ECB meeting preview: 75bp hike expected, but how high is high enough?

Entry posted by MongiIG in Market News

337 views

The ECB look likely to implement a 75bp rate hike, with traders looking out for clues over where policy and economic data goes from here

Source: Bloomberg

Source: Bloomberg

ECB meeting: the basics

The forthcoming European Central Bank (ECB) meeting will take place on Thursday 27 October 2022. The initial monetary policy decision will be announced at 1.15pm BST, with the press conference getting underway at 1.45pm.

What are the current issues faced by the ECB?

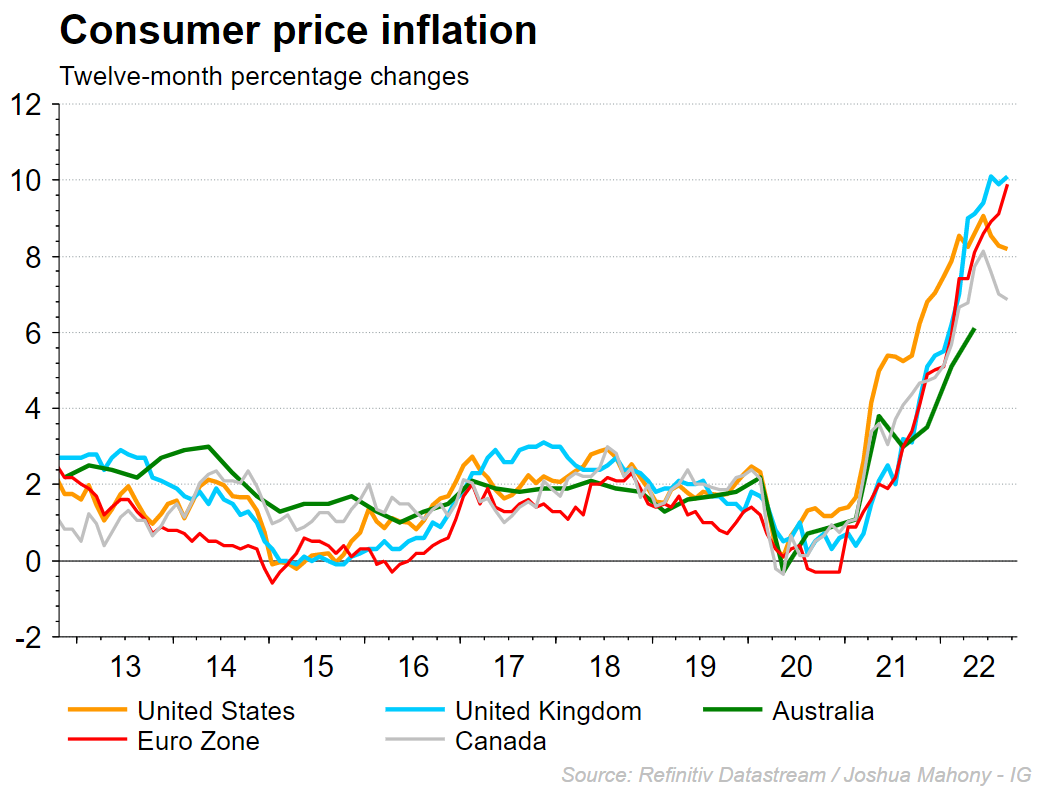

Inflation continues to be the dominant concern for Christine Lagarde and the ECB, with latest headline CPI figure standing at of 9.9%. While energy prices have drifted lower over recent months, we are seeing a sharp focus on the underlying price growth that has brought a record high core inflation reading of 4.8%. With inflation representing the primary mandate for the ECB, it is notable that they look likely to remain steadfast in their drive to tighten policy despite the negative economic implications that are likely to come as a result. However, the difficult task they are faced with is the challenge of driving down inflation without causing widespread damage to the eurozone economy. For the most part that means raising interest rates to a specific ‘terminal rate’ and maintaining them at that level until the heat is taken out of the economy. The hope is that they strike upon a terminal rate which is “neutral.” Neither stimulative nor anti-growth. However, there is a strong chance that this tightening phase overshoots to bring a number of economic repercussions, which could include a house price collapse, rising unemployment, economic contraction, and demand destruction for businesses. The chart below highlights how the eurozone and UK have continued to see inflation drive higher despite recent dips elsewhere in the world.

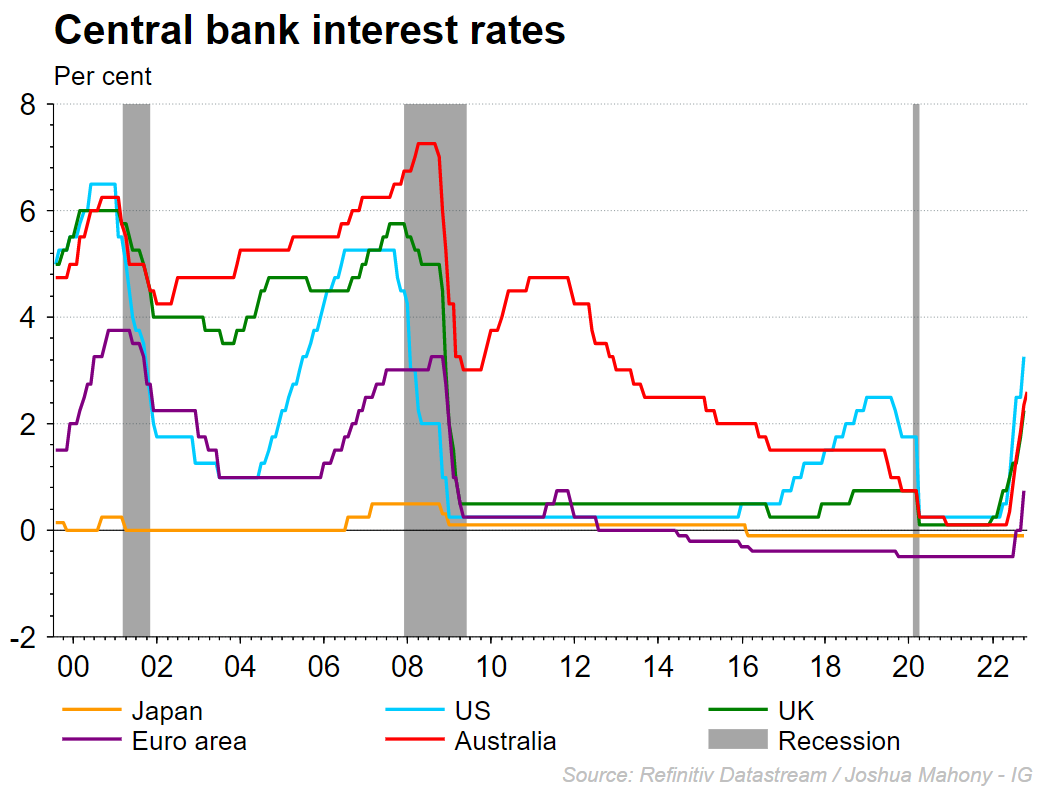

2022 has been a year that has been heavily driven by interest rate differentials, with the actions taken by central banks driving significant changes to market pricing for different assets. The recent decision from the RBA in Australia to hike by a mere 25-basis points produced a significant decline in the Australian dollar against many of the other major currencies. While their view that the FOMC rate hikes will do much of the heavy lifting when it comes to inflation, the ECB look unlikely given their relatively elevated inflation and lower rates. With eurozone inflation significantly above those further afield, markets expect to see a continued drive to push rates higher. It is worth noting that any early move to slow the pace of monetary tightening would also drive EUR/USD weakness, bringing higher imported inflation as a result.

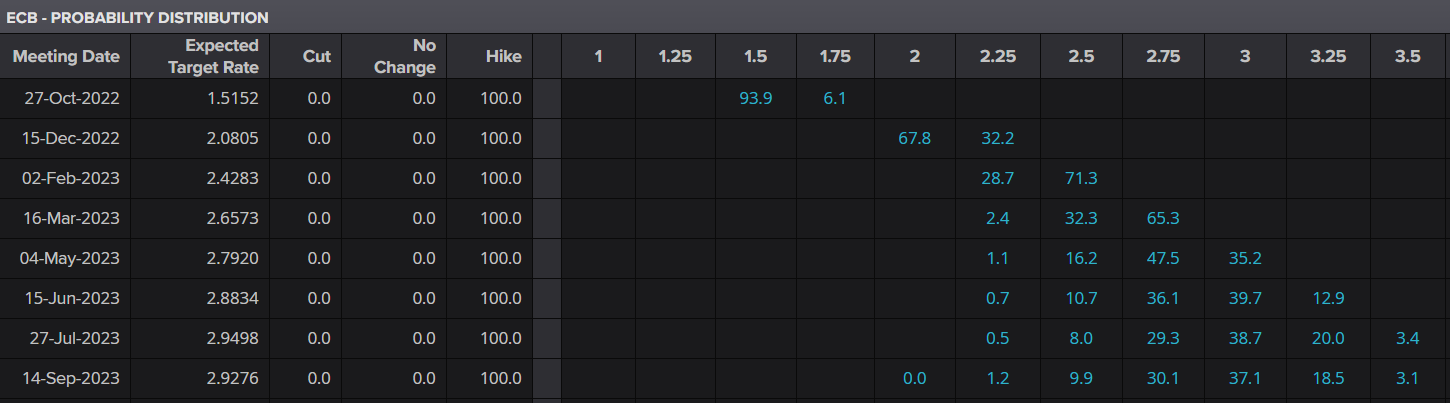

Markets are pricing in a 94% chance of a 75-basis point hike this Thursday, which would take the deposit rate to 1.50% and repo rate to 2.00%. The remaining 6% accounts for a potential 100-basis point move that would close the gap on the likes of the FOMC and BoE. Ultimately, with markets largely pricing in a significant hike, the question is more about future actions than current. What will be the terminal rate? How fast will we get there? Will we see inflation and growth forecasts amended? What is the outlook for quantitative tightening? These elements are likely to provide potential areas of commentary that could move the dial for markets.

The chart below shows the current market expectations, with the deposit rate priced to hike unto the 3% region by Q2 2023.

Source: Eikon

Source: Eikon

EURUSD upside unlikely to last

EUR/USD has enjoyed a rare period of upside of late, with the pair rising back towards the parity mark. However, the dollar dominance looks unlikely to end quite yet, with the recent PMI surveys highlighting further economic weakness to come. The daily chart signals the potential for another bearish turn from here, with a descending trendline coming into play once again. That line has held over the course of 2022 thus far, with the nearest swing-high coinciding with that 1.000 handle. As such, near-term upside looks likely to be sold into, with a move through the likes of 1.000 and 1.0368 bringing about a possible bullish reversal.

Source: ProRealTime

Source: ProRealTime

DAX rally brings potential short opportunities

The DAX provides a similar outlook, with a long-term downtrend dominating this year thus far. That comes into focus once again here, with price having rallied into the 100-day SMA and 61.8% Fibonacci level. With a long-term trendline up ahead, it seems likely that we will soon turn lower to continue the bearish trend. This pessimistic outlook holds unless price rallies through the September swing-high of 1.3570.

Source: ProRealTime

Source: ProRealTime

.jpeg.98f0cfe51803b4af23bc6b06b29ba6ff.jpeg)

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now