MongiIG

-

Posts

9,899 -

Joined

-

Last visited

-

Days Won

41

Content Type

Profiles

Forums

Blogs

Events

Community Tutorials

Store

Posts posted by MongiIG

-

-

15 hours ago, BillionaireFXTrader said:

After todays cpi news, although yoy & mom was same as expections. But core cpi and main cpi was better than expectations, what do you guys think about this?

On Tuesday, the US consumer price index (CPI), a closely watched inflation gauge, increased 0.1% in November and was up 3.1% from a year ago. Excluding volatile food and energy prices, the core CPI increased 0.3% on the month and 4% from a year ago, in line with the consensus. A 2.3% decrease in energy prices helped keep inflation in check, as gasoline fell 6% and fuel oil was off 2.7%. Food prices increased by 0.2%. The Federal Reserve is set to hold interest rates for their third policy meeting and keep the federal funds rate at a 22-year high of 5.25–5.5 per cent.

-

15 hours ago, BillionaireFXTrader said:

What do you guys think will happen if the fed cuts rates?

The US rate decision is due on Wednesday evening 7pm UK. There is a tough balancing act to be made in the face of intense pressure to reveal when and by how much it intends to cut interest rates next year. While the labour market is resilient and consumer spending is solid, there are signs of slower growth and, in turn, lower inflation.

What do you think is going to happen?

-

1

1

-

-

This Thursday, the ECB and Bank of England make key policy decisions. We assess traders' EUR/GBP positions pre-event, using a technical indicator to explain why some opt for a range-trading stance in this low-volatility FX pair.

This information has been prepared by IG, a trading name of IG Markets Limited. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients. See full non-independent research disclaimer and quarterly summary.

-

Asian markets were mixed again, with small gains for the Nikkei 225 and ASX 200 countered by losses in Chinese indices. Attention now turns to the Fed meeting and decision tonight. While a 'no change' on rates seems all but certain, it is Powell's tone that markets will focus on. Expectations of a cut in the first half of the year have risen dramatically, but if Powell opts for a more cautious tone then stock markets may come under fresh pressure, while the dollar could be given renewed upward impetus. UK GDP shrank by 0.3% in October, as household spending was squeezed by rate rises. Stocks are expected to open in positive form in Europe and the US, but nervousness is likely to rise ahead of tonight's decision.

-

The rejuvenated USD and robust US yields weigh on gold at the start of the week; gold and USD extend inverse relationship after NFP. What are potential support levels considered ahead of US CPI and FOMC meeting?

Source: Bloomberg

Source: Bloomberg

Rejuvenated USD and stronger US yields weigh on gold to start the week

Better-than-expected jobs data for November has cooled expectations of large-scale rate cuts in 2024, after the US unemployment rate declined from 3.9% to 3.7%. With the job market maintaining its relative strength, the Fed may have to maintain interest rates at restrictive levels for a little longer than markets anticipated. The ensuing downward revision in rate cut expectations has provided a breath of fresh air for the dollar and US yields which have both moved off their respective lows.

However, with inflation moving in the right direction, tightening credit conditions (stricter requirements for credit applicants and lower demand for credit) and a rise in corporate bankruptcies, the overwhelming narrative across the market is that the Fed will have to cave in and cut rates in support of worsening market conditions. One of the major risk events next week – apart from the obvious central bank meetings – is the US CPI print. A softer-than-expected figure is likely to extend dovish expectations, which could weigh further on the dollar, potentially providing a tailwind for gold prices.

Economic calendar

Source: DailyFX

Source: DailyFX

Gold and dollar extend inverse relationship after NFP

The recent rebound in the dollar and reversal in gold can be seen via the chart below, where the uptick in gold has weighed on the precious metal. Gold prices and the US dollar tend to exhibit an inverse relationship over the longer-term, and can be seen on the zoomed out daily chart.

Gold and the US dollar index

Source: TradingView

Source: TradingView

Potential support levels considered ahead of US CPI and FOMC meeting

Gold has started the week on the back foot, following on from where it ended last week. A second major pullback appears to be in the works since the October trough, and now tests the $1985 level of support. It is no surprise that gold prices have eased after spiking to a new all-time-high early in December, and the recent dollar lift has helped extend the sell-off.

Gold is expected to be highly reactive to USD data this week with US CPI and the FOMC meeting the major catalysts. Throw in the ECB to that mix as EUR/USD makes up the majority of the US dollar index and you have a very busy week with a lot to consider.

Should $1985 hold early on, resistance remains at $2010 followed by $2050. The main catalyst for a bullish continuation is if US CPI cools at a faster rate than anticipated.Gold daily chart

Source: TradingView

Source: TradingView

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.

-

2 hours ago, Carl-Gustav said:

Gold is now trading 6 days down from the high, which could be a cyclical turning point. There is a divergence to the upside and yesterdays close failed to close below cyclical support. Fow now, this is pointing to a temporarily or major low.

Thanks for sharing @Carl-Gustav

All the best - MongiIG

-

1

-

-

Asian indices registered further gains on Tuesday, though the Nikkei 225 struggled to hold on to its early advance. US indices were higher on Monday, continuing their strong run, though nervousness is setting in ahead of inflation data this afternoon and tomorrow's Fed decision. Having come so far in such a short space of time, indices may be vulnerable to some short-term weakness at least, should inflation not meet expectations of a monthly decline, or if the Fed chooses to refute in strong terms the current expectations around rate cuts next year. The UK unemployment rate held at 4.2% in October, while wages grew more slowly for the three months to October, at 7.2%, versus 7.7% expected and 8% at the previous reading.

-

This week sees three major central banks meet to decide on interest rates. All three of the Fed, ECB and BoE are expected to leave rates unchanged, but the commentary around these decisions could cause volatility.

Source: Bloomberg

Source: Bloomberg

Fed to rein in hopes of rate cuts?

The Federal Reserve is expected to maintain the current Fed funds target range of 5.25-5.5% at the upcoming FOMC meeting. This decision is influenced by recent economic indicators such as softer activity numbers, cooling labour data, and moderate month-on-month inflation figures. These factors suggest that the current monetary policy is likely restrictive enough to bring inflation down to the desired 2% level in the coming months.

However, the focus of attention is likely to be on the individual forecasts of Fed members. The market perceives that significant rate cuts are imminent, but it remains to be seen how far the Fed members will align with this sentiment. It is anticipated that there will be considerable resistance to such expectations.

Markets are now firmly anticipating the possibility of aggressive interest rate cuts by the Fed in 2023. On November 1st, after the Fed kept rates steady, markets saw only a 20% chance of a final rate hike in December and expected around 90 basis points of cuts through 2024. Currently, markets clearly believe interest rates have peaked, with 125 basis points of cuts priced in over the next year.

The risk for this Fed meeting is that the central bank proves to be insufficiently dovish for current investor expectations. Risk assets like stocks having come so far since late October that they are now pricing in a lot more good news. Disappointment in the wake of the Fed meeting could spark a selloff in equities and a surge in the dollar that could undermine hopes of a ‘Santa rally’ in stock markets.

ECB split on the way forward

The European Central Bank (ECB) is facing internal disagreements regarding future monetary policy. Some members are open to further rate hikes, while others believe rate cuts may be necessary. The weak economic backdrop does not justify rate hikes, but the solid labour market and wage growth, along with inflation above target, make discussions on rate cuts premature.

The ECB has mentioned the "last mile" in bringing inflation back to target, emphasizing the need to keep rates higher for longer. Wage settlements will also play a significant role in determining the ECB's stance.

Despite the ECB's gradual shift towards a more dovish stance, there is a risk of underestimating disinflation. The ECB is cautious after years of above-target inflation, and will be slow in moving towards a more dovish stance.

Bank of England to stick to tough stance on inflation

The Bank of England (BoE) is expected to maintain its firm stance against interest rate cuts in the UK, despite other central banks considering a change in their approach to inflation. The BoE is projected to keep borrowing costs at a 15-year high and emphasise the need for elevated rates to combat stubborn inflation in the country.

While the European Central Bank and the US Federal Reserve are also likely to keep their benchmark rates unchanged, officials at both institutions have indicated a potential shift towards rate cuts. Although the UK's inflation rate has decreased from its peak of 11.1% a year ago, it remains above the BoE's 2% target.

The BoE is concerned that despite signs of a cooling labour market, wage growth remains strong following the 14 consecutive interest rate hikes between December 2021 and August this year. Governor Andrew Bailey and other members of the Monetary Policy Committee have consistently emphasized that it is premature to consider rate cuts. However, investors are pricing in a potential BoE rate cut for May or June next year.

Nevertheless, the BoE is perceived to be lagging behind the ECB and the Fed, with markets indicating a 70% chance of rate cuts by March for both institutions.

This information has been prepared by IG, a trading name of IG Markets Limited. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients. See full non-independent research disclaimer and quarterly summary.

-

Asia stock indices mostly advance as China consumer prices drop the most in three years after another positive session in the US on Friday, shrugging off stronger-than-expected US jobs data ahead of Wednesday's FOMC meeting. With the ECB and BOE meeting on Thursday, volatility is likely to pick up in the middle of the week. While today's economic calendar is devoid of any market moving data, Tuesday should be more interesting with UK unemployment, Germany ZEW economic sentiment and the US inflation data releases.

-

Dovish RBA and US jobs report propel AUD/USD turbulence, reshaping economic outlook.

Source: Bloomberg

Source: Bloomberg

Last week, the AUD/USD soared to a nineteen-week high at .6691, only to plummet nearly 1.5%, closing at .6576. The sharp decline was fuelled by a potent combination of adverse local and offshore events

The dovish on-hold decision by the RBA last Tuesday, coupled with a sub-par Q3 GDP in Australia, triggered a significant transformation in the Australian interest rate market. It shifted from anticipating further RBA rate hikes to now reflecting expectations of rate cuts in 2024.

Simultaneously, a robust US employment report on Friday night pushed back the anticipated timing and magnitude of Fed rate cuts in 2024. This development bolstered US yields and the strength of the US dollar. Whether the AUD/USD can steady the ship this week will be determined by events in the US, including CPI, the FOMC meeting and retail sales, but also by Thursday’s all-important Australian jobs report for November.

Australia's employment report (Thursday, 14 December at 11.30 am AEDT)

In October, the Australian economy added 55k jobs vs. the 20k expected. The unemployment rate increased to 3.7% from 3.6%, and the participation rate increased to 67% from 66.8%.

Bjorn Jarvis, ABS head of labour statistics, said: "The large increase in employment in October followed a small increase in September of around 8,000 people. Looking over the past two months, these increases equate to average employment growth of around 31,000 people a month, which is slightly lower than the average growth of 35,000 people a month since October 2022."

In November, the market is looking for a +11k rise in employment, and the unemployment rate to rise to 3.8% from 3.7%. The participation rate is expected to ease to 66.9% from 67%.

AU unemployment rate chart

Source: TradingEconomics

Source: TradingEconomics

AUD/USD technical analysis

In last week’s update, we noted that the rally from the October .6270 low had been anything other than “smooth sailing,” and included several testing retracements.

Given the data-rich calendar touched on above, there is a good chance of more testing price action this week. More so, as the AUD/USD closed the week right on the 200-day moving average, making a high conviction directional view somewhat elusive.

Short-term traders may look to sell bounces back towards trendline resistance and last week's highs .6690 area, looking for the AUD/USD to test the .6520/00 support zone. For those who would prefer to buy the dip, .6520/00 is the support zone that needs to hold to prevent a deeper retracement.

AUD/USD daily chart

Source: TradingView

Source: TradingView

- Source TradingView. The figures stated are as of 11 December 2023. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation.

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.

-

1 hour ago, Koslanda50 said:

What is a DM please?

Hi @Koslanda50

DM - Direct Message. Check your Community inbox please

-

1

1

-

-

38 minutes ago, Carl-Gustav said:

Today is NFP

Non-farm payrolls in focus for Fed’s next move

In the US, the focus is on non-farm payrolls for the month of November, due at 1.30pm (UK) today.

For a few weeks now, the market has been trying to figure out how soon the US Federal Reserve will start cutting interest rates. IGTV’s Angela Barnes has the latest.

The US Federal Reserve's decision

The big thing that traders are looking out for is the release of the non-farm payrolls report for November in the US. This report will give us a good idea of how many jobs were added or lost and could affect the US Federal Reserve's decision on interest rates. Right now, there's a tool called CME FedWatch that predicts a 90% chance of a rate cut by May 2024 and a 60% chance of a cut at the March meeting. So, if the report shows that not a lot of jobs were added, the chances of a rate cut happening sooner rather than later might go up.

The JOLTs report

There are a couple of other reports that are giving us some clues. One is the JOLTs report, which showed that job openings decreased a lot and reached the lowest level since March 2021. Another is the ADP survey, which found that private businesses hired 103,000 workers in November, which was less than expected. These reports are making traders pay more attention to the non-farm payrolls data.

People are really interested in the non-farm payrolls report, and you can see that because the price of the US dollar has gone up a little bit. The experts have different ideas about what the report will say. Some think around 100,000 to 275,000 jobs were added, but the average guess is around 180,000. This would be better than October, when 150,000 jobs were added. But keep in mind that around 30,000 workers had come back to work after being on strike.

They think the unemployment rate will stay the same at 3.9%, which is the highest it's been since January 2022. And they predict that hourly earnings will have gone up about 0.3% from October and 4% compared to last year. Overall, this report is an important one for traders because it could affect interest rates. It's interesting to see the different forecasts and what they mean for the job market and the economy.

This information has been prepared by IG, a trading name of IG Markets Limited. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients. See full non-independent research disclaimer and quarterly summary.

-

1

1

-

-

-

There were some muted gains in Asia overnight, but the main mover was the Nikkei, which slumped another 1.7% as the yen continued to strengthen and Japanese GDP was revised down. Hints from the Bank of Japan this week have prompted a flight of short sellers from the yen on expectations that 2024 will finally see some policy tightening in Japan, just as other central banks contemplate cutting rates. Meanwhile, oil clawed back some losses as Russia and Saudi Arabia called on other OPEC+ members to adhere to the recently-agreed production cuts, but both Brent and WTI are still down heavily for the week. US non-farm payrolls are the main event of the day, with the focus on whether job growth is slowing or remaining resilient.

-

1 hour ago, Carl-Gustav said:

After a decade of trading experience, I've successfully created three highly effective indicators tailored for various market conditions: Martin Armstrong Cycles, MIDAS Trading Tools and the FX Capital Flow Scanner. I'm excited to now share them with the IG Community! 😊

Thanks for sharing @Carl-Gustav

-

1

-

-

11 minutes ago, Carl-Gustav said:

US30

Dow edges off highs

The index continues to trim the gains made last week, with Wednesday’s session seeing its largest drop in a month as energy stocks fell sharply thanks to fresh declines in oil prices. However, for the moment a more sustained pullback has yet to develop. Upward momentum has faded, but the price remains above the August highs. Additional gains continue to target 36,570, and then on to the record highs at 36,954.

Source: ProRealTime

Source: ProRealTime

-

1

-

-

Dow edges lower, while Nasdaq 100 and CAC40 mixed

While the Dow is holding on to its recent gains, the Nasdaq 100 is unable to establish a clear direction. The CAC40 has tested trendline resistance from the April highs.

Source: Bloomberg

Source: Bloomberg

Dow edges off highs

The index continues to trim the gains made last week, with Wednesday’s session seeing its largest drop in a month as energy stocks fell sharply thanks to fresh declines in oil prices. However, for the moment a more sustained pullback has yet to develop. Upward momentum has faded, but the price remains above the August highs. Additional gains continue to target 36,570, and then on to the record highs at 36,954.

Source: ProRealTime

Nasdaq 100 fights to establish a direction

This week has seen a see-saw movement in the index; Monday’s losses were reversed by Tuesday’s gains, which were then countered by Wednesday’s drop. The price is hovering above 15,760 support, and a fresh drop below this might then see the price head back towards the 50-day simple moving average. Buyers will be looking for a close back above 16,100 to suggest that a new leg higher has begun.

Source: ProRealTime

Source: ProRealTime

CAC40 struggles around trendline resistance

The price briefly pushed above trendline resistance from the April high yesterday, but after the huge gains since late October it is perhaps not surprising that it was unable to hold above the trendline. Like a number of other indices, the price shows no sign of slowing down or reversing – the consolidation around the 200-day SMA in mid-November seems to have been sufficient for the time being. A close back below 7350 might signal a pullback is beginning, while a close above post-April trendline resistance would then see the price target the late July high at 7526.

Source: ProRealTime

Source: ProRealTime

-

-

Asian indices took their cue from a poor finish on Wall Street, where bullish momentum faded thanks to declining energy stocks. Poor Chinese trade data hit sentiment in the Asia-Pacific region, as weakness in imports flagged fresh concerns about the Chinese economy. Lower oil and commodity prices hit markets on Wednesday, in part thanks to a revival in the US dollar. Overnight the yen saw fresh safe haven flows, taking USDJPY to its lowest level since mid-September, and hitting the Nikkei 225 hard. US weekly unemployment claims are the main event of the day, with a weaker open expected for most European and US indices.

-

Market update: is Bitcoin on the way to $50k or retracement first?

Bitcoin nears $45k; options suggest $50k surge. Crypto resilient, market cap up $750B since Nov '22.BTCUSD daily chart

Source: TradingView

Source: TradingView

-

WTI crude drops below $70, indicating bearish trends; watch key thresholds for market insights.

Source: Bloomberg

Source: Bloomberg

On Wednesday, WTI futures recorded a sharp decline, marking the fourth consecutive session drop and reaching June's lowest level. Today's round about 4% fall adds to December's cumulative loss of nearly 9%, breaking the crucial $70.00 threshold—a bearish development from a technical perspective.

The recent selloff in energy markets hasn’t been driven by a singular catalyst but rather a convergence of multiple factors. First off, investors have been dismayed by OPEC+ supply cuts announced in late November because they will be voluntary rather than mandatory, which can potentially enable members to circumvent individually committed reductions.

Global economic challenges deepen oil market turmoil

Disappointing growth in China, coupled with record US crude production at a time of slowing economic activity, has also created a hostile environment for the commodity. The uptick in US fuel stockpiles beyond the seasonal norm in recent weeks has strengthened the belief that demand destruction is taking place, further weighing on sentiment.

Speculative activity by over-leveraged CTAs, which tend to be trend followers, has reinforced oil's weakness, bolstering volatility and exacerbating prevailing directional moves. With CTAs becoming increasingly dominant, their influence on markets will continue to grow, giving way to more and more episodes of rapid and significant price swings.

Oil's trajectory tied to US economic health

Focusing on the outlook, oil’s path will likely hinge on the health of the US economy. That said, if incoming information validates the view that a recession might emerge soon, prices could remain depressed and even head lower, with the next bearish zone of interest at $67.00. Subsequent losses could draw attention to March and May’s swing lows near $64.00.

In the event of a bullish turnaround, a possibility worth considering given some of the disconnects between physical and paper markets, initial resistance lies around $70.00. A successful breach and price consolidation above this threshold might rekindle buying interest, setting the stage for a rally towards $72.50. Further upside progress would shift the focus to the $75.00 mark.

Crude oil prices daily chart

Source: TradingView

Source: TradingView

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.

-

4 hours ago, DifDrama said:

Bitcoin

Market update: is Bitcoin on the way to $50k or retracement first?

Bitcoin nears $45k; options suggest $50k surge. Crypto resilient, market cap up $750B since Nov '22.

Source: Bloomberg

IG Analyst | Publication date:

Source: Bloomberg

IG Analyst | Publication date:Bitcoin finally stalls following five successive days of gains totaling +-16% and coming within a whisker of the $45k mark. The performance of Bitcoin and the crypto industry in 2023 continues to surprise given the challenges being faced by the industry over the past 18 months.

The world’s largest cryptocurrency is approaching $1T in market cap and is up 180% since November 2022. The 45% of that growth has been recorded over the past six weeks as speculation continues to grow regarding the spot Bitcoin ETF. As things stand, based on the Grayscale Bitcoin Trust's NAV discount, which has narrowed dramatically, the market assigns a probability of around 90% that the Securities and Exchange Commission will approve such a vehicle.

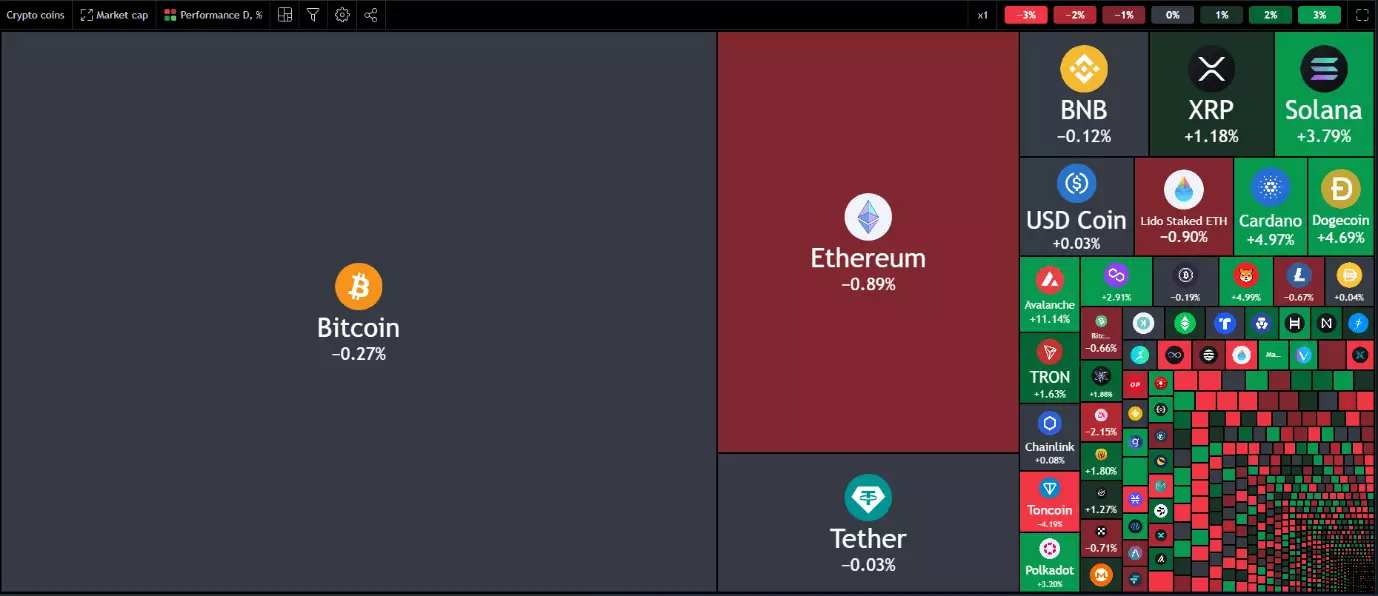

The crypto industry as a whole is benefitting at present having added approximately $750 billion of market cap since November 2022. Looking at the crypto heatmap below and surprisingly the major cryptos appear to be experiencing a lull today which could also be down to some profit taking following the recent rally, while altcoins continue to rise with avalanche up as much as 11%+ on the day.

Crypto market chart

Source: TradingView

Source: TradingView

Crypto industry resilience

If the last 24 months have proven anything it's that crypto is here to stay. Having faced unprecedented challenges and many powerful and vocal proponents to its uses and use cases with the latest being JPMorgan CEO Jamie Dimon, who stated he is deeply opposed to crypto. His argument being the same as countless others who attribute crime, money laundering and tax evasion which is ironic considering the US dollars role in crime across the globe. A story for another time.

Of course, Bitcoin does have its vocal supporters with the likes of ARKS Cathy Wood and MicroStrategy founder Michael Saylor. The failure of US banks this year may have been a blessing in disguise for the crypto industry. There are still clouds hovering over the industry, but this is becoming a normality with market participants hardly taking notice anymore, or so it may seem.

BlackRock announce seed funding for Spot ETF of $100k which is small but it is just a first step with cash likely to change hands a lot quicker once an approval occurs. This shows commitment by BlackRock is ensuring that they are ready for a potential approval.

Bitcoin price outlook

From a technical standpoint BTCUSD is approaching a key area of resistance around the $45k mark. However, options markets are hinting that Bitcoin will hit $50k by January with the Spot Bitcoin ETF expected to be approved early in January as well. The question I am grappling with is what will come first? A test of the $50k mark or the spot Bitcoin ETF approval?

Open interest for Bitcoin $50,000 strike calls is massive, as displayed in the chart below with options also suggesting the recent rally is just the beginning.

Open interest chart for Bitcoin

Source: Kobeissi Letter

Source: Kobeissi Letter

Resistance levels:

- 45000

- 47500

- 50000

Support levels:

- 42500

- 40000

- 38590

BTCUSD daily chart

Source: TradingView

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.

-

19 hours ago, Carl-Gustav said:

Gold is setting up for a major sling-shot to the upside.

-

1

-

-

Indices in Asia staged a recovery from their lows, providing a more optimistic performance than that seen in the US yesterday. After a brief period of weakness, hopes are once again rising that central banks are at the end of their tightening cycle. The ASX 200 and the Nikkei 225 were the strongest performers, but Chinese indices continued their poorer run of form, struggling to move into positive territory for the day. Today sees the release of the latest ADP employment report in the US, the precursor to Friday's non-farm payrolls, along with a decision from the Bank of Canada. Rates are expected to remain unchanged at 5%. The Bank of England's latest Financial Stability Report is also published today, and BoE governor Andrew Bailey will speak at 11am.

IG Morning Call

in General Trading Strategy Discussion

Posted

A fresh record on the Dow caps an astonishing year for markets, as indices rallied in the wake of a dovish Fed meeting. Chairman Jerome Powell caught investors by surprise with his shift in policy, saying that the Fed would not make the mistake of keeping rates high for too long. The FOMC expects three rate cuts next year, which though below market expectations, was enough to give stocks a push higher and knock back the dollar. Now the focus turns to the BoE and ECB, to see if these banks will follow the Fed's lead or whether they will opt for a more cautious tone. US weekly jobless claims are also on the agenda for today.