology. It aims to reverse what has been a decline of those buying the package but whether that software update will translate to better figures for the quarter we’re currently in remains yet to be seen.

Key points investors continue to watch

- Newer models: attention is on the mass-market sub-$30K EV expected to enter production in the second half of 2025. This model aims to compete with BYD and its lower-cost models, especially after recent attention from a Reuters report claiming Tesla was cancelling it. Musk's response was that “Reuters is lying (again).”

- The latest roadster version: Musk has indicated plans for unveiling the latest Roadster at the end of this year, with shipping slated for next year

- Charging business: Tesla's charging network has gone from strength to strength, notably opening up to Ford EVs at the end of February

- Optimus: there's increased optimism around its potential following positive early feedback

- Chinese competition: Musk's comments from the last earnings call suggested Tesla could “pretty much demolish” the competition in the absence of trade barriers

- Cybertruck progress: after its first full quarter of deliveries, ramping up production to around a quarter-million units is a challenge due to its “manufacturing complexity.”

- Potential catalysts: updates that could shift the narrative and act as a catalyst to draw investors back with more confidence, including any hints about the upcoming 8 August robotaxi unveiling.

Source: Bloomberg

Source: Bloomberg

Tesla's Q1 EPS and revenue forecasts

In all, expectations for Tesla's first quarter are that we'll get an earnings per share (EPS) reading of just $0.54, a figure that's lower both quarter-on-quarter (q/q) as well as year-on-year (y/y), and revised notably lower compared to a few months back. Revenue should also come in lower for both periods, at $22.75 billion, and here too, estimates have been revised lower.

Margins are expected to continue struggling in the current phase. As it tackles the lower end of the market from here on out, intense competition from all sides only means that figure will remain tested. Its gross profit margins are expected to drop but remain above 17%. Their reliance on rates falling – given higher interest rates translate into costlier financing to purchase a Tesla – means they’ll have to wait until at least September. This is according to market pricing of when the US Federal Reserve will cut rates on the front (CME’s FedWatch) following hotter US CPI (Consumer Price Index) readings

Where do analysts stand on Tesla?

As for analyst recommendations, there are five in the ‘strong buy’ category, 11 ‘buy’, a larger 22 for a ‘hold’, seven for ‘sell’ and four still favoring a ‘strong sell’, with the average price target among them lowered to $186.88 that's above its share price but in comparison to recent figures, not too far off (source: LSEG).

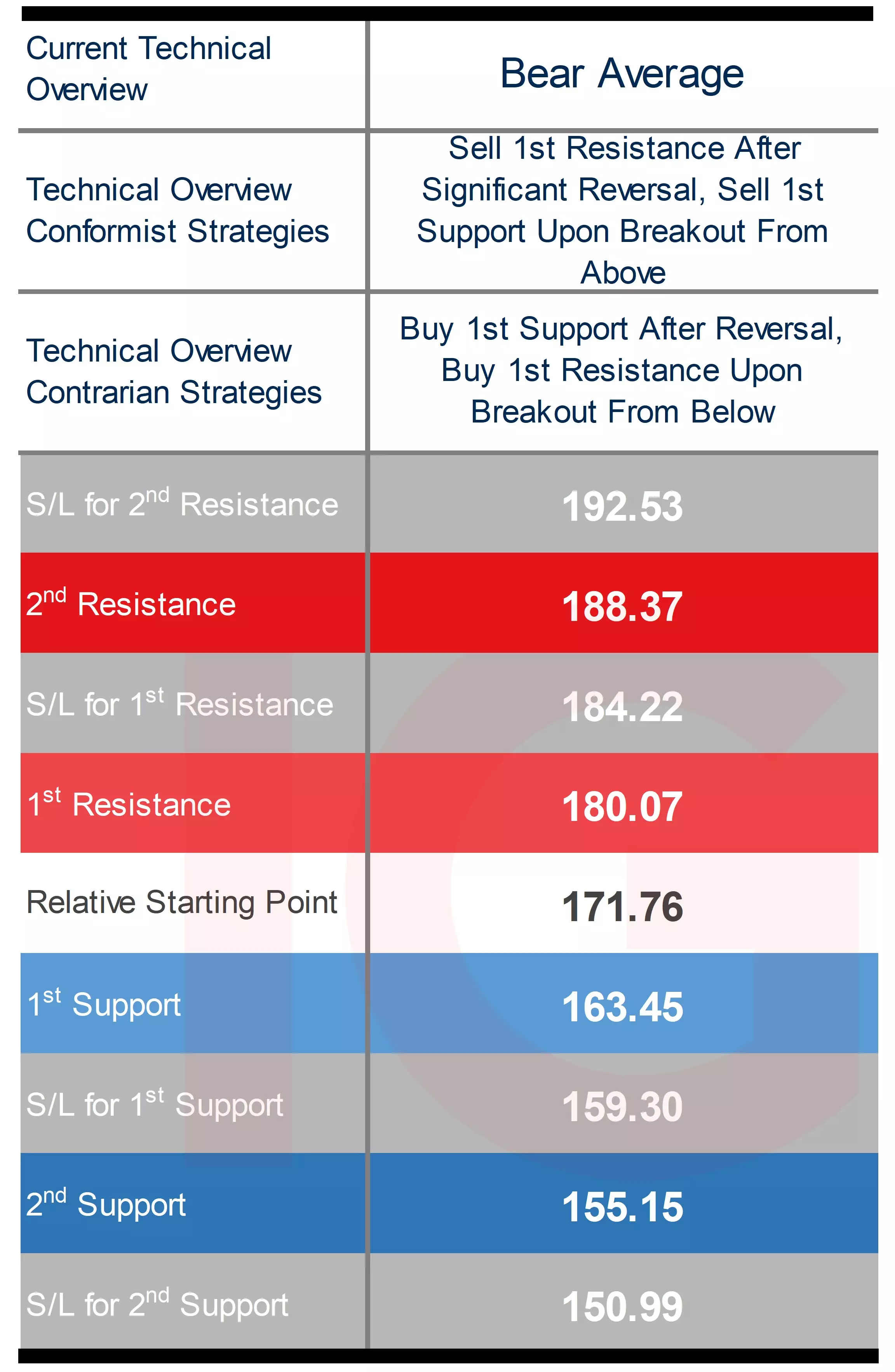

Trading Tesla’s Q1 results: weekly technical overview and trading strategies

Tesla's share price is well above the lows seen at the start of last year, but that's about all we can get in terms of good news on the technical front. We're working within two bear channels (see chart below), the narrower one still holding while price has failed to breach the upper end of the larger one.

Looking at its key technical indicators, and the price is still beneath all its main long-term weekly moving averages (50, 100, 200), working off the lower end of the weekly band. On the DMI (Directional Movement Index) front, the -DI remains above the +DI by a decent margin, and an ADX (Average Directional Movement Index) is reaching trending territory.

That has led to a technical overview that's 'bear average', though keep in mind that on average, we've still been experiencing relatively controlled intraweek moves. There's the obvious matter that the earnings release is a fundamental event where technicals are shelved, especially when it involves a surprise, and means technical levels will likely struggle or even fail to hold once the latest figures are released.

Source: IG

Source: IG

Tesla weekly chart with key technical indicators

Source: IG

Source: IG

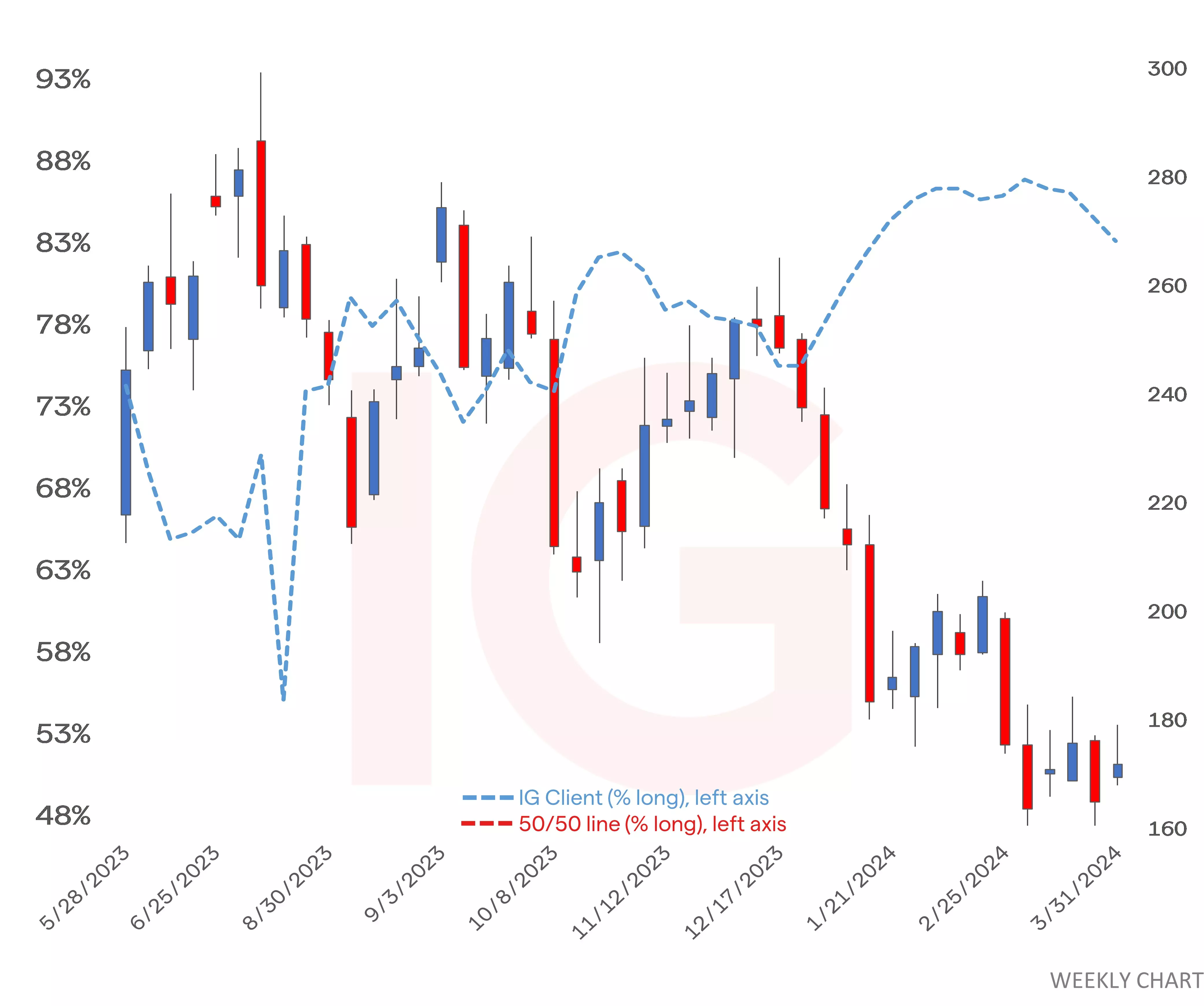

Tesla weekly chart with IG client sentiment

Source: IG

Source: IG

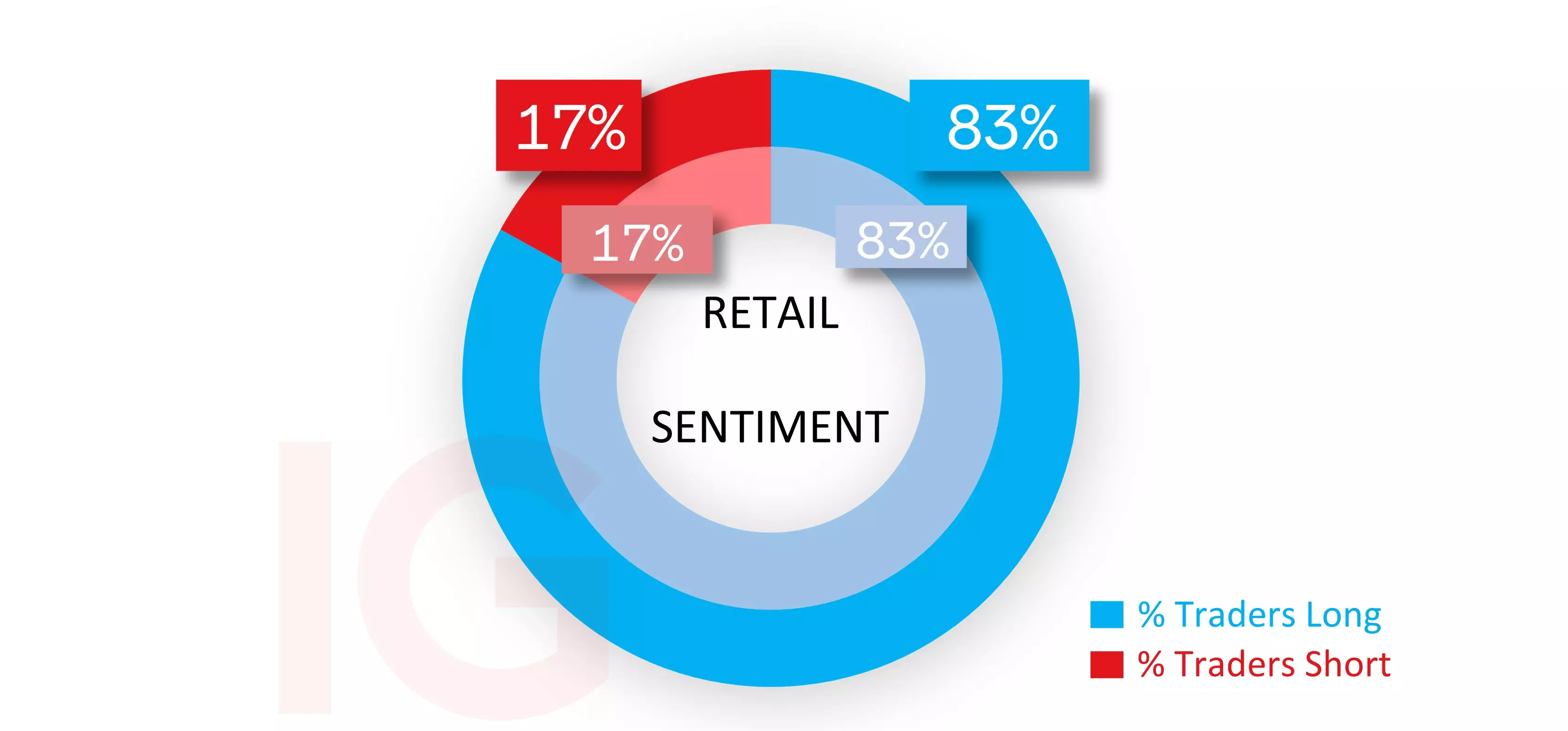

IG client sentiment* and short interest for Tesla shares

Among IG clients, the sentiment has consistently shown an extreme buy bias for the past three months. This followed a period where it oscillated between this extreme buy bias and a heavy long position. The latest figure stands at 83% as of Thursday morning, remaining unchanged from yesterday (image below).

Short interest in Tesla shares has seen an increase over the last three months, moving from 86 million shares, which represented 2.73% of the total in January during our previous earnings preview, to over 107 million shares. These now account for 3.37% of the total (source: LSEG).

Source: IG

Source: IG

- *The percentage of IG client accounts with positions in this market that are currently long or short. Calculated to the nearest 1%, as of today morning 8am for the outer circle. Inner circle is from the previous trading day.

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now