US jobs report preview: hiring difficulties could limit the size of any NFP rebound

Entry posted by ArvinIG in Analyst Article

399 views

Friday’s US jobs report unlikely to bring a sharp rebound, with businesses struggling to find the right people amid record high level of vacancies.

Source: Bloomberg

The September US jobs report is due to be released at 1.30pm, on Friday 8 October (UK time). Coming at a time where we are seeing huge volatility within financial markets, traders will be keeping a close eye on this latest jobs data to see if it maintains the economic recovery story or undermines it.

Coming at a time when businesses are worrying about supply chain and labour issues, there is an argument that businesses are struggling to hire as opposed to being unwilling to hire. Thus, with labour shortages and roaring demand, the question here is whether the US has workers that are skilled enough and in the right locations to take up the record number of vacancies currently on offer.

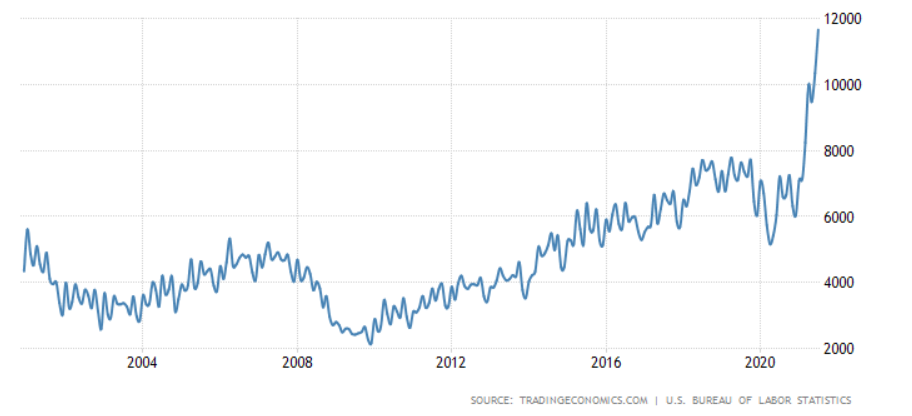

Source: Tradingeconomics.com

With that in mind, Friday’s jobs report provides us with a critical update on how businesses have been able to hire in the face of growing demand and ahead of a busy festive period. Will demand ultimately lead to a sharp rise in wages?

Non-farm Payrolls

Last month saw a somewhat worrying 235,000 Non-farm payroll's (NFP) figure, with a weak automatic data processing (ADP) and a sharp decline in the employment element of the manufacturing purhcasing managers index (PMI) providing a good clue that such a move was going to occur. That 235,000 figure represents the lowest reading we have seen in seven-months, and will leave markets questioning whether this is a short-term or longer lasting phenomenon. This month brings expectations of a 490,000 reading, which would still only take us up to roughly half the August reading.

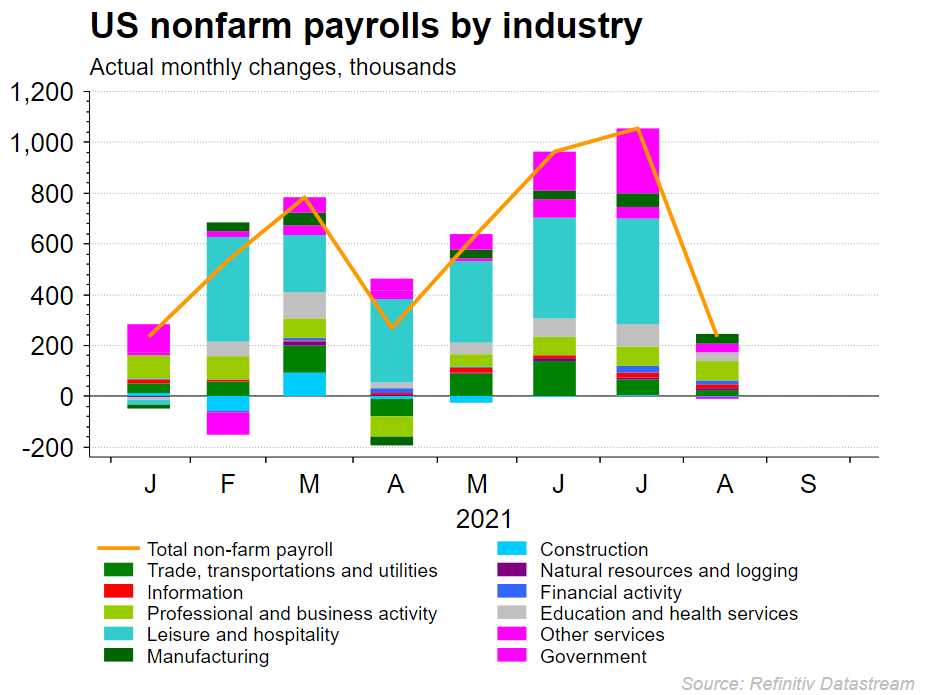

The chart below highlights how the weak August jobs figure involved a collapse in the crucial leisure and hospitality employment segment, with government hiring also falling off for the time being.

Source: Refinitiv Datastream

Unemployment

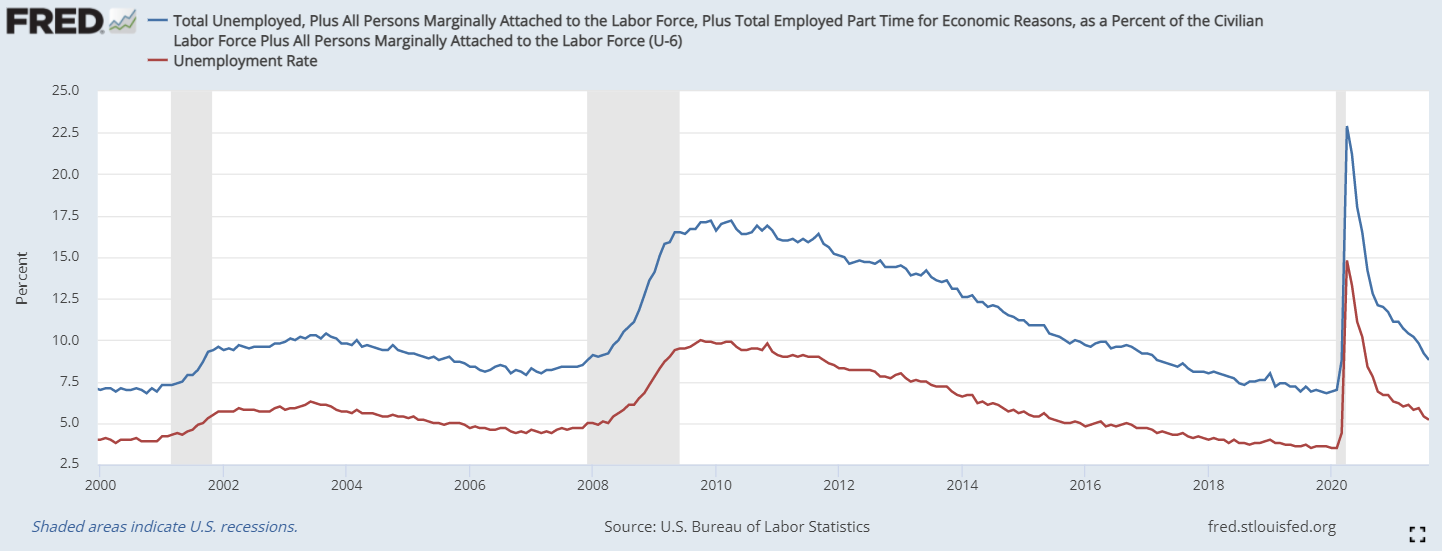

On the unemployment front, there is little reason to expect unemployment to rise. Instead, we are looking for unemployment to fall from 5.2% to 5.1%. Keep a close eye out for the latest participation rate, which will hopefully continue to fall as prospective workers come back into the jobs market.

The depressed nature of the participation rate means we should keep an eye on the wider U6 unemployment rate alongside the traditional U3 figure.

Source: Fred

Earnings

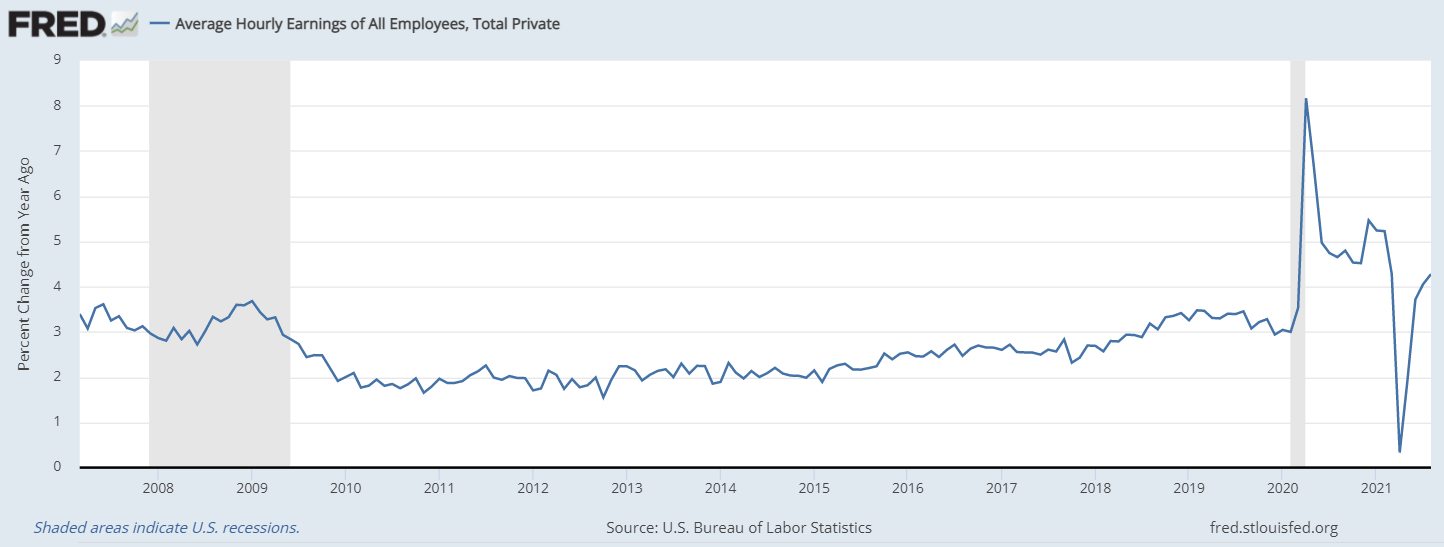

From an earnings perspective, the risk is that the growing hiring difficulties will spark a sharp rise in wages which in turn pushes up inflation. The market forecasts point towards a jump in earnings, with the September figure predicted at 4.7% following a reading on 4.3% in August.

The chart below highlights how such a figure would still be well below the 2020 readings that topped out at 8.1%. However, that rise was borne out of huge unemployment where Covid-19 restrictions adversely impacted low earners. Hence it is more significant to see 4.7% wage growth at times when unemployment is low than a huge spike in average wages driven by a sharp spike in joblessness. Yet again, such a consistent rise in business costs does provide a hinderance for future growth.

Source: Fred

What do other employment readings tell us?

One way to predict where Friday’s jobs report may move is to look at some of the alternate employment readings for gauge on the state of play.

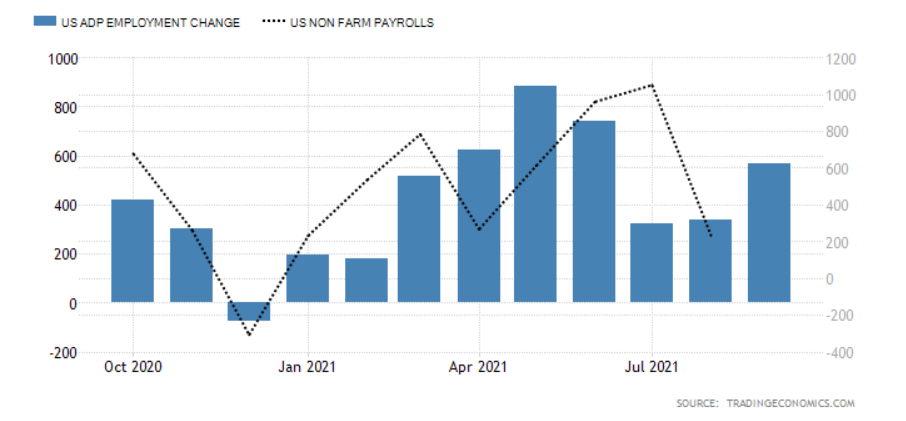

ADP payrolls – the latest September ADP payrolls figure provided a welcome bounce, with the figure of 475,000 managing to recover after insightful 235,000 figure for August. The relationship been ADP and NFP payrolls may not be perfect, but it can often predict the direction of the move. Thus, this ADP rebound does support the notion that we could see a decent recovery for payrolls as expected.

Source: Tradingeconomics.com

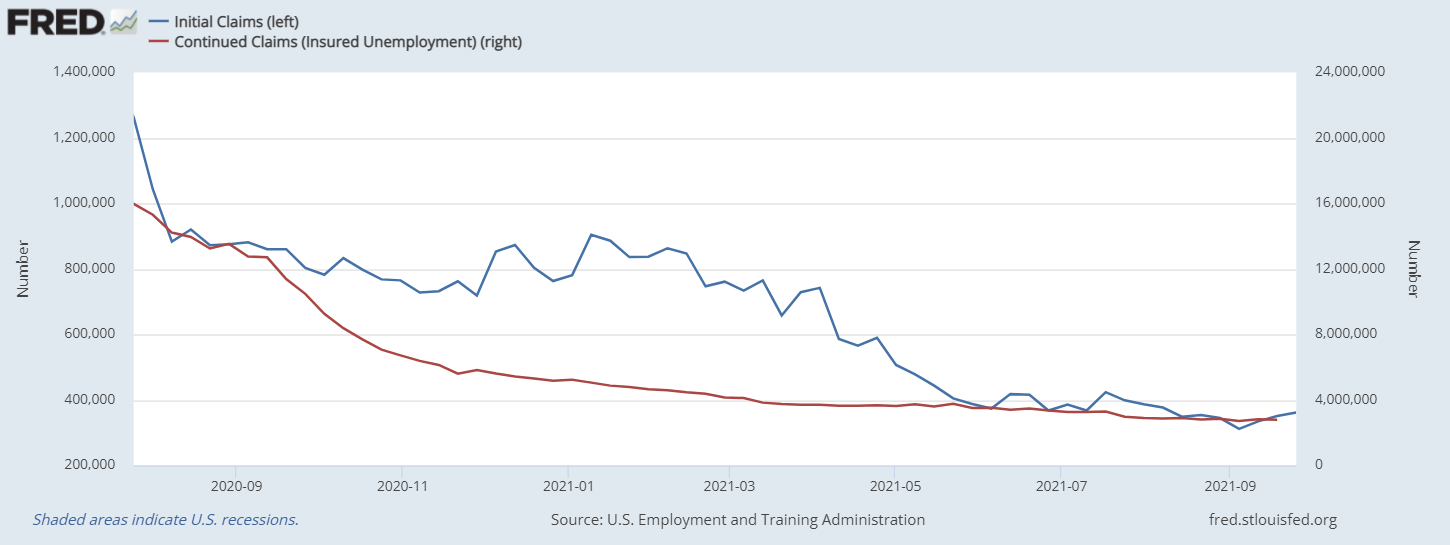

Jobless claims – both initial and continuing jobless claims have been gradually drifting lower of late, pointing towards gradual improvements in the September jobs report. This essentially tells us that there are no signs of an impending rise in unemployment, but will not necessarily give us too much on the payrolls front.

Source: Fred

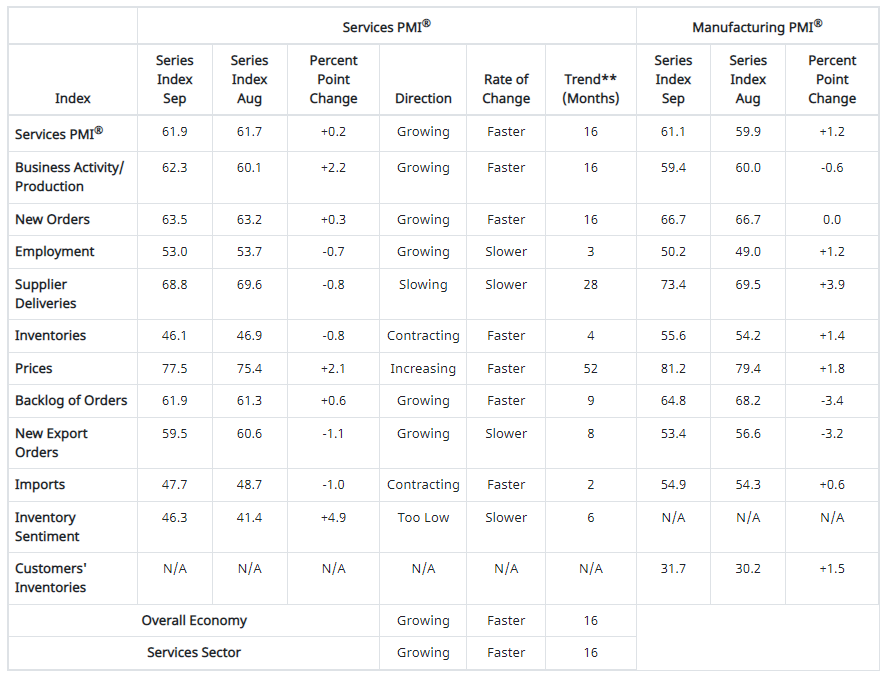

ISM manufacturing PMI – after a worrying August employment reading of 49, we are back into expansion territory ccrding to the latest ISM manufacturing PMI. This supports the rebound theory, although the 50.2 reading for the employment element does also show that things are still not great. 85% of employment related comments stated that firms were attempting to hire more staff. Thus the theme of businesses struggling to fill positions does hold here. As such, a medium-sized rise in payrolls does look likely as it is held back by a lack of candidates.

ISM manufacturing PMI – services sector employment growth appears to be faring better, with the reading of 53 representing a strong growth rate in September. However, the fact that this is down from the 53.7 level seen in August does highlight the tightening seen elsewhere in the market.

Source: IG

Dollar index technical analysis

The dollar is in great shape of late, with the index rising into a fresh 13-month high last week. Haven demand has ramped up as markets head lower, with fears around monetary tightening coming into play as commodities drive up inflation expectations. The double bottom formation seen throughout the past year does point towards further upside to come.

As such, a bullish view holds here, with a strong jobs report helping to further the case that the Federal Resereve (Fed) should act sooner rather than later. Conversely, a disappointing jobs report could weaken the dollar as it helps build the case that economic difficulties mean the Federal Open Market Commitee (FOMC) should hold off until this volatility has played out. With the trend currently bullish, a break below $91.93 would be needed to bring an end to this recent uptrend.

Source: ProRealTime

S&P 500 technical analysis

The S&P 500 has had a tough time of late, with the index losing over 6% from its highs. The price is trying to hold up in recent days, but there is a distinct risk of further downside to come. Keep an eye out for 4232 support, alongside the rarely engaged 200-day simple moving average (SMA).

Source: ProRealTime

Joshua Mahony | Senior Market Analyst, London

08 October 2021

0 Comments

Recommended Comments

There are no comments to display.

Create an account or sign in to comment

You need to be a member in order to leave a comment

Create an account

Sign up for a new account in our community. It's easy!

Register a new accountSign in

Already have an account? Sign in here.

Sign In Now