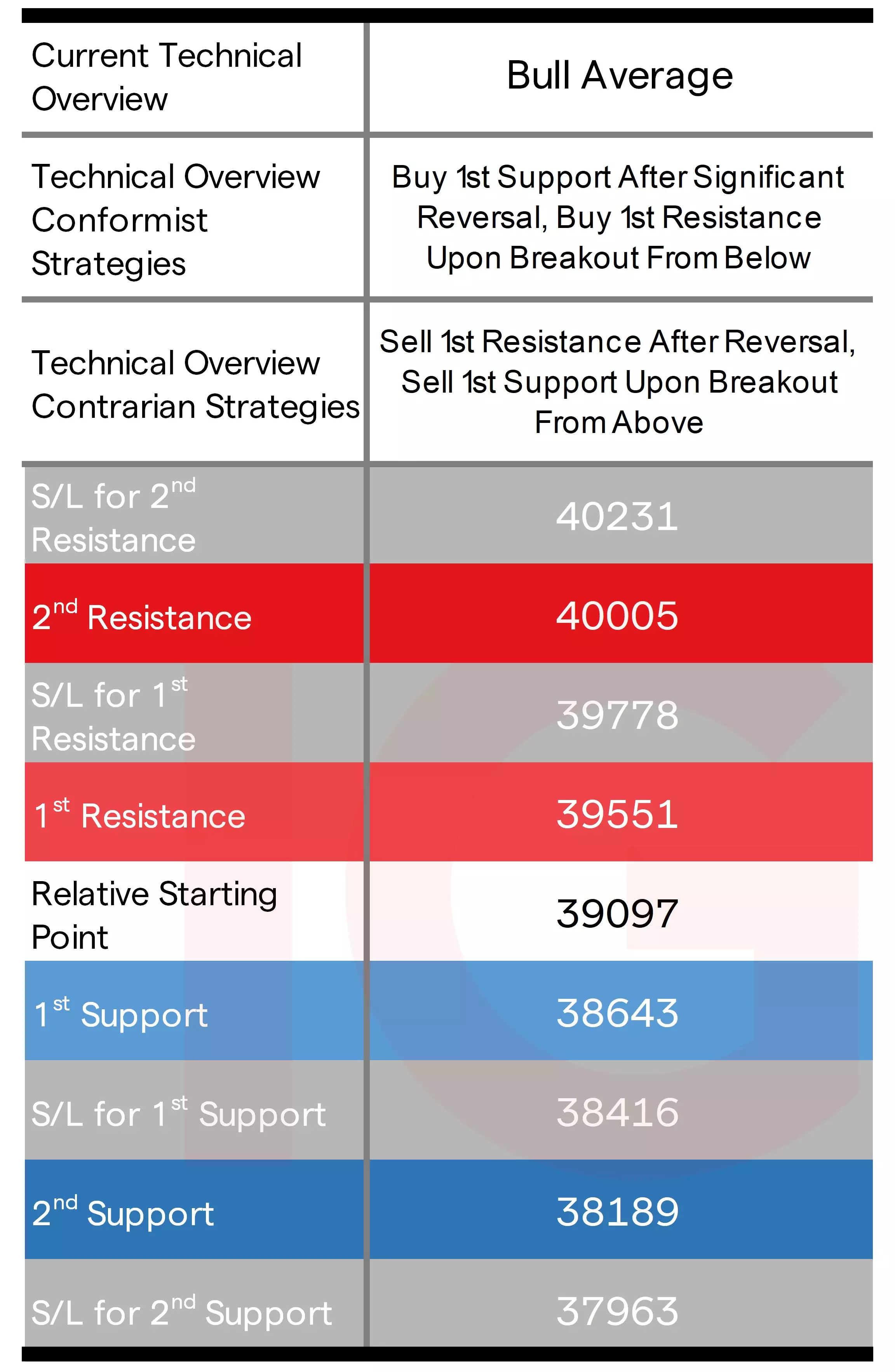

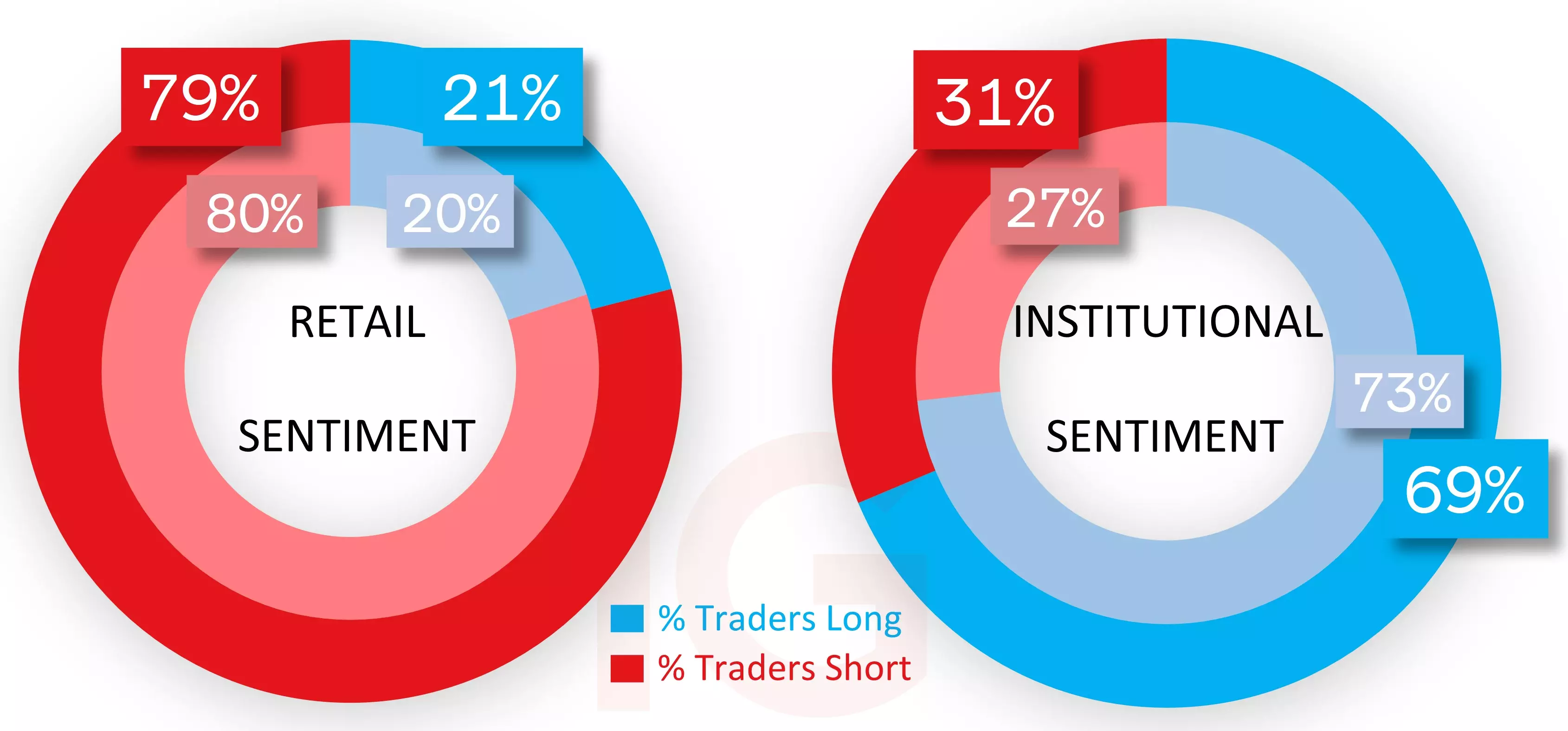

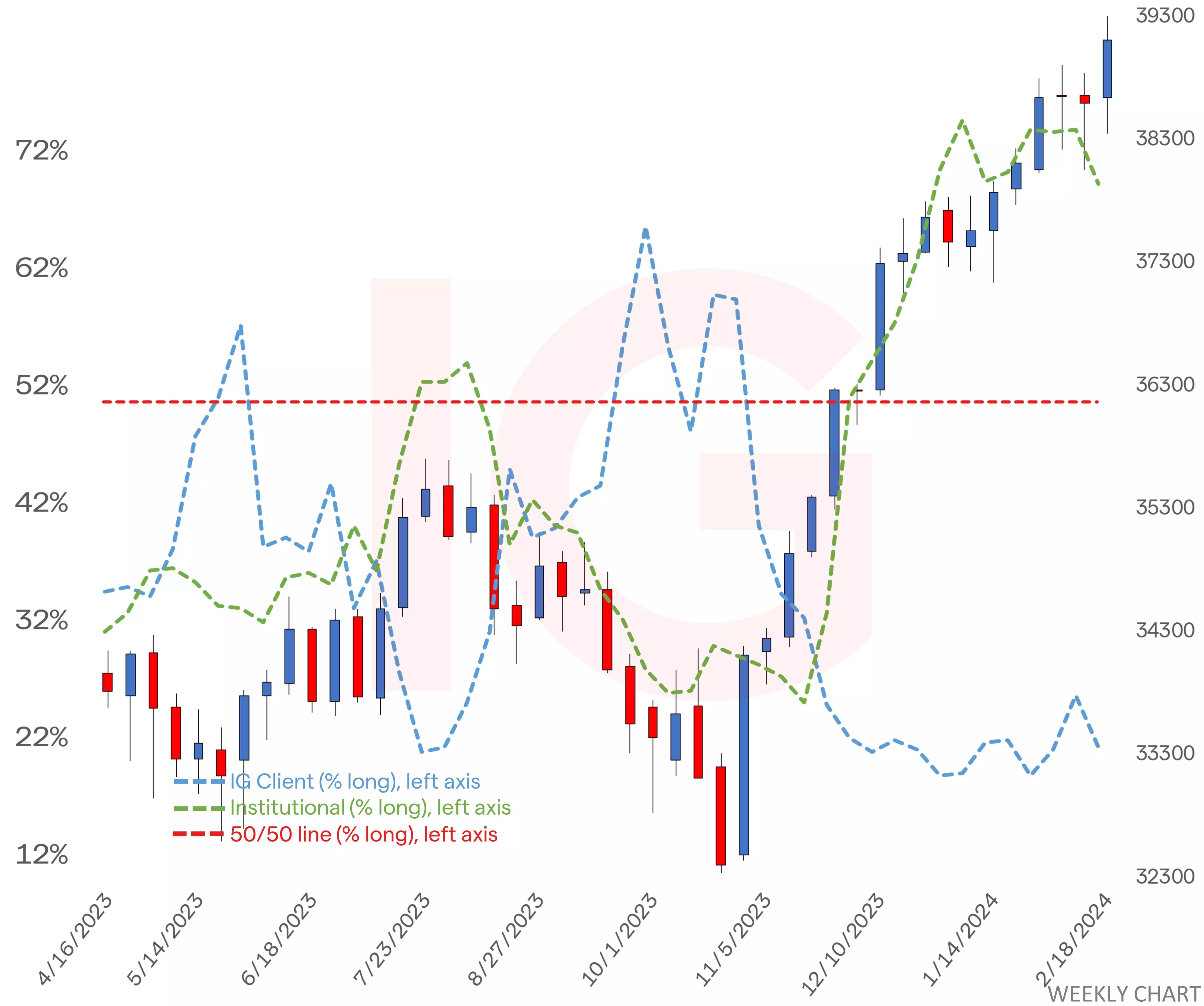

It’s one of the most popular traded markets on our end, and we take a look at the S&P 500’s technical overview in both weekly and daily time frames, the strategies to deploy for conformist, contrarian and ‘hold’ camps.

Dive into the conflicting sentiments of IG clients versus COT speculators and stay ahead of the game with upcoming market events. Don't miss out on this essential guide to understanding the current state of the S&P 500 and preparing for what lies ahead!

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.

Wave 5 Extension on the Dax (Germany 40) ?!? Elliott wave theory

in IG Trading Support - Dealing Questions

Posted

Hi @JustinCamm

Thanks for sharing

Below from our analysts:

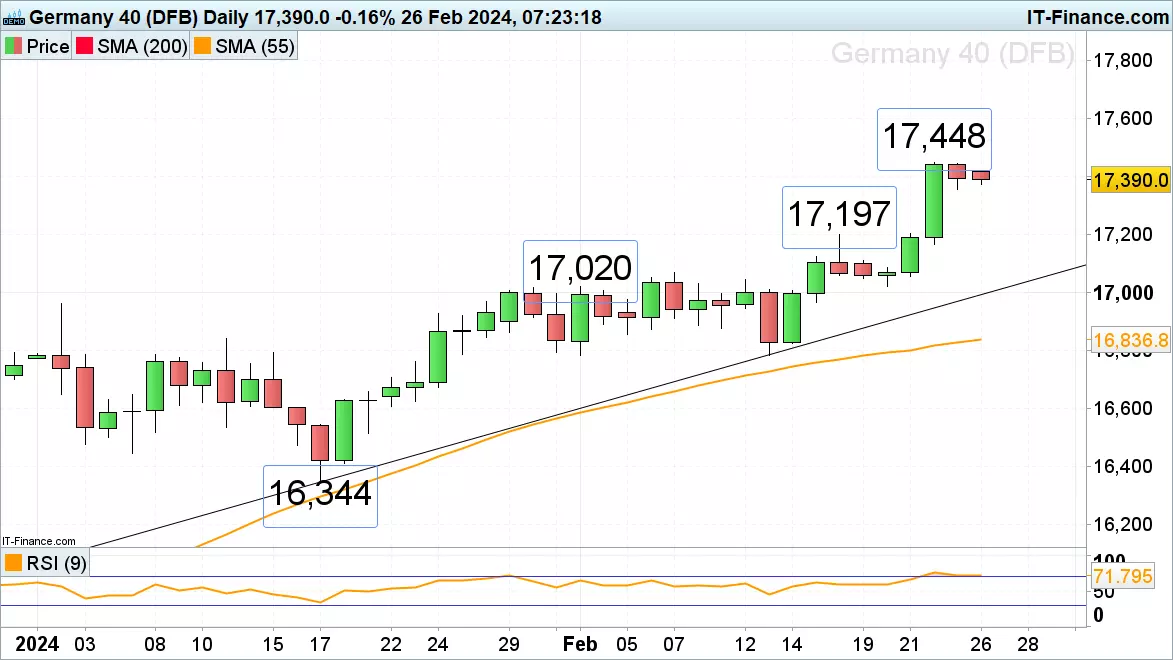

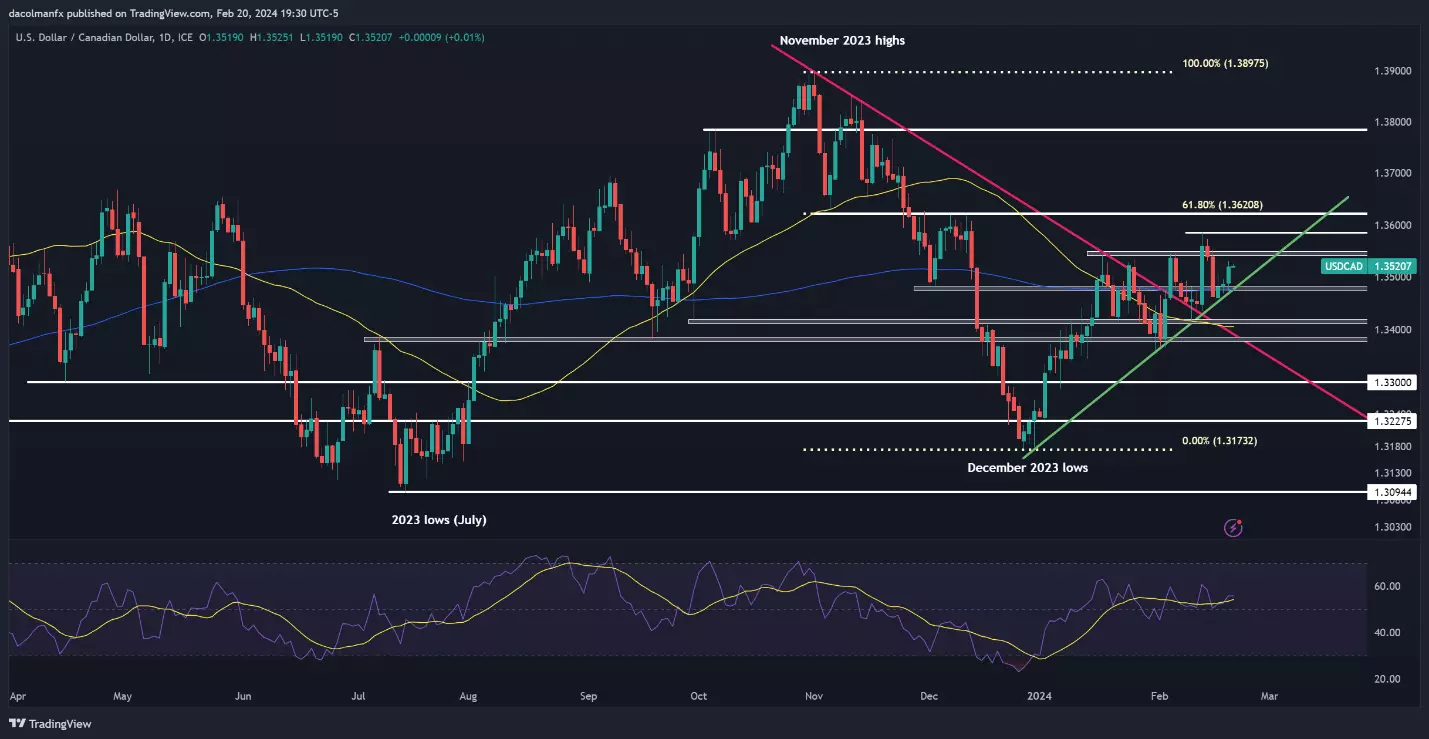

DAX 40 once again trades at record highs

The DAX 40 index seems to be unstoppable as it rallies to yet another record high around the 17,600 mark as the latest earnings season highlighted that European stocks remain undervalued compared to their American counterparts with regards to Price-to-Earnings (PE) ratios. This has attracted further investment in Europe’s largest economy as Germany’s consumer morale also improves slightly.

Minor support is seen along the accelerated uptrend line at 17,464. Above the current record high at 17,607 lies the 18,000 region.

DAX 40 DAILY CHART

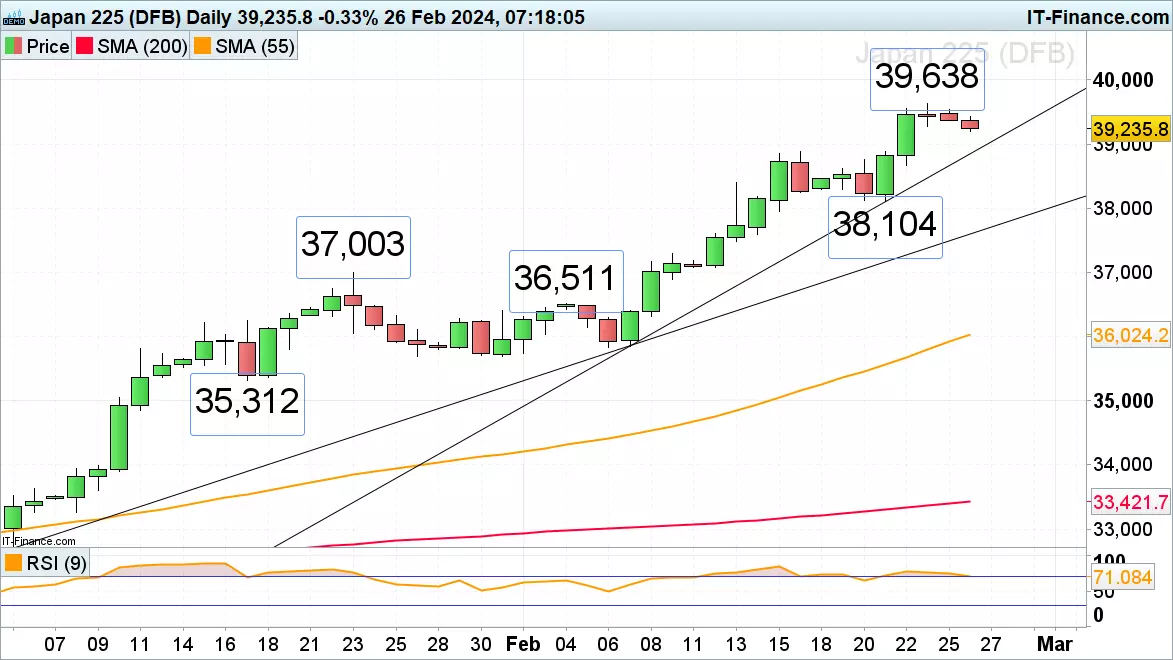

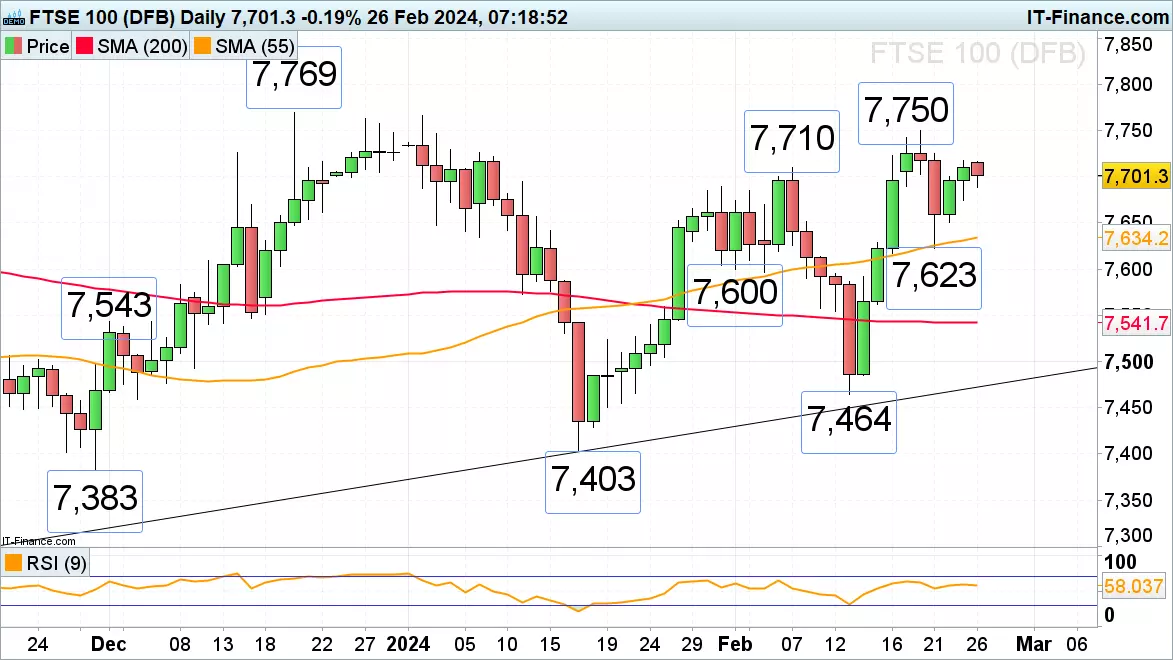

FTSE 100 and S&P 500 Consolidate while DAX 40 Trades in New Record Highs

Feb 28, 2024 1:00 PM +02:00

Axel Rudolph,

IG Senior Market Analyst