Wall Street: US equity indices Jolted by jobs data and House Speakers removal

Entry posted by MongiIG in Market News

580 views

Explore the key factors driving volatility, including a strong JOLTS report and hawkish Fed comments. Plus, get insights on the upcoming ISM Services PMI data and expert S&P 500 and Nasdaq technical analysis.

Source: Bloomberg

Source: Bloomberg

US equities in sharp decline

US equities experienced a sharp decline overnight as yields surged, following a red-hot JOLTS opening report that reinforced the message from the recent FOMC meeting regarding the need for higher rates over a longer period.

The JOLTS job openings for August surged to 9610k, a "mere" four standard deviations above the consensus median outcome of 8815k, with job openings returning to their highest level since May. Fed Chair Jerome Powell's favored metric of job openings per unemployed remained elevated at 1.52.

Hawkish Fed and high stakes

This week, hawkish Fed remarks, coupled with a stronger-than-expected ISM print and JOLTS job opening data, placed added significance on Friday night's Non-Farm Payroll report. However, before that, the market must assess the impact of the removal of House Speaker Kevin McCarthy, which raises the odds of a government shutdown when temporary funding expires on 17th November, along with the release of the ISM services PMI this evening.

We maintain the view that the interest rate market is too complacent about the possibility of one final rate hike before year-end, which is currently about 50% priced in (13 basis points) by year-end.

What to expect from ISM services PMI

Date: Thursday, October 5th at 1 am AEDT

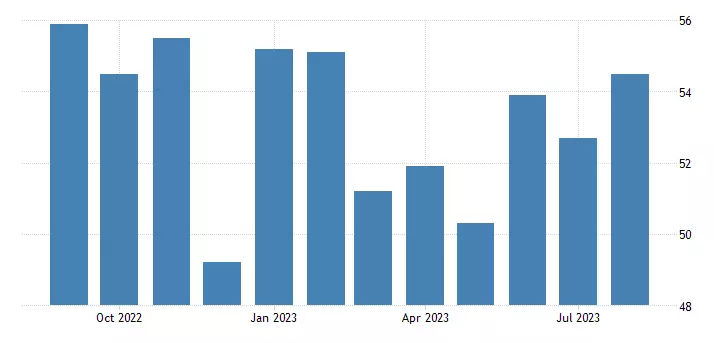

In August, the services PMI unexpectedly rose to 54.5 from 52.7 in July. It marked the fastest rate of growth in the services sector in six months, with robust increases in new orders (57.5 vs. 55), employment (54.7 vs. 50.7), and inventories (57.5 vs. 50.4).

For the month of September, the market anticipates the services PMI to ease to 53.5 from 54.5. If the services PMI does not cool as expected, it will further contribute to the reasons behind this week's yield surge and potentially undermine risk sentiment.

US ISM services PMI

Source: TradingEconomics

Source: TradingEconomics

S&P 500 technical analysis

Since early September, we have opined that the S&P 500 was missing another leg lower towards 4250/4000 as part of the correction that began in July.

The tentative signs of support noted within that range last week have been negated after the S&P 500 rejected resistance from the August 4335 low and broke below uptrend support at 4,250 from the October 3491 low.

If the S&P 500 now fails to hold above the 200-day moving average at 4,00 (on a closing basis), it negates the view that the pullback from the July high was corrective and warns of a potential impulsive Wave III decline towards 3900.

S&P 500 daily chart

Source: TradingView

Source: TradingView

Nasdaq technical analysis

Similar to the S&P 500 and in our previous reporting, we have suggested that the Nasdaq could experience another leg lower towards 14,200/14,000 as part of the correction that began in July.

The Wave C pullback from the early September high of 15,618 (as part of a three-wave Elliott Wave ABC correction) has yet to reach the ideal pullback zone and seems to be missing a final leg lower (minor Wave V).

If this pullback unfolds as expected, we anticipate a recovery that could push the Nasdaq to test and surpass the highs of July, possibly setting up a challenge to the 2021 bull market high of 16,764.

Nasdaq daily chart

Source: TradingView

Source: TradingView

- Source: TradingView - the figures stated are as of October 4th, 2023. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation.

This information has been prepared by IG, a trading name of IG Markets Limited. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients. See full non-independent research disclaimer and quarterly summary.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now