Microsoft’s Q1 earnings preview: Resilience expected to be the story

Entry posted by MongiIG in Market News

225 views

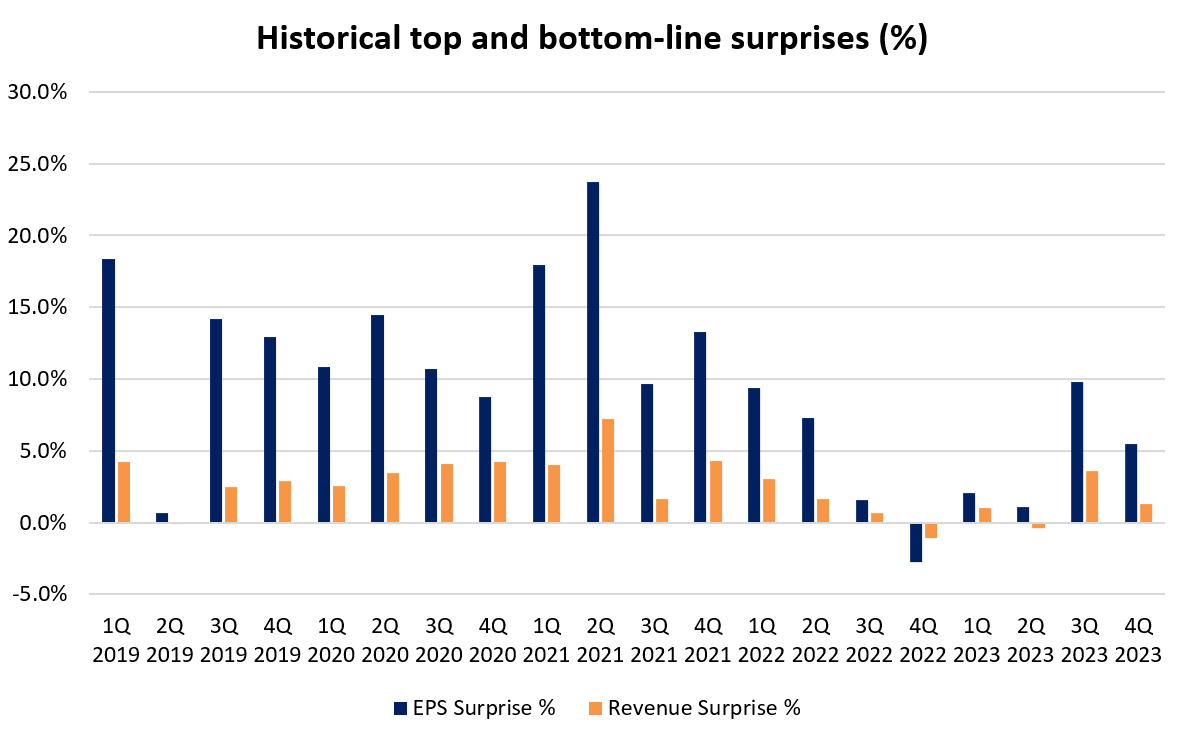

Broad consensus is for the upcoming results to reflect a continued recovery in both Microsoft’s top and bottom-line, in line with the trend over the past two quarters.

Source: Bloomberg

Source: Bloomberg

When does Microsoft Corp report earnings?

Microsoft Corp is set to release its quarter one (Q1) financial results on 24 October 2023, after market closes.

Microsoft’s earnings – what to expect

Broad consensus is for the upcoming results to reflect a continued recovery in both Microsoft’s top and bottom-line, in line with the trend over the past two quarters. Current expectations are for Microsoft’s Q1 2024 revenue to increase 8.7% from a year ago to US$54.48 billion.

Likewise, earnings per share (EPS) is expected to increase 12.8% year-on-year to US$2.65, up significantly from the US$2.35 in Q1 2023. Its earnings before interest, taxes, depreciation and amortization (EBITDA) margin is also expected to improve to 51.9% from the 48.5% a year ago.

Historically, Microsoft tends to have a strong track record of beating market expectations. It has beaten top-line estimates on 17 out of 20 previous occasions, while earnings have only fallen short of expectations once (4Q 2022) over the past 20 quarters.

Source: Refinitiv

Source: Refinitiv

Cloud segment on watch to reverse softening growth trend, along with hopes for stabilisation in PC market

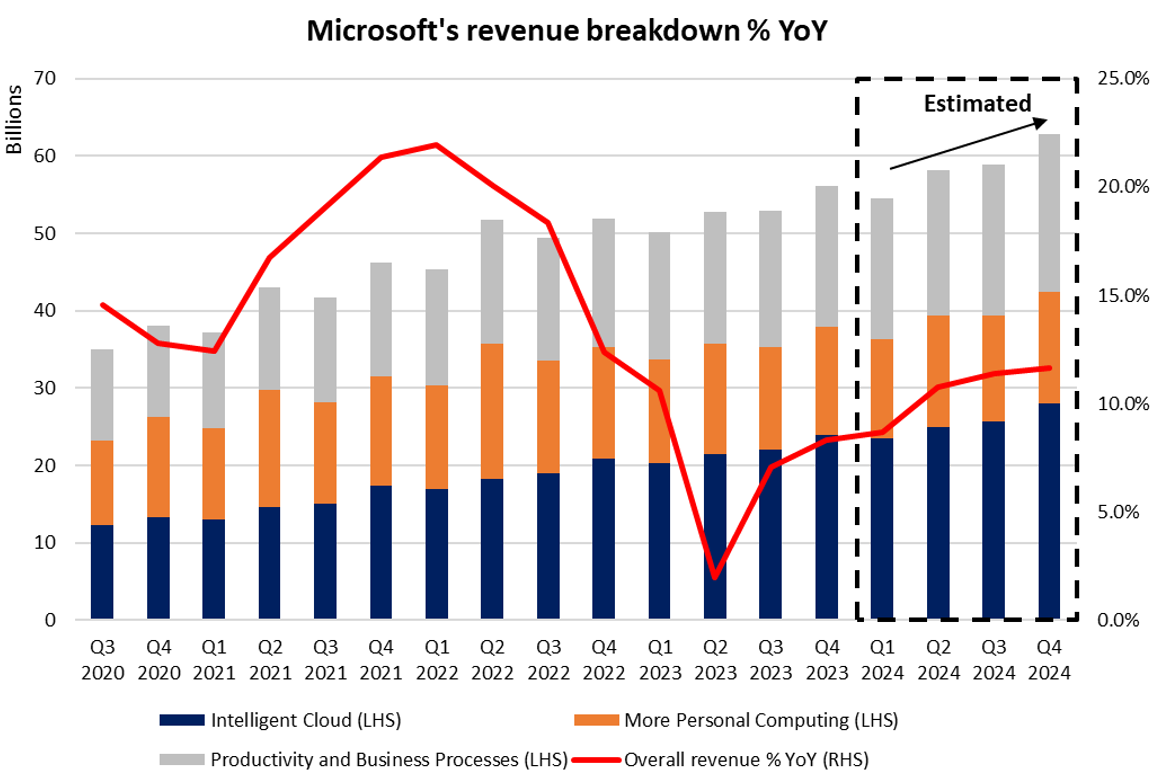

Year-on-year growth for Microsoft’s Intelligent Cloud segment has been witnessing a slowdown over the past five quarters, with momentum moderating from its initial >25% growth to 14.8% in the previous quarter. The segment has been the crown jewel for Microsoft’s businesses by being its highest-growth division and accounts for 43% of overall revenue.

That said, for the upcoming 1Q24 results, expectations are looking for a reversion to stronger growth (estimated 15.5% versus previous 14.8%) for the segment – its first since 3Q 2022. With that, any validation from the numbers may likely fuel optimism for the start of an improving growth trend ahead, while reflecting resilience in corporates’ digital transformation efforts despite uncertain economic conditions.

On the other hand, weak consumer demand for personal computers (PCs) may remain a weighing block for the recovery in its personal computing business, with the segment expected to turn in its fourth straight quarter of year-on-year contraction (estimated -3.7%). But with subdued expectations already in place, forward-looking statements may play a greater role in leading sentiments. The International Data Corporation (IDC) projects that global PC shipments may return to growth in 2024, which leaves any positive surprises on watch over coming quarters.

Source: Refinitiv

Source: Refinitiv

Forward-looking statements on vast growth catalysts to be in focus

Microsoft has recently received the green light for its US$69 billion acquisition of Activision Blizzard, which will significantly strengthen the company’s presence in the gaming industry. While any boost to its gaming revenue will not be reflected in the upcoming results, investors will be closely watching for any forward-looking guidance on the synergies with its Game Pass subscription service, in line with the company’s vision of focusing on player engagement over console sales.

Further, the company’s AI-driven product portfolio will be in focus as well, as the company leverages on its first-mover advantage in generative AI with a vast investment in OpenAI this year (US$10 billion). It is currently in the midst of rolling out its Microsoft 365 AI subscription service, Copilot, with more visibility on its adoption likely to be revealed over coming quarters. The huge user base of 345 million for its Microsoft 365 suite and dominance of its 365 products in the market (>50% market share for office productivity software) may offer vast room for monetisation, which could be a matter of time before the developments make its way into the company’s top and bottom-line.

Technical analysis – Share price setting its sight to overcome cloud resistance

A bullish divergence displayed on Moving Average Convergence/Divergence (MACD) on the daily chart has led to a more than 8% recovery in Microsoft’s share price since the start of the month, as buyers are now attempting to defend its 100-day moving average (MA). The broader upward trend may remain intact for now, with its weekly Relative Strength Index (RSI) successfully bouncing off the key 50 level over the past month – the midline that separates the bullish and bearish territories.

Coupled with an upward break of a near-term trendline resistance and MACD reverting back into positive territory, buyers seem to be in greater control for now. Its share price is now heading towards the upper edge of its Ichimoku cloud on the daily chart at the US$340.00 level, which may serve as immediate resistance to overcome. This level also coincides with its earlier September 2023 high, with any successful move above the cloud potentially leaving its all-time high at the US$366.01 on watch for a retest.

Source: IG charts

Source: IG charts

This information has been prepared by IG, a trading name of IG Markets Limited. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients. See full non-independent research disclaimer and quarterly summary.

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now