Global markets September preview: Fed, China and inflation

Entry posted by MongiIG in Market News

581 views

Historically, September has been a relatively weaker month in the financial world. What are the key events and releases could potentially influence the global markets this September?

Source: Bloomberg

Source: Bloomberg

As August comes to a close, the financial world gears up for the final month of the third quarter. Historically, September has been a relatively weaker month in the financial world.

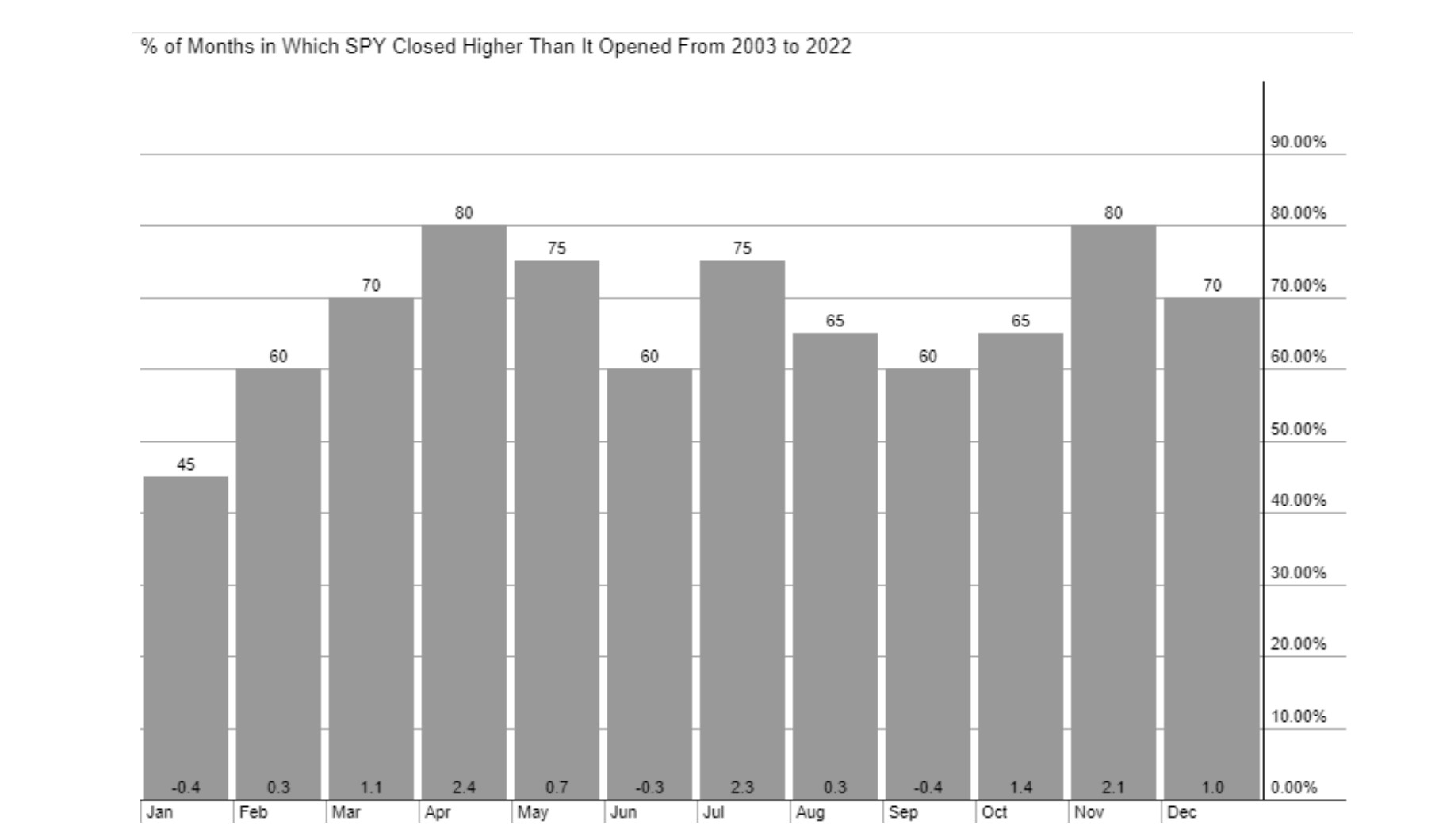

Over the past two decades, the probability of seeing the market move higher by the end of the month has been only 60% for September, the second lowest out of the 12 months. So, what are the key events and releases that could potentially stir the global markets this September?

September 1st to 10th

September 1st:US job report

The US job report for August will raise the curtain for September’s economic updates, including the Non-Farm Payrolls and the unemployment rate. Over the past two months, Non-Farm Payrolls have declined to the lowest levels of the year, and it's expected that August's figure will be around 180,000, marking the smallest increase in over 12 months. However, despite recent signs of a cooling in the job market, the unemployment rate is still projected to remain historically low at 3.5%. This suggests that there is still some way to go before the US labor market reaches a more balanced level, alleviating the Federal Reserve's concerns about rising service inflation.

September 5th:RBA meeting and Australia’s Q2 GDP

The Reserve Bank of Australia (RBA) is scheduled to hold its interest rate meeting on the first Tuesday of September. This meeting will be the final one under the leadership of the current RBA Governor, Philip Lowe. In both the July and August meetings, the Australian central bank kept its interest rates unchanged, and the market anticipates that the RBA will likely keep the current rate of 4.1% on hold in the September meeting.

At the same time, Australia’s GDP growth rate in the second quarter is anticipated to be a quarter-on-quarter increase of 0.2% and an annual rate of 1.5%. If these expectations materialize, it would signify the lowest level of economic growth in Australia since the fourth quarter of 2020.

September 9th:China’s deflation

China's Consumer Price Index officially dipped into deflation territory in July, and this trend is expected to persist as the August price index is projected to decline by 0.4% year-on-year. One of the most criticized factors contributing to China's lackluster economic recovery thus far is its insufficient domestic demand. The growing deflationary concerns are putting a serious damper on confidence in China's economic outlook.

September 11th to 19th

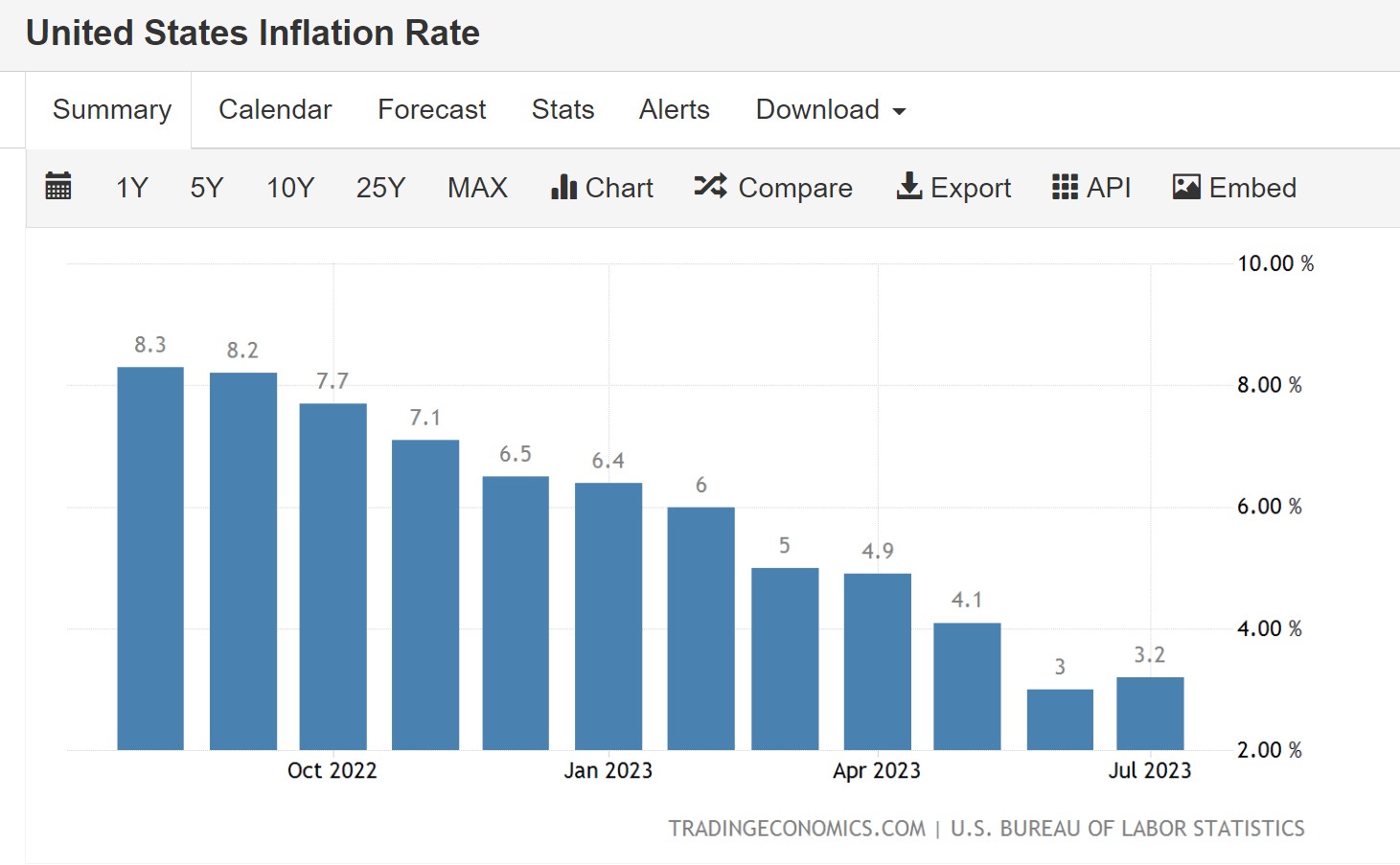

September 13/14th: US Inflation

This gauge of consumer and producer price data will be the final set of inflation indicators before the Federal Reserve's interest rate decision in the September FOMC meeting. At the time of writing, expectations suggest that the US consumer prices will rise by 0.3% compared to the previous month, with a year-on-year increase of 3.4%, and the core inflation rate at 4.6%.

Starting from July, due to base effects, the ongoing downtrend of the US’s primary inflation metric has come to an end, and it appears that the trajectory of inflation has reached an inflection point. Therefore, if this month's CPI figure exceeds expectations, it would not bode well for the Federal Reserve, signalling that inflation has entered a more sticky and challenging-to-control phase. Additionally, the Producer Price Index, which rebounded to its highest monthly increase since January 2023 last month, bakes more uncertainty into the future path of the inflation.

September 13th: ECB interest rate meeting

Currently, the market widely expects the European Central Bank to pause its rate hikes at the September meeting. In the August rate meeting, the European Central Bank raised rates by 25 basis points for the ninth consecutive time. Although inflation in the Eurozone has moderated somewhat, it still remains above the European Central Bank's 2% inflation target.

At Jackson Hole, the ECB Governor reaffirmed her dedication to the 2% inflation target, signaling that the European Central Bank's rate hike journey is yet to reach its conclusion. As such, if ECB decides to pause in September, it will be more likely to be a hawkish pause.

September 15th: China’s economic snapshot

On this day, China is set to unveil a slew of economic data, including housing prices, industrial production, fixed asset investment, unemployment rates, and retail sales. At present, it is anticipated that China's housing prices will continue their downward trajectory, while the unemployment rate is expected to climb to its highest level since February of this year, reaching 5.4%.

Over recent months, the majority of China's economic update have fallen short of market expectations. Concurrently, since the early days of this quarter, China has introduced a series of economic stimulus policies. Thus, these to-be-revelled economic indicators will play a pivotal role in assessing the effectiveness of these stimulus measures.

September 20th to 30th

This week is set to be the busiest period of September, with three major central banks scheduled to make updates to their monetary policies. The signals these central banks send following their meetings are poised to have a profound impact on global markets.

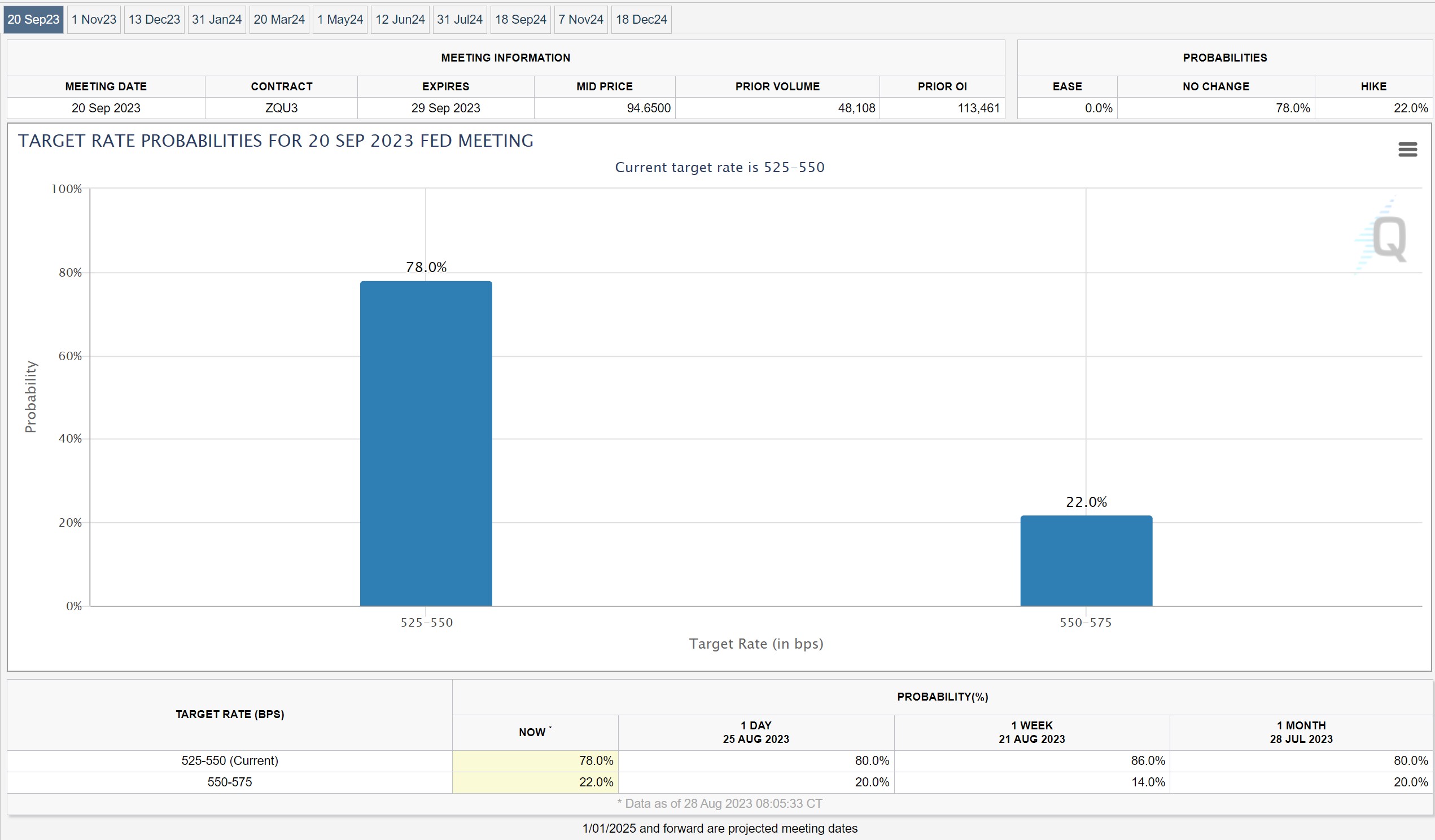

September 20th: FOMC meeting

After almost two months, the forthcoming FOMC meeting in September is garnering significant attention. Over the past weeks, the Federal Reserve has consistently emphasized its hawkish stance, including Powell's recent speech at Jackson Hole where he reiterated the commitment to keeping high-interest rates in place for longer to bring inflation back within the 2% target range.

As of the end of August, the market only perceived a 22% likelihood of a rate hike during the September meeting. Nevertheless, with more inflation and employment data coming in, it cannot be ruled out that market sentiment may shift as the Federal Reserve meeting approaches.

Source: CME

Source: CME

September 20th: BOE meeting

While there was a noticeable dip in UK inflation last month, it still remains remarkably high at 6.8%. Consequently, the Bank of England has a relatively long journey ahead in its tightening cycle.

During the August rate meeting, the Bank of England raised rates by 25 basis points, reaching 5.25%. This marked the 14th consecutive rate hike by the Bank of England and pushed UK interest rates to their highest point in 15 years. As we look ahead to the September rate meeting, the prevailing market expectation is that the Bank of England will continue hiking rates with another 25 basis points.

September 21th: BOJ meeting

Despite Japan grappling with persistently high inflation and a yen at decades-low levels, the Governor of the Bank of Japan recently reiterated that the Bank of Japan still views "underlying inflation" as remaining below the bank's target. Therefore, it wouldn't come as a surprise to the market if the BOJ's September meeting will continues to uphold its ultra-loose monetary policy.

However, the Bank of Japan did surprise the market in the previous meeting by stating that its 0.5% yield curve control ceiling should be regarded as a reference point rather than a strict limit. This was interpreted as an early signal of introducing more flexibility into its current monetary policy setting. As such, the key watch for the upcoming BOJ meeting is whether the BOJ will signal an exit from its contentious Yield Curve Control (YCC) .

2 Comments

Recommended Comments

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now